is to maximize expected

discounted utility from consumption over the remainder of a lifetime that ends in period

is to maximize expected

discounted utility from consumption over the remainder of a lifetime that ends in period  :

:

SolvingMicroDSOPs, April 7, 2022

Note: The code associated with this document should work (though the Matlab code may be out of date), but has been superceded by the set of tools available in the Econ-ARK toolkit, more specifically the HARK Framework. The SMM estination code at the end has specifically been superceded by the SolvingMicroDSOPs REMARK

_____________________________________________________________________________________

Abstract

These notes describe tools for solving microeconomic dynamic stochastic optimization problems,

and show how to use those tools for efficiently estimating a standard life cycle consumption/saving

model using microeconomic data. No attempt is made at a systematic overview of the many possible

technical choices; instead, I present a specific set of methods that have proven useful in my own work

(and explain why other popular methods, such as value function iteration, are a bad idea). Paired

with these notes is Mathematica, Matlab, and Python software that solves the problems described in

the text.

Dynamic Stochastic Optimization, Method of Simulated Moments, Structural Estimation

E21, F41

| PDF: | https://github.com/llorracc/SolvingMicroDSOPs/blob/master/SolvingMicroDSOPs.pdf |

| Slides: | https://github.com/llorracc/SolvingMicroDSOPs/blob/master/SolvingMicroDSOPs-Slides.pdf |

| Web: | https://llorracc.github.io/SolvingMicroDSOPs |

| Code: | https://github.com/llorracc/SolvingMicroDSOPs/tree/master/Code |

| Archive: | https://github.com/llorracc/SolvingMicroDSOPs |

| (Contains LaTeX code for this document and software producing figures and results) |

1Carroll: Department of Economics, Johns Hopkins University, Baltimore, MD, http://www.econ2.jhu.edu/people/ccarroll/, ccarroll@jhu.edu, Phone: (410) 516-7602 The notes were originally written for my Advanced Topics in Macroeconomic Theory class at Johns Hopkins University; instructors elsewhere are welcome to use them for teaching purposes. Relative to earlier drafts, this version incorporates several improvements related to new results in the paper “Theoretical Foundations of Buffer Stock Saving” (especially tools for approximating the consumption and value functions). Like the last major draft, it also builds on material in “The Method of Endogenous Gridpoints for Solving Dynamic Stochastic Optimization Problems” published in Economics Letters, available at http://www.econ2.jhu.edu/people/ccarroll/EndogenousArchive.zip, and by including sample code for a method of simulated moments estimation of the life cycle model a la Gourinchas and Parker (2002) and Cagetti (2003). Background derivations, notation, and related subjects are treated in my class notes for first year macro, available at http://www.econ2.jhu.edu/people/ccarroll/public/lecturenotes/consumption. I am grateful to several generations of graduate students in helping me to refine these notes, to Marc Chan for help in updating the text and software to be consistent with Carroll (2006), to Kiichi Tokuoka for drafting the section on structural estimation, to Damiano Sandri for exceptionally insightful help in revising and updating the method of simulated moments estimation section, and to Weifeng Wu and Metin Uyanik for revising to be consistent with the ‘method of moderation’ and other improvements. All errors are my own.

Calculating the mathematically optimal amount to save is a remarkably difficult problem. Under well-founded assumptions about the nature of risk (and attitudes toward risk), the problem cannot be solved analytically; computational solutions are the only option. To avoid having to solve this hard problem, past generations of economists showed impressive ingenuity in reformulating the question. Budding graduate students are still taught a host of tricks whose purpose is partly to avoid the resort to numerical solutions: Quadratic or Constant Absolute Risk Aversion utility, perfect markets, perfect insurance, perfect foresight, the “timeless” perspective, the restriction of uncertainty to very special kinds,1 and more.

The motivation is mainly to exchange an intractable general problem for a tractable specific alternative. Unfortunately, the burgeoning literature on numerical solutions has shown that the features that yield tractability also profoundly change the solution. These tricks are excuses to solve a problem that has defined away the central difficulty: Understanding the proper role of uncertainty (and other complexities like constraints) in optimal intertemporal choice.

The temptation to use such tricks (and the tolerance for them in leading academic journals) is palpably lessening, thanks to advances in mathematical analysis, increasing computing power, and the growing capabilities of numerical computation software. Together, such tools permit today’s laptop computers to solve problems that required supercomputers a decade ago (and, before that, could not be solved at all).

These points are not unique to the consumption/saving problem; the same propositions apply to almost any question that involves both intertemporal choice and uncertainty, including many aspects of the behavior of firms and governments.

Given the ubiquity of such problems, one might expect that the use of numerical methods for solving dynamic optimization problems would by now be nearly as common as the use of econometric methods in empirical work.

Of course, we remain far from that equilibrium. The most plausible explanation for the gap is that barriers to the use of numerical methods have remained forbiddingly high.

These lecture notes provide a gentle introduction to a particular set of solution tools and show how they can be used to solve some canonical problems in consumption choice and portfolio allocation. Specifically, the notes describe and solve optimization problems for a consumer facing uninsurable idiosyncratic risk to nonfinancial income (e.g., labor or transfer income),2 with detailed intuitive discussion of the various mathematical and computational techniques that, together, speed the solution by many orders of magnitude compared to “brute force” methods. The problem is solved with and without liquidity constraints, and the infinite horizon solution is obtained as the limit of the finite horizon solution. After the basic consumption/saving problem with a deterministic interest rate is described and solved, an extension with portfolio choice between a riskless and a risky asset is also solved. Finally, a simple example is presented of how to use these methods (via the statistical ‘method of simulated moments’ or MSM; sometimes called ‘simulated method of moments’ or SMM) to estimate structural parameters like the coefficient of relative risk aversion (a la Gourinchas and Parker (2002) and Cagetti (2003)).

We are interested in the behavior a consumer whose goal in period is to maximize expected

discounted utility from consumption over the remainder of a lifetime that ends in period :

![[ ]

T∑− t

max 𝔼t βn𝜃𝜃𝜃u(ct+n) ,

n𝜃𝜃𝜃=0](SolvingMicroDSOPs2x.svg) | (1) |

and whose circumstances evolve according to the transition equations3

| (2) |

where the variables are

|

For now, we will assume that the exogenous variables evolve as follows:

|

Using the fact about lognormally distributed variables

ELogNorm4

that if  then

then ![log 𝔼 [φφφ ] = φ + σ2 ∕2

φ](SolvingMicroDSOPs8x.svg) , assumption the assumption about the

distribution of shocks guarantees that

, assumption the assumption about the

distribution of shocks guarantees that ![log 𝔼[𝜃𝜃𝜃] = 0](SolvingMicroDSOPs9x.svg) which means that

which means that ![𝔼 [𝜃𝜃𝜃]](SolvingMicroDSOPs10x.svg) =1 (the mean

value of the transitory shock is 1).

=1 (the mean

value of the transitory shock is 1).

Equation (3) indicates that we are allowing for a predictable average profile of

income growth over the lifetime  (allowing, for example, for typical career wage

paths).5

(allowing, for example, for typical career wage

paths).5

Finally, the utility function is of the Constant Relative Risk Aversion (CRRA), form,

.

.

As is well known, this problem can be rewritten in recursive (Bellman equation) form

![vvvt(mt, pt) = max u (ct) + 𝔼t[βvvvt+1(mt+1, pt+1)]

ct](SolvingMicroDSOPs13x.svg) | (3) |

subject to the Dynamic Budget Constraint (DBC) (2) given above, where  measures total

expected discounted utility from behaving optimally now and henceforth.

measures total

expected discounted utility from behaving optimally now and henceforth.

The single most powerful method for speeding the solution of such models is to redefine the

problem in a way that reduces the number of state variables (if possible). In the consumption

problem here, the obvious idea is to see whether the problem can be rewritten in terms of the

ratio of various variables to permanent noncapital (‘labor’) income  (henceforth for brevity

referred to simply as ‘permanent income.’)

(henceforth for brevity

referred to simply as ‘permanent income.’)

In the last period of life, there is no future,  , so the optimal plan is to consume

everything, implying that

, so the optimal plan is to consume

everything, implying that

| (4) |

Now define nonbold variables as the bold variable divided by the level of permanent

income in the same period, so that, for example,  ; and define

; and define

.6

For our CRRA utility function,

.6

For our CRRA utility function,  , so equation (4) can be rewritten

as

, so equation (4) can be rewritten

as

|

Now define a new optimization problem:

![vt(mt ) = max u(ct) + 𝔼t[βΦΦΦ1 −ρvt+1(mt+1)]

ct t+1

s.t.

at = mt − ct

mt+1 = (R ∕ΦΦΦt+1) at + 𝜃𝜃𝜃t+1

◟--◝◜--◞

≡ ℛt+1](SolvingMicroDSOPs24x.svg) |

The accumulation equation is the normalized version of the transition equation for

.7

Then it is easy to see that for

.7

Then it is easy to see that for  ,

,

|

and so on back to all earlier periods. Hence, if we solve the problem (5) which has only a single

state variable  , we can obtain the levels of the value function, consumption, and all other

variables of interest simply by multiplying the results by the appropriate function of

, we can obtain the levels of the value function, consumption, and all other

variables of interest simply by multiplying the results by the appropriate function of  ,

e.g.

,

e.g.  or

or  . We have thus reduced the

problem from two continuous state variables to one (and thereby enormously simplified its

solution).

. We have thus reduced the

problem from two continuous state variables to one (and thereby enormously simplified its

solution).

For some problems it will not be obvious that there is an appropriate ‘normalizing’ variable, but many problems can be normalized if sufficient thought is given. For example, Valencia (2006) shows how a bank’s optimization problem can be normalized by the level of the bank’s productivity.

The first order condition for (5) with respect to  is

is

![u′(c ) = 𝔼 [β ℛ ΦΦΦ1 −ρv′ (m )]

t t t+1 t+1 t+1 t+1

= 𝔼t [βR ΦΦΦt−+ρ1v ′t+1(mt+1 )]](SolvingMicroDSOPs34x.svg) |

and because the Envelope theorem tells us that

![v ′t(mt ) = 𝔼t[βRΦΦΦ −tρ+1v′t+1(mt+1)]](SolvingMicroDSOPs35x.svg) | (5) |

we can substitute the LHS of (5) for the RHS of (5) to get

| (6) |

and rolling this equation forward one period yields

| (7) |

while substituting the LHS in equation (5) gives us the Euler equation for consumption

![′ −ρ ′

u (ct) = 𝔼t [βR ΦΦΦ t+1u (ct+1)].](SolvingMicroDSOPs38x.svg) | (8) |

Now note that in equation (7) neither  nor

nor  has any direct effect on

has any direct effect on  - only

the difference between them (i.e. unconsumed market resources or ‘assets’

- only

the difference between them (i.e. unconsumed market resources or ‘assets’  )

matters. It is therefore possible (and will turn out to be convenient) to define a

function8

)

matters. It is therefore possible (and will turn out to be convenient) to define a

function8

![𝔳t(at) = 𝔼t[βΦΦΦ1−t+1ρvt+1(ℛt+1at + 𝜃𝜃𝜃t+1)]](SolvingMicroDSOPs43x.svg) | (9) |

that returns the expected  value associated with ending period

value associated with ending period  with any given

amount of assets. This definition implies that

with any given

amount of assets. This definition implies that

![𝔳′(a ) = 𝔼 [βR ΦΦΦ− ρv′ (ℛ a + 𝜃𝜃𝜃 )]

t t t t+1 t+1 t+1 t t+1](SolvingMicroDSOPs46x.svg) | (10) |

or, substituting from equation (7),

![′ [ −ρ ′ ]

𝔳t(at) = 𝔼t βRΦΦΦt+1u (ct+1(ℛt+1at + 𝜃𝜃𝜃t+1)) .](SolvingMicroDSOPs47x.svg) | (11) |

Finally, note for future use that the first order condition (5) can now be rewritten as

| (12) |

The problem in the second-to-last period of life is:

![v (m ) = max u (c ) + β 𝔼 [ΦΦΦ1 −ρv ((m − c )ℛ + 𝜃𝜃𝜃 )],

T−1 T−1 cT−1 T −1 T−1 T T T−1 T− 1 T T](SolvingMicroDSOPs49x.svg) |

and using (1) the fact that  ; (2) the definition of

; (2) the definition of  ; (3) the definition of the

expectations operator, and (4) the fact that

; (3) the definition of the

expectations operator, and (4) the fact that  is nonstochastic, this becomes

is nonstochastic, this becomes

|

where  is the cumulative distribution function for

is the cumulative distribution function for  .

.

In principle, the maximization implicitly defines a function  that yields

optimal consumption in period

that yields

optimal consumption in period  for any given level of resources

for any given level of resources  . Unfortunately,

however, there is no general analytical solution to this maximization problem, and so for any

given

. Unfortunately,

however, there is no general analytical solution to this maximization problem, and so for any

given  we must use numerical computational tools to find the

we must use numerical computational tools to find the  that maximizes

the expression. This is excruciatingly slow because for every potential

that maximizes

the expression. This is excruciatingly slow because for every potential  to be

considered, the integral must be calculated numerically, and numerical integration is very

slow.

to be

considered, the integral must be calculated numerically, and numerical integration is very

slow.

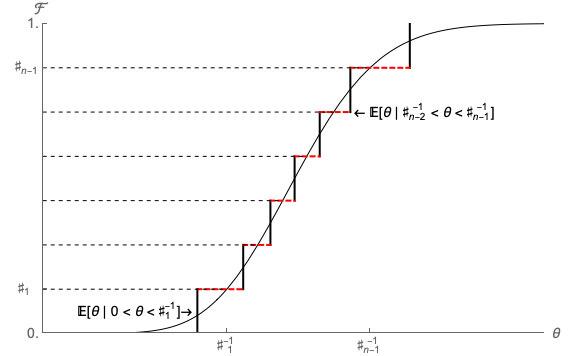

Our first time-saving step is therefore to construct a discrete approximation to the lognormal

distribution that can be used in place of numerical integration. We calculate an  -point

approximation as follows.

-point

approximation as follows.

Define a set of points from  to

to  on the

on the ![[0,1]](SolvingMicroDSOPs65x.svg) interval as the elements of the set

interval as the elements of the set

.9

Call the inverse of the

.9

Call the inverse of the  distribution

distribution  , and define the points

, and define the points  . Then the

conditional mean of

. Then the

conditional mean of  in each of the intervals numbered 1 to

in each of the intervals numbered 1 to  is:

is:

![∫ ♯−1

𝜃𝜃𝜃 ≡ 𝔼 [𝜃𝜃𝜃|♯−1 ≤ 𝜃𝜃𝜃 < ♯− 1] = i 𝜗 dℱ (𝜗 ).

i i− 1 i ♯−1

i−1](SolvingMicroDSOPs73x.svg) | (13) |

The method is illustrated in Figure 1. The solid continuous curve represents the “true” CDF

for a lognormal distribution such that

for a lognormal distribution such that ![𝔼[𝜃𝜃𝜃] = 1](SolvingMicroDSOPs75x.svg) ,

,  . The short vertical line

segments represent the

. The short vertical line

segments represent the  equiprobable values of

equiprobable values of  which are used to approximate this

distribution.10

which are used to approximate this

distribution.10

Recalling our definition of  , for

, for

| (14) |

so we can rewrite the maximization problem as

| (15) |

Given a particular value of  , a numerical maximization routine can now find the

, a numerical maximization routine can now find the  that maximizes (15) in a reasonable amount of time. The Mathematica program that solves

exactly this problem is called 2period.m. (The archive also contains parallel Matlab programs,

but these notes will dwell on the specifics of the Mathematica implementation, which is

superior in many respects.)

that maximizes (15) in a reasonable amount of time. The Mathematica program that solves

exactly this problem is called 2period.m. (The archive also contains parallel Matlab programs,

but these notes will dwell on the specifics of the Mathematica implementation, which is

superior in many respects.)

The first thing 2period.m does is to read in the file functions.m which contains

definitions of the consumption and value functions; functions.m also defines the function

SolveAnotherPeriod which, given the existence in memory of a solution for period  ,

solves for period

,

solves for period  .

.

The next step is to run the programs setup_params.m, setup_grids.m, setup_shocks.m,

respectively. setup_params.m sets values for the parameter values like the coefficient of

relative risk aversion. setup_shocks.m calculates the values for the  defined above (and

puts those values, and the (identical) probability associated with each of them, in the vector

variables

defined above (and

puts those values, and the (identical) probability associated with each of them, in the vector

variables  Vals and

Vals and  Prob). Finally, setup_grids.m constructs a list of potential values

of cash-on-hand and saving, then puts them in the vector variables mVec = aVec =

Prob). Finally, setup_grids.m constructs a list of potential values

of cash-on-hand and saving, then puts them in the vector variables mVec = aVec =

respectively. Then 2period.m runs the program setup_lastperiod.m which

defines the elements necessary to determine behavior in the last period, in which

respectively. Then 2period.m runs the program setup_lastperiod.m which

defines the elements necessary to determine behavior in the last period, in which  and

and  .

.

After all the setup, the only remaining step in 2period.m is to invoke SolveAnotherPeriod,

which constructs the solution for period  given the presence of the solution for period

given the presence of the solution for period

(constructed by setup_lastperiod.m).

(constructed by setup_lastperiod.m).

Because we will always be comparing our solution to the perfect foresight solution, we also

construct the variables required to characterize the perfect foresight consumption function in

periods prior to  . In particular, we construct the list yExpPDV (which contains the PDV of

expected income – ‘expected human wealth’), and yMinPDV which contains the minimum possible

discounted value of future income at the beginning of period

. In particular, we construct the list yExpPDV (which contains the PDV of

expected income – ‘expected human wealth’), and yMinPDV which contains the minimum possible

discounted value of future income at the beginning of period  (‘minimum human

wealth’).11

(‘minimum human

wealth’).11

The perfect foresight consumption function is also constructed (setup_PerfectForesightSolution.m).

This program uses the fact that, in Mathematica, functions can be saved as objects using the

commands # and &. The # denotes the argument of the function, while the &, placed at the end

of the function, tells Mathematica that the function should be saved as an object. In the

program, the last period perfect foresight consumption function is saved as an element in the

list  = {(# - 1 + Last[yExpPDV]) Last[

= {(# - 1 + Last[yExpPDV]) Last[ Min] &}, where Last[yExpPDV]

gives the just-constructed PDV of human wealth at the beginning of

Min] &}, where Last[yExpPDV]

gives the just-constructed PDV of human wealth at the beginning of  (equal to

1, since current income is included in

(equal to

1, since current income is included in  ), and Last[

), and Last[ Min] gives the perfect

foresight marginal propensity to consume (equal to 1, since it is optimal to spend all

resources in the last period). Since # in the code stands in for what was called

Min] gives the perfect

foresight marginal propensity to consume (equal to 1, since it is optimal to spend all

resources in the last period). Since # in the code stands in for what was called  in

the model, the discounted total wealth is decomposed into discounted non-human

wealth # - 1 and discounted human wealth Last[yExpPDV]. The resulting formula

then corresponds to

in

the model, the discounted total wealth is decomposed into discounted non-human

wealth # - 1 and discounted human wealth Last[yExpPDV]. The resulting formula

then corresponds to  , which translates to

, which translates to  for

for

.

.

The infinite horizon perfect foresight marginal propensity to save

| (16) |

is also defined because it will be useful in a number of derivations.12

The program then constructs behavior for one iteration back from the last period of life by

using the function AddNewPeriodToParamLifeDates. Using the Mathematica command

AppendTo, various existing lists (which characterized the solution for period  ) are redefined

to include an additional element representing the relevant formulas in the second to last period

of life. For example,

) are redefined

to include an additional element representing the relevant formulas in the second to last period

of life. For example,  Min now has two elements. The second element, given by 1/(1 +

Last[

Min now has two elements. The second element, given by 1/(1 +

Last[ ]/Last[

]/Last[ Min]), is the perfect foresight marginal propensity to consume in

Min]), is the perfect foresight marginal propensity to consume in

.13

.13

Next, the program defines a function  [at_] (in functions_stable.m) which is the

exact implementation of (9): It returns the expectation of the value of behaving

optimally in period

[at_] (in functions_stable.m) which is the

exact implementation of (9): It returns the expectation of the value of behaving

optimally in period  given any specific amount of assets at the end of

given any specific amount of assets at the end of  ,

,

.

.

The heart of the program is the next expression (in functions.m). This expression loops over the values of the variable mVec, solving the maximization problem (given in equation (15)):

![max u[c ] + 𝔳 [mVec [[i]]- c]

c](SolvingMicroDSOPs117x.svg) | (17) |

for each of the  values of mVec (henceforth let’s call these points

values of mVec (henceforth let’s call these points  ). The

maximization routine returns two values: the maximized value, and the value of

). The

maximization routine returns two values: the maximized value, and the value of  which

yields that maximized value. When the loop (the Table command) is finished, the variable

vAndcList contains two lists, one with the values

which

yields that maximized value. When the loop (the Table command) is finished, the variable

vAndcList contains two lists, one with the values  and the other with the consumption

levels

and the other with the consumption

levels  associated with the

associated with the  .

.

Now we use the first of the really convenient built-in features of Mathematica. Given a set of

points on a function (in this case, the consumption function  ), Mathematica can

create an object called an InterpolatingFunction which when applied to an input

), Mathematica can

create an object called an InterpolatingFunction which when applied to an input  will

yield the value of

will

yield the value of  that corresponds to a linear interpolation of the value of

that corresponds to a linear interpolation of the value of  from the

points in the InterpolatingFunction object. We can therefore define an approximation to

the consumption function

from the

points in the InterpolatingFunction object. We can therefore define an approximation to

the consumption function  which, when called with an

which, when called with an  that is equal to

one of the points in mVec[[i]] returns the associated value of

that is equal to

one of the points in mVec[[i]] returns the associated value of  , and when called with a

value of

, and when called with a

value of  that is not exactly equal to one of the mVec[[i]], returns the value of

that is not exactly equal to one of the mVec[[i]], returns the value of

that reflects a linear interpolation between the

that reflects a linear interpolation between the  associated with the two

mVec[[i]] points nearest to

associated with the two

mVec[[i]] points nearest to  . Thus if the function is called with

. Thus if the function is called with  and the nearest gridpoints are

and the nearest gridpoints are  and

and  then the value of

then the value of

returned by the function would be

returned by the function would be  . We can define a

numerical approximation to the value function

. We can define a

numerical approximation to the value function  in an exactly analogous

way.

in an exactly analogous

way.

Figures 2 and 3 show plots of the  and

and  InterpolatingFunctions that are generated

by the program 2PeriodInt.m. While the

InterpolatingFunctions that are generated

by the program 2PeriodInt.m. While the  function looks very smooth, the fact that the

function looks very smooth, the fact that the

function is a set of line segments is very evident. This figure provides the beginning of

the intuition for why trying to approximate the value function directly is a bad idea (in this

context).14

function is a set of line segments is very evident. This figure provides the beginning of

the intuition for why trying to approximate the value function directly is a bad idea (in this

context).14

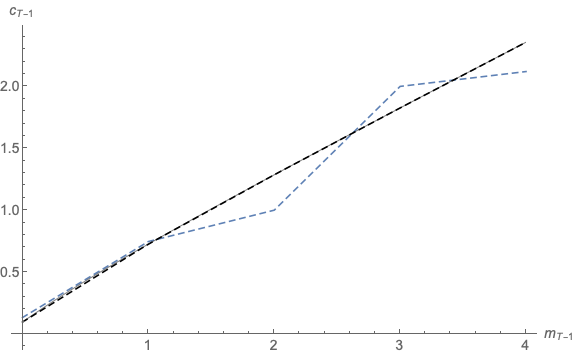

2period.m works well in the sense that it generates a good approximation to the true optimal

consumption function. However, there is a clear inefficiency in the program: Since it uses

equation (15), for every value of  the program must calculate the utility consequences of

various possible choices of

the program must calculate the utility consequences of

various possible choices of  as it searches for the best choice. But for any given

value of

as it searches for the best choice. But for any given

value of  , there is a good chance that the program may end up calculating the

corresponding

, there is a good chance that the program may end up calculating the

corresponding  many times while maximizing utility from different

many times while maximizing utility from different  ’s. For

example, it is possible that the program will calculate the value of ending the period

with

’s. For

example, it is possible that the program will calculate the value of ending the period

with  dozens of times. It would be much more efficient if the program

could make that calculation once and then merely recall the value when it is needed

again.

dozens of times. It would be much more efficient if the program

could make that calculation once and then merely recall the value when it is needed

again.

This can be achieved using the same interpolation technique used above to construct a

direct numerical approximation to the value function: Define a grid of possible values for

saving at time  ,

,  (aVec in setup_grids.m), designating the specific points

(aVec in setup_grids.m), designating the specific points

; for each of these values of

; for each of these values of  , calculate the vector

, calculate the vector  as the collection of

points

as the collection of

points  using equation (9); then construct an InterpolatingFunction

object

using equation (9); then construct an InterpolatingFunction

object  from the list of points on the function captured in the

from the list of points on the function captured in the  and

and  vectors.

vectors.

Thus, we are now interpolating for the function that reveals

the expected value of ending the period with a given amount of

assets.15

The program 2periodIntExp.m solves this problem. Figure 4 compares the true value

function to the InterpolatingFunction approximation; the functions are of course identical

at the gridpoints chosen for  and they appear reasonably close except in the region

below

and they appear reasonably close except in the region

below  .

.

Nevertheless, the resulting consumption rule obtained when  is used instead of

is used instead of

is surprisingly bad, as shown in figure 5. For example, when

is surprisingly bad, as shown in figure 5. For example, when  goes

from 2 to 3,

goes

from 2 to 3,  goes from about 1 to about 2, yet when

goes from about 1 to about 2, yet when  goes from 3 to

4,

goes from 3 to

4,  goes from about 2 to about 2.05. The function fails even to be strictly

concave, which is distressing because Carroll and Kimball (1996) prove that the correct

consumption function is strictly concave in a wide class of problems that includes this

problem.

goes from about 2 to about 2.05. The function fails even to be strictly

concave, which is distressing because Carroll and Kimball (1996) prove that the correct

consumption function is strictly concave in a wide class of problems that includes this

problem.

Loosely speaking, our difficulty reflects the fact that the consumption choice is governed by

the marginal value function, not by the level of the value function (which is the object that we

approximated). To understand this point, recall that a quadratic utility function exhibits risk

aversion because with a stochastic  ,

,

![𝔼 [− (c − /c)2] < − (𝔼[c] − /c)2](SolvingMicroDSOPs177x.svg) | (18) |

where  is the ‘bliss point’. However, unlike the CRRA utility function, with quadratic utility

the consumption/saving behavior of consumers is unaffected by risk since behavior is

determined by the first order condition, which depends on marginal utility, and when utility is

quadratic, marginal utility is unaffected by risk:

is the ‘bliss point’. However, unlike the CRRA utility function, with quadratic utility

the consumption/saving behavior of consumers is unaffected by risk since behavior is

determined by the first order condition, which depends on marginal utility, and when utility is

quadratic, marginal utility is unaffected by risk:

![𝔼[− 2(c − /c)] = − 2(𝔼[c] − /c).](SolvingMicroDSOPs179x.svg) | (19) |

Intuitively, if one’s goal is to accurately capture choices that are governed by marginal value, numerical techniques that approximate the marginal value function will yield a more accurate approximation to optimal behavior than techniques that approximate the level of the value function.

The first order condition of the maximization problem in period  is:

is:

![′ −ρ ′

u (cT −1) = β 𝔼T −1[ΦΦΦ T Ru (cT)]

( 1 ) ∑n𝜃𝜃𝜃

c−T ρ−1 = Rβ --- ΦΦΦ −Tρ(R (mT −1 − cT −1) + 𝜃𝜃𝜃i)−ρ .

n𝜃𝜃𝜃 i=1](SolvingMicroDSOPs181x.svg) | (20) |

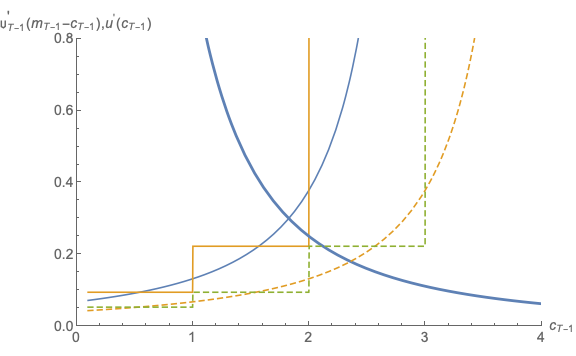

The downward-sloping curve in Figure 6 shows the value of  for our baseline

parameter values for

for our baseline

parameter values for  (the horizontal axis). The solid upward-sloping curve

shows the value of the RHS of (20) as a function of

(the horizontal axis). The solid upward-sloping curve

shows the value of the RHS of (20) as a function of  under the assumption that

under the assumption that

. Constructing this figure is rather time-consuming, because for every value of

. Constructing this figure is rather time-consuming, because for every value of

plotted we must calculate the RHS of (20). The value of

plotted we must calculate the RHS of (20). The value of  for which the RHS and

LHS of (20) are equal is the optimal level of consumption given that

for which the RHS and

LHS of (20) are equal is the optimal level of consumption given that  , so the

intersection of the downward-sloping and the upward-sloping curves gives the optimal value of

, so the

intersection of the downward-sloping and the upward-sloping curves gives the optimal value of

. As we can see, the two curves intersect just below

. As we can see, the two curves intersect just below  . Similarly, the

upward-sloping dashed curve shows the expected value of the RHS of (20) under the

assumption that

. Similarly, the

upward-sloping dashed curve shows the expected value of the RHS of (20) under the

assumption that  , and the intersection of this curve with

, and the intersection of this curve with  yields the

optimal level of consumption if

yields the

optimal level of consumption if  . These two curves intersect slightly below

. These two curves intersect slightly below

. Thus, increasing

. Thus, increasing  from 3 to 4 increases optimal consumption by about

0.5.

from 3 to 4 increases optimal consumption by about

0.5.

Now consider the derivative of our function  . Because we have constructed

. Because we have constructed

as a linear interpolation, the slope of

as a linear interpolation, the slope of  between any two adjacent points

between any two adjacent points

is constant. The level of the slope immediately below any particular

gridpoint is different, of course, from the slope above that gridpoint, a fact which implies that

the derivative of

is constant. The level of the slope immediately below any particular

gridpoint is different, of course, from the slope above that gridpoint, a fact which implies that

the derivative of  follows a step function.

follows a step function.

The solid-line step function in Figure 6 depicts the actual value of  . When

we attempt to find optimal values of

. When

we attempt to find optimal values of  given

given  using

using  , the numerical

optimization routine will return the

, the numerical

optimization routine will return the  for which

for which  . Thus,

for

. Thus,

for  the program will return the value of

the program will return the value of  for which the downward-sloping

for which the downward-sloping

curve intersects with the

curve intersects with the  ; as the diagram shows, this value is

exactly equal to 2. Similarly, if we ask the routine to find the optimal

; as the diagram shows, this value is

exactly equal to 2. Similarly, if we ask the routine to find the optimal  for

for  , it

finds the point of intersection of

, it

finds the point of intersection of  with

with  ; and as the diagram shows,

this intersection is only slightly above 2. Hence, this figure illustrates why the numerical

consumption function plotted earlier returned values very close to

; and as the diagram shows,

this intersection is only slightly above 2. Hence, this figure illustrates why the numerical

consumption function plotted earlier returned values very close to  for both

for both

and

and  .

.

We would obviously obtain much better estimates of the point of intersection

between  and

and  if our estimate of

if our estimate of  were not a

step function. In fact, we already know how to construct linear interpolations to

functions, so the obvious next step is to construct a linear interpolating approximation

to the expected marginal value of end-of-period assets function

were not a

step function. In fact, we already know how to construct linear interpolations to

functions, so the obvious next step is to construct a linear interpolating approximation

to the expected marginal value of end-of-period assets function  . That is, we

calculate

. That is, we

calculate

| (21) |

at the points in aVec yielding  and construct

and construct

as the linear interpolating function that fits this set of points.

as the linear interpolating function that fits this set of points.

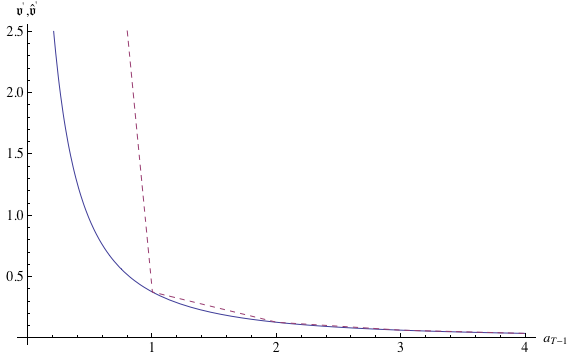

The program file functionsIntExpFOC.m therefore uses the function  a[at_] defined

in functions_stable.m as the embodiment of equation (21), and constructs the

InterpolatingFunction as described above. The results are shown in Figure 7. The linear

interpolating approximation looks roughly as good (or bad) for the marginal value function as

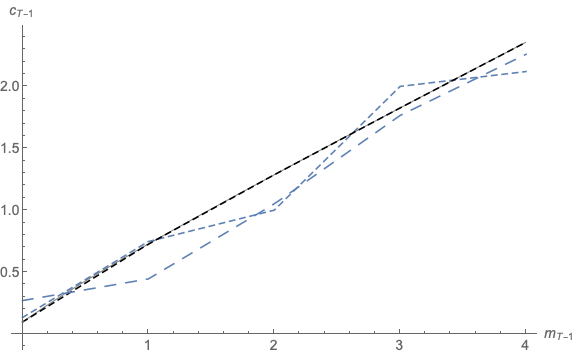

it was for the level of the value function. However, Figure 8 shows that the new consumption

function (long dashes) is a considerably better approximation of the true consumption

function (solid) than was the consumption function obtained by approximating the level of the

value function (short dashes).

a[at_] defined

in functions_stable.m as the embodiment of equation (21), and constructs the

InterpolatingFunction as described above. The results are shown in Figure 7. The linear

interpolating approximation looks roughly as good (or bad) for the marginal value function as

it was for the level of the value function. However, Figure 8 shows that the new consumption

function (long dashes) is a considerably better approximation of the true consumption

function (solid) than was the consumption function obtained by approximating the level of the

value function (short dashes).

Even the new-and-improved consumption function diverges notably from the true solution,

especially at lower values of  . That is because the linear interpolation does an increasingly

poor job of capturing the nonlinearity of

. That is because the linear interpolation does an increasingly

poor job of capturing the nonlinearity of  at lower and lower levels of

at lower and lower levels of

.

.

This is where we unveil our next trick. To understand the logic, start by considering the

case where  and there is no uncertainty (that is, we know for sure that

income next period will be

and there is no uncertainty (that is, we know for sure that

income next period will be  ). The final Euler equation is then:

). The final Euler equation is then:

| (22) |

In the case we are now considering with no uncertainty and no liquidity constraints, the

optimizing consumer does not care whether a unit of income is scheduled to be received in the

future period  or the current period

or the current period  ; there is perfect certainty that the income will

be received, so the consumer treats it as equivalent to a unit of current wealth. Total resources

therefore are comprised of two types: current market resources

; there is perfect certainty that the income will

be received, so the consumer treats it as equivalent to a unit of current wealth. Total resources

therefore are comprised of two types: current market resources  and ‘human wealth’

(the PDV of future income) of

and ‘human wealth’

(the PDV of future income) of  (where we use the Gothic font to signify that this is

the expectation, as of the END of the period, of the income that will be received in future

periods; it does not include current income, which has already been incorporated into

(where we use the Gothic font to signify that this is

the expectation, as of the END of the period, of the income that will be received in future

periods; it does not include current income, which has already been incorporated into

).

).

The optimal solution is to spend half of total lifetime resources in period  and the remainder in period

and the remainder in period  . Since total resources are known with certainty

to be

. Since total resources are known with certainty

to be  , and since

, and since  this implies

that

this implies

that

| (23) |

Of course, this is a highly nonlinear function. However, if we raise both sides of (23) to the

power  the result is a linear function:

the result is a linear function:

| (24) |

This is a specific example of a general phenomenon: A theoretical literature cited in Carroll

and Kimball (1996) establishes that under perfect certainty, if the period-by-period marginal

utility function is of the form  , the marginal value function will be of the form

, the marginal value function will be of the form

for some constants

for some constants  . This means that if we were solving the perfect

foresight problem numerically, we could always calculate a numerically exact (because linear)

interpolation. To put this in intuitive terms, the problem we are facing is that the marginal

value function is highly nonlinear. But we have a compelling solution to that problem,

because the nonlinearity springs largely from the fact that we are raising something to

the power

. This means that if we were solving the perfect

foresight problem numerically, we could always calculate a numerically exact (because linear)

interpolation. To put this in intuitive terms, the problem we are facing is that the marginal

value function is highly nonlinear. But we have a compelling solution to that problem,

because the nonlinearity springs largely from the fact that we are raising something to

the power  . In effect, we can ‘unwind’ all of the nonlinearity owing to that

operation and the remaining nonlinearity will not be nearly so great. Specifically,

applying the foregoing insights to the end-of-period value function

. In effect, we can ‘unwind’ all of the nonlinearity owing to that

operation and the remaining nonlinearity will not be nearly so great. Specifically,

applying the foregoing insights to the end-of-period value function  , we can

define

, we can

define

![′ − 1∕ρ

𝔠T−1(aT− 1) ≡ [𝔳T− 1(aT −1)]](SolvingMicroDSOPs255x.svg) | (25) |

which would be linear in the perfect foresight case. Thus, our procedure is to calculate the

values of  at each of the

at each of the  gridpoints, with the idea that we will construct

gridpoints, with the idea that we will construct  as the interpolating function connecting these points.

as the interpolating function connecting these points.

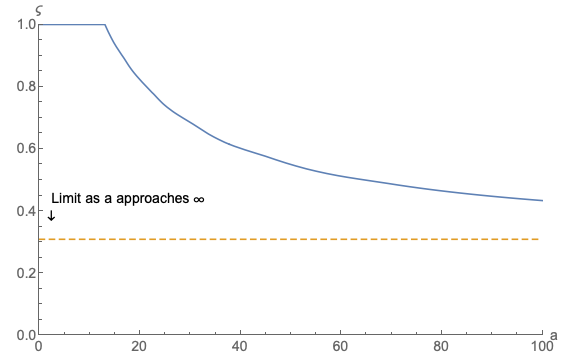

Lower Bound

Lower BoundThis is the appropriate moment to ask an awkward question that we have so far neglected:

How should a function like  be evaluated outside the range of points spanned by

be evaluated outside the range of points spanned by

for which we have calculated the corresponding

for which we have calculated the corresponding  gridpoints

used to produce our linearly interpolating approximation

gridpoints

used to produce our linearly interpolating approximation  (as described in

section 5.3)?

(as described in

section 5.3)?

The natural answer would seem to be linear extrapolation; for example, we could use

| (26) |

for values of  , where

, where  is the derivative of the

is the derivative of the  function at the bottommost gridpoint (see below). Unfortunately, this approach

will lead us into difficulties. To see why, consider what happens to the true (not

approximated)

function at the bottommost gridpoint (see below). Unfortunately, this approach

will lead us into difficulties. To see why, consider what happens to the true (not

approximated)  as

as  approaches the value

approaches the value  . From (21) we

have

. From (21) we

have

| (27) |

But since  , exactly at

, exactly at  the first term in the summation would be

the first term in the summation would be

which is infinity. The reason is simple:

which is infinity. The reason is simple:  is the PDV, as of

is the PDV, as of

, of the minimum possible realization of income in period

, of the minimum possible realization of income in period  (

( ). Thus,

if the consumer borrows an amount greater than or equal to

). Thus,

if the consumer borrows an amount greater than or equal to  (that is, if the consumer

ends

(that is, if the consumer

ends  with

with  ) and then draws the worst possible income shock in

period

) and then draws the worst possible income shock in

period  , he will have to consume zero in period

, he will have to consume zero in period  (or a negative amount), which

yields

(or a negative amount), which

yields  utility and

utility and  marginal utility (or undefined utility and marginal

utility).

marginal utility (or undefined utility and marginal

utility).

These reflections lead us to the conclusion that the consumer faces a ‘self-imposed’ liquidity

constraint (which results from the precautionary motive): He will never borrow an amount

greater than or equal to  (that is, assets will never reach the lower bound of

(that is, assets will never reach the lower bound of

).16

The constraint is ‘self-imposed’ in the sense that if the utility function were different (say,

Constant Absolute Risk Aversion), the consumer would be willing to borrow more than

).16

The constraint is ‘self-imposed’ in the sense that if the utility function were different (say,

Constant Absolute Risk Aversion), the consumer would be willing to borrow more than  because a choice of zero or negative consumption in period

because a choice of zero or negative consumption in period  would yield some finite amount

of utility.17

would yield some finite amount

of utility.17

This self-imposed constraint cannot be captured well when the  function is

approximated by a piecewise linear function like

function is

approximated by a piecewise linear function like  , because a linear approximation can

never reach the correct gridpoint for

, because a linear approximation can

never reach the correct gridpoint for  To see what will happen instead, note

first that if we are approximating

To see what will happen instead, note

first that if we are approximating  the smallest value in aVec must be greater than

the smallest value in aVec must be greater than

(because the expectation for any gridpoint

(because the expectation for any gridpoint  is undefined). Then when the

approximating

is undefined). Then when the

approximating  function is evaluated at some value less than the first element in

aVec[1], the approximating function will linearly extrapolate the slope that characterized the

lowest segment of the piecewise linear approximation (between aVec[1] and aVec[2]), a

procedure that will return a positive finite number, even if the requested

function is evaluated at some value less than the first element in

aVec[1], the approximating function will linearly extrapolate the slope that characterized the

lowest segment of the piecewise linear approximation (between aVec[1] and aVec[2]), a

procedure that will return a positive finite number, even if the requested  point is below

point is below

. This means that the precautionary saving motive is understated, and by an

arbitrarily large amount as the level of assets approaches its true theoretical minimum

. This means that the precautionary saving motive is understated, and by an

arbitrarily large amount as the level of assets approaches its true theoretical minimum

.

.

The foregoing logic demonstrates that the marginal value of saving approaches infinity as

. But this implies that

. But this implies that  ;

that is, as

;

that is, as  approaches its minimum possible value, the corresponding amount of

approaches its minimum possible value, the corresponding amount of  must

approach its minimum possible value: zero.

must

approach its minimum possible value: zero.

The upshot of this discussion is a realization that all we need to do is to augment each of

the  and

and  vectors with an extra point so that the first element in the list used to

produce our InterpolatingFunction is

vectors with an extra point so that the first element in the list used to

produce our InterpolatingFunction is  .

.

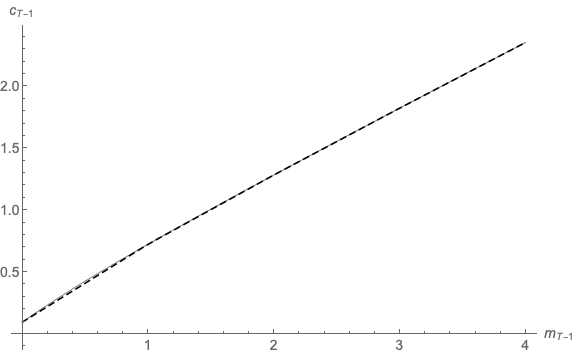

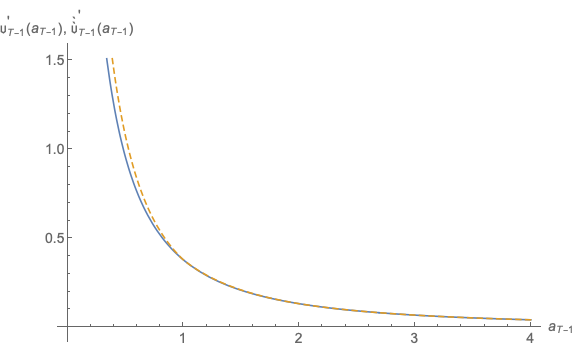

Figure 9 plots the results (generated by the program 2periodIntExpFOCInv.m). The solid

line calculates the exact numerical value of  while the dashed line is the linear

interpolating approximation

while the dashed line is the linear

interpolating approximation  This figure well illustrates the value of the

transformation: The true function is close to linear, and so the linear approximation is

almost indistinguishable from the true function except at the very lowest values of

This figure well illustrates the value of the

transformation: The true function is close to linear, and so the linear approximation is

almost indistinguishable from the true function except at the very lowest values of

.

.

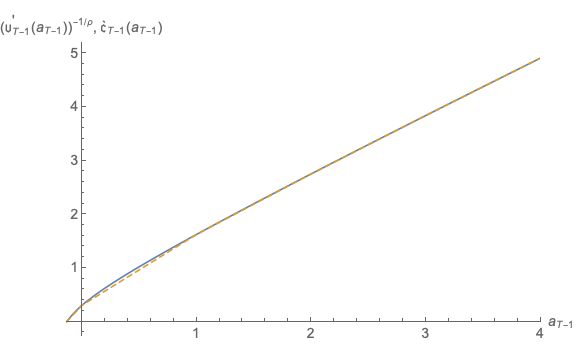

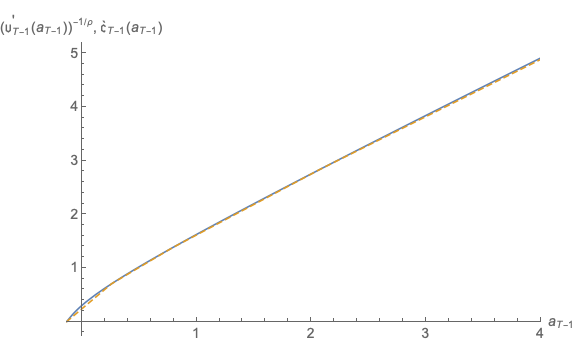

Figure 10 similarly shows that when we calculate  as

as ![[`𝔠 (a )]−ρ

T−1 T− 1](SolvingMicroDSOPs313x.svg) (dashed

line) we obtain a much closer approximation to the true function

(dashed

line) we obtain a much closer approximation to the true function  (solid

line) than we did in the previous program which did not do the transformation

(Figure 7).

(solid

line) than we did in the previous program which did not do the transformation

(Figure 7).

Our solution procedure for  still requires us, for each point in

still requires us, for each point in  (mVect in the

code), to use a numerical rootfinding algorithm to search for the value of

(mVect in the

code), to use a numerical rootfinding algorithm to search for the value of  that

solves

that

solves  . Unfortunately, rootfinding is a notoriously

computation-intensive (that is, slow!) operation.

. Unfortunately, rootfinding is a notoriously

computation-intensive (that is, slow!) operation.

Our next trick lets us completely skip the rootfinding step. The method can be understood

by noting that any arbitrary value of  (greater than its lower bound value

(greater than its lower bound value  ) will

be associated with some marginal valuation as of the end of period

) will

be associated with some marginal valuation as of the end of period  , and the further

observation that it is trivial to find the value of

, and the further

observation that it is trivial to find the value of  that yields the same marginal valuation,

using the first order condition,

that yields the same marginal valuation,

using the first order condition,

| (28) |

But with mutually consistent values of  and

and  (consistent, in the

sense that they are the unique optimal values that correspond to the solution to the

problem in a single state), we can obtain the

(consistent, in the

sense that they are the unique optimal values that correspond to the solution to the

problem in a single state), we can obtain the  that corresponds to both of them

from

that corresponds to both of them

from

| (29) |

These  gridpoints are “endogenous” in contrast to the usual solution method of

specifying some ex-ante grid of values of

gridpoints are “endogenous” in contrast to the usual solution method of

specifying some ex-ante grid of values of  and then using a rootfinding routine to locate

the corresponding optimal

and then using a rootfinding routine to locate

the corresponding optimal  .

.

Thus, we can generate a set of  and

and  pairs that can be interpolated between in

order to yield

pairs that can be interpolated between in

order to yield  at virtually zero computational cost once we have the

at virtually zero computational cost once we have the  values in

hand!18

One might worry about whether the

values in

hand!18

One might worry about whether the  points obtained in this way will provide a good

representation of the consumption function as a whole, but in practice there are good reasons

why they work well (basically, this procedure generates a set of gridpoints that is

naturally dense right around the parts of the function with the greatest nonlinearity).

points obtained in this way will provide a good

representation of the consumption function as a whole, but in practice there are good reasons

why they work well (basically, this procedure generates a set of gridpoints that is

naturally dense right around the parts of the function with the greatest nonlinearity).

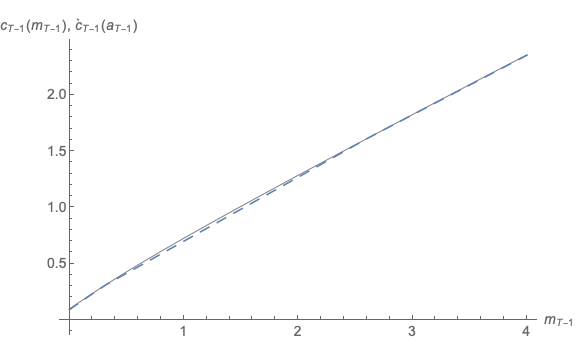

Figure 11 plots the actual consumption function  and the approximated consumption

function

and the approximated consumption

function  derived by the method of endogenous grid points. Compared to the

approximate consumption functions illustrated in Figure 8

derived by the method of endogenous grid points. Compared to the

approximate consumption functions illustrated in Figure 8  is quite close to the actual

consumption function.

is quite close to the actual

consumption function.

Grid

GridThus far, we have arbitrarily used  gridpoints of

gridpoints of  (augmented

in the last subsection by

(augmented

in the last subsection by  ). But it has been obvious from the figures that

the approximated

). But it has been obvious from the figures that

the approximated  function tends to be farthest from its true value

function tends to be farthest from its true value  at

low values of

at

low values of  . Combining this with our insight that

. Combining this with our insight that  is a lower bound, we

are now in position to define a more deliberate method for constructing gridpoints

for

is a lower bound, we

are now in position to define a more deliberate method for constructing gridpoints

for  – a method that yields values that are more densely spaced than the

uniform grid at low values of

– a method that yields values that are more densely spaced than the

uniform grid at low values of  . A pragmatic choice that works well is to find the

values such that (1) the last value exceeds the lower bound by the same amount

. A pragmatic choice that works well is to find the

values such that (1) the last value exceeds the lower bound by the same amount

as our original maximum gridpoint (in our case, 4.); (2) we have the same

number of gridpoints as before; and (3) the multi-exponential growth rate (that is,

as our original maximum gridpoint (in our case, 4.); (2) we have the same

number of gridpoints as before; and (3) the multi-exponential growth rate (that is,

for some number of exponentiations

for some number of exponentiations  ) from each point to the next point is

constant (instead of, as previously, imposing constancy of the absolute gap between

points).

) from each point to the next point is

constant (instead of, as previously, imposing constancy of the absolute gap between

points).

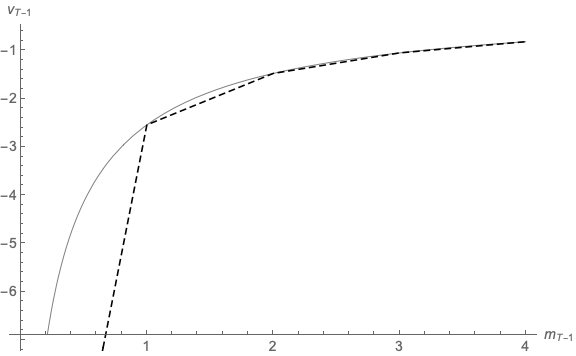

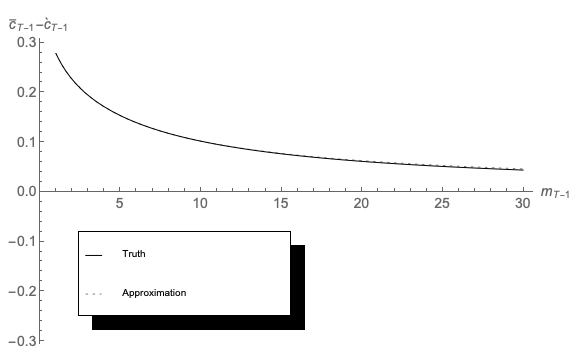

The results (generated by the program 2periodIntExpFOCInvEEE.m) are depicted in Figures 12 and 13, which are notably closer to their respective truths than the corresponding figures that used the original grid.

Unfortunately, this endogenous gridpoints solution is not very well-behaved outside the

original range of gridpoints targeted by the solution method. (Though other common solution

methods are no better outside their own predefined ranges). Figure 14 demonstrates the point

by plotting the amount of precautionary saving implied by a linear extrapolation of our

approximated consumption rule (the consumption of the perfect foresight consumer

minus our approximation to optimal consumption under uncertainty,

minus our approximation to optimal consumption under uncertainty,  ).

Although theory proves that precautionary saving is always positive, the linearly

extrapolated numerical approximation eventually predicts negative precautionary

saving (at the point in the figure where the extrapolated locus crosses the horizontal

axis).

).

Although theory proves that precautionary saving is always positive, the linearly

extrapolated numerical approximation eventually predicts negative precautionary

saving (at the point in the figure where the extrapolated locus crosses the horizontal

axis).

This error cannot be fixed by extending the upper gridpoint; in the presence of serious uncertainty, the consumption rule will need to be evaluated outside of any prespecified grid (because starting from the top gridpoint, a large enough realization of the uncertain variable will push next period’s realization of assets above that top; a similar argument applies below the bottom gridpoint). While a judicious extrapolation technique can prevent this problem from being fatal (for example by carefully excluding negative precautionary saving), the problem is often dealt with using inelegant methods whose implications for the accuracy of the solution are difficult to gauge.

As a preliminary to our solution, define  as end-of-period human wealth (the present

discounted value of future labor income) for a perfect foresight version of the problem of a ‘risk

optimist:’ a consumer who believes with perfect confidence that the shocks will always take the

value 1,

as end-of-period human wealth (the present

discounted value of future labor income) for a perfect foresight version of the problem of a ‘risk

optimist:’ a consumer who believes with perfect confidence that the shocks will always take the

value 1, ![𝜃𝜃𝜃t+n = 𝔼 [𝜃𝜃𝜃] = 1 ∀ n > 0](SolvingMicroDSOPs365x.svg) . The solution to a perfect foresight problem of this kind takes

the form19

. The solution to a perfect foresight problem of this kind takes

the form19

| (30) |

for a constant minimal marginal propensity to consume  given below.

given below.

We similarly define  as ‘minimal human wealth,’ the present discounted value

of labor income if the shocks were to take on their worst possible value in every

future period

as ‘minimal human wealth,’ the present discounted value

of labor income if the shocks were to take on their worst possible value in every

future period  (which we define as corresponding to the beliefs of a

‘pessimist’).

(which we define as corresponding to the beliefs of a

‘pessimist’).

We will call a ‘realist’ the consumer who correctly perceives the true probabilities of the future risks and optimizes accordingly.

A first useful point is that, for the realist, a lower bound for the level of market resources is

, because if

, because if  equalled this value then there would be a positive finite chance

(however small) of receiving

equalled this value then there would be a positive finite chance

(however small) of receiving  in every future period, which would require the

consumer to set

in every future period, which would require the

consumer to set  to zero in order to guarantee that the intertemporal budget constraint

holds (this is the multiperiod generalization of the discussion in section 5.7 about

to zero in order to guarantee that the intertemporal budget constraint

holds (this is the multiperiod generalization of the discussion in section 5.7 about  ).

Since consumption of zero yields negative infinite utility, the solution to realist consumer’s

problem is not well defined for values of

).

Since consumption of zero yields negative infinite utility, the solution to realist consumer’s

problem is not well defined for values of  , and the limiting value of the realist’s

, and the limiting value of the realist’s  is

zero as

is

zero as  .

.

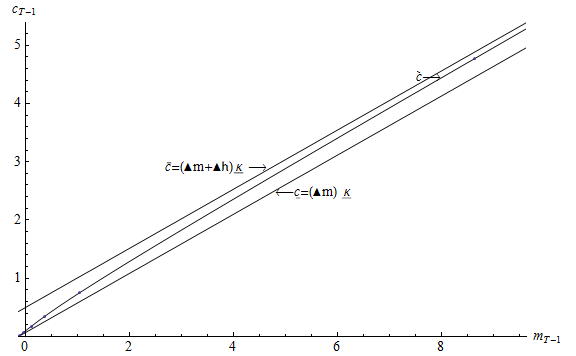

Given this result, it will be convenient to define ‘excess’ market resources as the amount by which actual resources exceed the lower bound, and ‘excess’ human wealth as the amount by which mean expected human wealth exceeds guaranteed minimum human wealth:

|

We can now transparently define the optimal consumption rules for the two perfect foresight

problems, those of the ‘optimist’ and the ‘pessimist.’ The ‘pessimist’ perceives human wealth

to be equal to its minimum feasible value  with certainty, so consumption is given by the

perfect foresight solution

with certainty, so consumption is given by the

perfect foresight solution

|

The ‘optimist,’ on the other hand, pretends that there is no uncertainty about future income, and therefore consumes

|

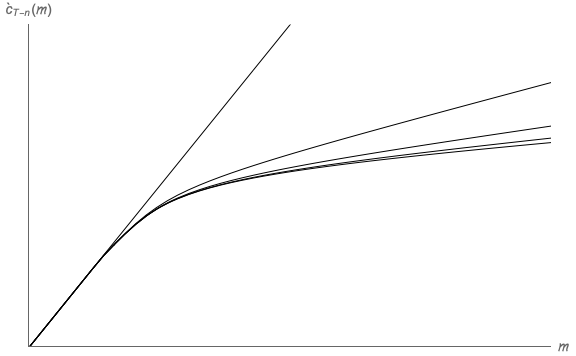

It seems obvious that the spending of the realist will be strictly greater than that of the

pessimist and strictly less than that of the optimist. Figure 15 illustrates the proposition for

the consumption rule in period  .

.

Proof is more difficult than might be imagined, but the necessary work is done in Carroll (2022) so we will take the proposition as a fact and proceed by manipulating the inequality:

where the fraction in the middle of the last inequality is the ratio of actual precautionary saving (the numerator is the difference between perfect-foresight consumption and optimal consumption in the presence of uncertainty) to the maximum conceivable amount of precautionary saving (the amount that would be undertaken by the pessimist who consumes nothing out of any future income beyond the perfectly certain component).

Defining  (which can range from

(which can range from  to

to  ), the object in the middle of

the last inequality is

), the object in the middle of

the last inequality is

| (31) |

and we now define

| (32) |

which has the virtue that it is linear in the limit as  approaches

approaches  .

.

Given  , the consumption function can be recovered from

, the consumption function can be recovered from

| (33) |

Thus, the procedure is to calculate  at the points

at the points  corresponding to the log of the

corresponding to the log of the

points defined above, and then using these to construct an interpolating approximation

points defined above, and then using these to construct an interpolating approximation

from which we indirectly obtain our approximated consumption rule

from which we indirectly obtain our approximated consumption rule  by substituting

by substituting

for

for  in equation (33).

in equation (33).

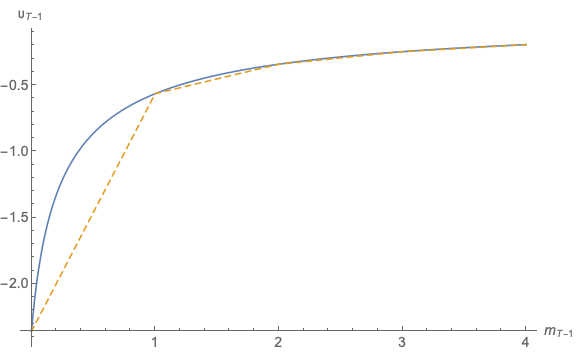

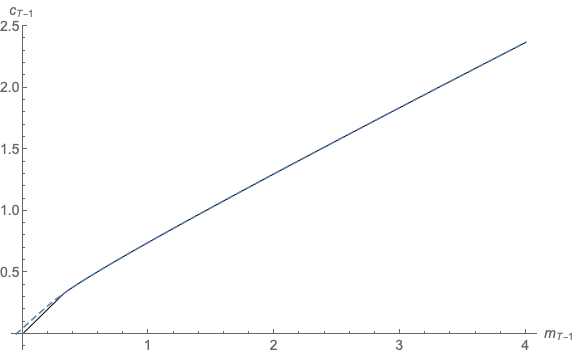

Because this method relies upon the fact that the problem is easy to solve if the decision maker has unreasonable views (either in the optimistic or the pessimistic direction), and because the correct solution is always between these immoderate extremes, we call our solution procedure the ‘method of moderation.’

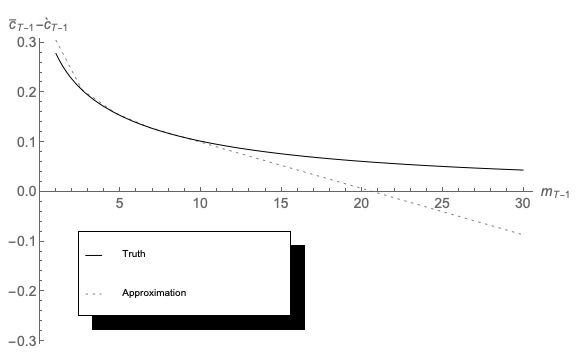

Results are shown in Figure 16; a reader with very good eyesight might be able to detect the barest hint of a discrepancy between the Truth and the Approximation at the far righthand edge of the figure – a stark contrast with the calamitous divergence evident in Figure 14.

Until now, we have calculated the level of consumption at various different gridpoints and used

linear interpolation (either directly for  or indirectly for, say,

or indirectly for, say,  ). But the resulting

piecewise linear approximations have the unattractive feature that they are not differentiable

at the ‘kink points’ that correspond to the gridpoints where the slope of the function changes

discretely.

). But the resulting

piecewise linear approximations have the unattractive feature that they are not differentiable

at the ‘kink points’ that correspond to the gridpoints where the slope of the function changes

discretely.

Carroll (2022) shows that the true consumption function for this problem is ‘smooth:’ It

exhibits a well-defined unique marginal propensity to consume at every positive value of  .

This suggests that we should calculate, not just the level of consumption, but also the

marginal propensity to consume (henceforth

.

This suggests that we should calculate, not just the level of consumption, but also the

marginal propensity to consume (henceforth  ) at each gridpoint, and then find an

interpolating approximation that smoothly matches both the level and the slope at those

points.

) at each gridpoint, and then find an

interpolating approximation that smoothly matches both the level and the slope at those

points.

This requires us to differentiate (31) and (32), yielding

| (34) |

and (dropping arguments) with some algebra these can be combined to yield

| (35) |

To compute the vector of values of (34) corresponding to the points in  , we need the

marginal propensities to consume (designated

, we need the

marginal propensities to consume (designated  ) at each of the gridpoints,

) at each of the gridpoints,  (the vector of

such values is

(the vector of

such values is  ). These can be obtained by differentiating the Euler equation (12) (where

we define

). These can be obtained by differentiating the Euler equation (12) (where

we define  ):

):

| (36) |

with respect to  , yielding a marginal propensity to have consumed

, yielding a marginal propensity to have consumed  at each

gridpoint:

at each

gridpoint:

| (37) |

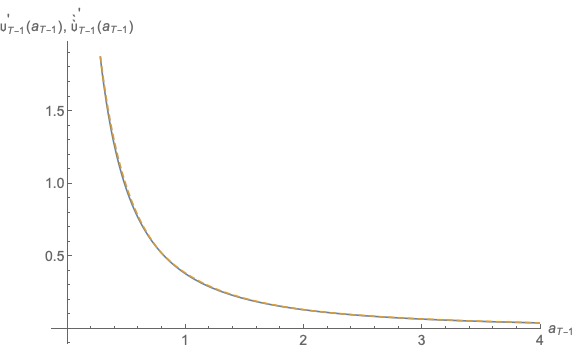

and the marginal propensity to consume at the beginning of the period is obtained from the marginal propensity to have consumed by noting that

|

which, together with the chain rule  , yields the MPC from

, yields the MPC from

| (38) |

Designating  as the approximated consumption rule obtained using an interpolating

polynomial approximation to

as the approximated consumption rule obtained using an interpolating

polynomial approximation to  that matches both the level and the first derivative at

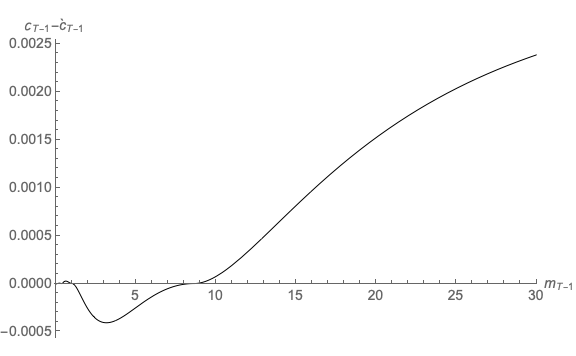

the gridpoints, Figure 17 plots the difference between this latest approximation

and the true consumption rule for period

that matches both the level and the first derivative at

the gridpoints, Figure 17 plots the difference between this latest approximation

and the true consumption rule for period  up to the same large value (far

beyond the largest gridpoint) used in prior figures. Of course, at the gridpoints

the approximation will match the true function; but this figure illustrates that the

approximation is quite accurate far beyond the last gridpoint (which is the last point

at which the difference touches the horizontal axis). (We plot here the difference

between the two functions rather than the level plotted in previous figures, because in

levels the approximation error would not be detectable even to the most eagle-eyed

reader.)

up to the same large value (far

beyond the largest gridpoint) used in prior figures. Of course, at the gridpoints

the approximation will match the true function; but this figure illustrates that the

approximation is quite accurate far beyond the last gridpoint (which is the last point

at which the difference touches the horizontal axis). (We plot here the difference

between the two functions rather than the level plotted in previous figures, because in

levels the approximation error would not be detectable even to the most eagle-eyed

reader.)

Often it is useful to know the value function as well as the consumption rule. Fortunately, many of the tricks used when solving for the consumption rule have a direct analogue in approximation of the value function.

Consider the perfect foresight (or “optimist’s”) problem in period  :

:

|

where  is the present discounted value of consumption. A similar function

can be constructed recursively for earlier periods, yielding the general expression

is the present discounted value of consumption. A similar function

can be constructed recursively for earlier periods, yielding the general expression

| (39) |

where the second line uses the fact demonstrated in Carroll (2022) that  .

.

This can be transformed as

|

with derivative

|

and since  is a constant while the consumption function is linear,

is a constant while the consumption function is linear,  will also be

linear.

will also be

linear.

We apply the same transformation to the value function for the problem with uncertainty (the “realist’s” problem) and differentiate

|

and an excellent approximation to the value function can be obtained by calculating the values

of  at the same gridpoints used by the consumption function approximation, and

interpolating among those points.

at the same gridpoints used by the consumption function approximation, and

interpolating among those points.

However, as with the consumption approximation, we can do even better if we realize that

the  function for the optimist’s problem is an upper bound for the

function for the optimist’s problem is an upper bound for the  function in the

presence of uncertainty, and the value function for the pessimist is a lower bound. Analogously

to (31), define an upper-case

function in the

presence of uncertainty, and the value function for the pessimist is a lower bound. Analogously

to (31), define an upper-case

| (40) |

with derivative (dropping arguments)

| (41) |

and an upper-case version of the  equation in (32):

equation in (32):

| (42) |

with corresponding derivative

| (43) |

and if we approximate these objects then invert them (as above with the  and

and  functions)

we obtain a very high-quality approximation to our inverted value function at the same points

for which we have our approximated value function:

functions)

we obtain a very high-quality approximation to our inverted value function at the same points

for which we have our approximated value function:

| (44) |

from which we obtain our approximation to the value function and its derivatives as

|

Although a linear interpolation that matches the level of  at the gridpoints is simple, a

Hermite interpolation that matches both the level and the derivative of the

at the gridpoints is simple, a

Hermite interpolation that matches both the level and the derivative of the  function at the

gridpoints has the considerable virtue that the

function at the

gridpoints has the considerable virtue that the  derived from it numerically satisfies

the envelope theorem at each of the gridpoints for which the problem has been

solved.

derived from it numerically satisfies

the envelope theorem at each of the gridpoints for which the problem has been

solved.

If we use the double-derivative calculated above to produce a higher-order Hermite polynomial, our approximation will also match marginal propensity to consume at the gridpoints; this would guarantee that the consumption function generated from the value function would match both the level of consumption and the marginal propensity to consume at the gridpoints; the numerical differences between the newly constructed consumption function and the highly accurate one constructed earlier would be negligible within the grid.

Carroll (2022) derives an upper limit  for the MPC as

for the MPC as  approaches its lower bound.

Using this fact plus the strict concavity of the consumption function yields the proposition

that

approaches its lower bound.

Using this fact plus the strict concavity of the consumption function yields the proposition

that

| (45) |

The solution method described above does not guarantee that approximated consumption will respect this constraint between gridpoints, and a failure to respect the constraint can occasionally cause computational problems in solving or simulating the model. Here, we describe a method for constructing an approximation that always satisfies the constraint.

Defining  as the ‘cusp’ point where the two upper bounds intersect:

as the ‘cusp’ point where the two upper bounds intersect:

|

we want to construct a consumption function for ![#

mt ∈ (mt, m t ]](SolvingMicroDSOPs457x.svg) that respects the tighter

upper bound:

that respects the tighter

upper bound:

Again defining  , the object in the middle of the inequality is

, the object in the middle of the inequality is

|

As  approaches

approaches  ,

,  converges to zero, while as

converges to zero, while as  approaches

approaches  ,

,

approaches

approaches  .

.

As before, we can derive an approximated consumption function; call it  . This

function will clearly do a better job approximating the consumption function for low

values of

. This

function will clearly do a better job approximating the consumption function for low

values of  while the previous approximation will perform better for high values of

while the previous approximation will perform better for high values of

.

.

For middling values of  it is not clear which of these functions will perform better.

However, an alternative is available which performs well. Define the highest gridpoint below

it is not clear which of these functions will perform better.

However, an alternative is available which performs well. Define the highest gridpoint below

as

as  and the lowest gridpoint above

and the lowest gridpoint above  as

as  . Then there will be a unique

interpolating polynomial that matches the level and slope of the consumption function at

these two points. Call this function

. Then there will be a unique

interpolating polynomial that matches the level and slope of the consumption function at

these two points. Call this function  .

.

Using indicator functions that are zero everywhere except for specified intervals,

|

we can define a well-behaved approximating consumption function

| (46) |

This just says that, for each interval, we use the approximation that is most appropriate. The function is continuous and once-differentiable everywhere, and is therefore well behaved for computational purposes.

We now construct an upper-bound value function implied for a consumer whose spending behavior is consistent with the refined upper-bound consumption rule.

For  , this consumption rule is the same as before, so the constructed upper-bound

value function is also the same. However, for values

, this consumption rule is the same as before, so the constructed upper-bound

value function is also the same. However, for values  matters are slightly more

complicated.

matters are slightly more

complicated.

Start with the fact that at the cusp point,

|

But for all  ,

,

|

and we assume that for the consumer below the cusp point consumption is given by  so

for

so

for

|

which is easy to compute because  where

where  is as defined above

because a consumer who ends the current period with assets exceeding the lower bound will

not expect to be constrained next period. (Recall again that we are merely constructing an

object that is guaranteed to be an upper bound for the value that the ‘realist’ consumer will

experience.) At the gridpoints defined by the solution of the consumption problem can then

construct

is as defined above

because a consumer who ends the current period with assets exceeding the lower bound will