grows by a constant factor

grows by a constant factor  every period, reflecting exogenous

labor productivity improvements:

every period, reflecting exogenous

labor productivity improvements:

beginCDC

This handout illustrates the logic of precautionary saving by assuming that individuals face only a single, simple kind of uncertainty: A small risk of becoming permanently unemployed. More realistic assumptions yield similar conclusions (after much more work).1

The aggregate wage grows by a constant factor every period, reflecting exogenous

labor productivity improvements:

| (1) |

The consumer lives in a small open economy – there is a constant interest factor  .

Defining

.

Defining  as market resources (net worth plus current income),

as market resources (net worth plus current income),  as end-of-period assets

after all actions have been accomplished (specifically, after the consumption decision), and

as end-of-period assets

after all actions have been accomplished (specifically, after the consumption decision), and  as bank balances before receipt of labor income, the dynamic budget constraint (DBC) can be

decomposed into the following elements:

as bank balances before receipt of labor income, the dynamic budget constraint (DBC) can be

decomposed into the following elements:

| (2) |

where  measures the consumer’s labor productivity (‘endowment’) and

measures the consumer’s labor productivity (‘endowment’) and  is a dummy variable indicating the consumer’s employment state: Everyone

is either employed (state ‘e’), in which case

is a dummy variable indicating the consumer’s employment state: Everyone

is either employed (state ‘e’), in which case  , or unemployed (state

‘u’), in which case

, or unemployed (state

‘u’), in which case  , so that for unemployed individuals labor income is

zero.2

, so that for unemployed individuals labor income is

zero.2

Once a person becomes unemployed, that person can never become employed

again (i.e. if  then

then  ). Consumers have a CRRA felicity

function3

). Consumers have a CRRA felicity

function3

, and they discount future felicity geometrically by

, and they discount future felicity geometrically by  per

period.

per

period.

The solution to the unemployed consumer’s optimization problem is4

| (3) |

where the  superscript signifies the consumer’s (un)employment status;

superscript signifies the consumer’s (un)employment status;  is the marginal propensity to consume for the perfect foresight consumer,

which is strictly below the MPC for the problem with uncertainty (Carroll and

Kimball (1996)); and

is the marginal propensity to consume for the perfect foresight consumer,

which is strictly below the MPC for the problem with uncertainty (Carroll and

Kimball (1996)); and  is what Carroll (2022) calls the ‘return patience

factor.’5

is what Carroll (2022) calls the ‘return patience

factor.’5

We now impose the ‘return impatience condition’ (RIC),

| (4) |

which deserves its name because it is the condition that guarantees that  – the consumer

must not be so patient that, given the interest rate, a boost to resources fails to boost

spending.6

An alternative (equally correct) interpretation is that the condition

guarantees that the PDV of consumption for the unemployed consumer is not

infinity.7

– the consumer

must not be so patient that, given the interest rate, a boost to resources fails to boost

spending.6

An alternative (equally correct) interpretation is that the condition

guarantees that the PDV of consumption for the unemployed consumer is not

infinity.7

For many purposes (not least, the calibration of the model), it turns out to be useful to

alternatviely express impatience conditions like (4) in terms of the upper bound of the range

of time preference factors  that satisfy the condition; solving (4) for

that satisfy the condition; solving (4) for  , we designate this

object

, we designate this

object

| (5) |

and write the alternative version of the constraint as

| (6) |

is the ‘return patience factor’ because it defines the patience factor

is the ‘return patience factor’ because it defines the patience factor  relative

to the return factor

relative

to the return factor  ; correspondingly, we define the ‘return patience rate’ as

lower-case

; correspondingly, we define the ‘return patience rate’ as

lower-case

| (7) |

and we say that a consumer is ‘return impatient’ if the RIC (4) holds (equivalent conditions are  and

and  ).8

).8

If a person who is employed in period  (

( ) is still employed next period (

) is still employed next period ( ),

market resources will be

),

market resources will be

| (8) |

But employed consumers face a constant risk  of becoming unemployed. It will be convenient

to define

of becoming unemployed. It will be convenient

to define  as the probability that a consumer does not become unemployed.

Whether the consumer is employed or not, the consumer’s labor productivity

as the probability that a consumer does not become unemployed.

Whether the consumer is employed or not, the consumer’s labor productivity  is

well-defined:9

For convenience,

is

well-defined:9

For convenience,  is assumed to grow by a factor

is assumed to grow by a factor  every period,

every period,

| (9) |

which means that for a consumer who remains employed, labor income will grow by factor

| (10) |

so that the expected labor income growth factor for employed consumers is the same  as in

the perfect foresight case:

as in

the perfect foresight case:

![( )

ℓtGWt

𝔼t[Wt+1 ℓt+1ξt+1] = ------- (℧ × 0 + //℧ × 1)

( ) //℧

𝔼t[Wt+1-ℓt+1-ξt+1]

Wt ℓt = G,](TractableBufferStock54x.svg) |

which is the reason for (9)’s assumption about the growth of individual labor productivity: It

implies that an increase in  is a pure increase in uncertainty with no effect on the PDV of

expected labor income (‘human wealth’); an increase in

is a pure increase in uncertainty with no effect on the PDV of

expected labor income (‘human wealth’); an increase in  therefore constitutes a

‘mean-preserving spread’ in human wealth.

therefore constitutes a

‘mean-preserving spread’ in human wealth.

The same solution methods used in PerfForesightCRRA can be applied here too (take

the first order condition with respect to  , use the Envelope theorem); the only

difference is the need to keep the expectations operator in place. Using

, use the Envelope theorem); the only

difference is the need to keep the expectations operator in place. Using  as a

placeholder for ‘e’ or ‘u,’ the usual steps lead to the standard consumption Euler

equation:

as a

placeholder for ‘e’ or ‘u,’ the usual steps lead to the standard consumption Euler

equation:

![[ ]

u′(cet) = R β 𝔼t u′(c∙t+1)

[( ∙ ) −ρ]

1 = R β 𝔼 ct+1 .

t cet](TractableBufferStock59x.svg) | (11) |

Defining nonbold variables as the bold equivalent divided by the level of permanent labor

income for an employed consumer, e.g.  , we can rewrite the consumption

Euler equation as

, we can rewrite the consumption

Euler equation as

![[ ]

( c∙ W ℓ ) −ρ

1 = R β 𝔼t -t+1--t+1-t+1-

cetWt ℓt

[( ∙ ) −ρ]

ct+1Φ

= R β 𝔼t cet ΦΦ

[( ) ]

−ρ c∙t+1 −ρ

= ΦΦΦ R β 𝔼t --e-

{ ct }

( ce )− ρ ( cu ) −ρ

= ΦΦΦ −ρR β (1 − ℧ ) -t+1- + ℧ -t+1

cet cet](TractableBufferStock61x.svg) | (12) |

It will be useful now to define a ‘growth patience factor’ (terminology justified below):

| (13) |

which is the factor by which  would grow in the perfect foresight version of the model with

permanent income growth factor

would grow in the perfect foresight version of the model with

permanent income growth factor  (again see PerfForesightCRRA). Using this, (12) can be

written as

(again see PerfForesightCRRA). Using this, (12) can be

written as

![( e )− ρ{ [( u ) ( e ) ]−ρ}

1 = ÞÞÞρ ct+1- (1 − ℧) + ℧ ct+1 -ct-

ΦΦΦ cet cet cet+1

( )− ρ{ [( ) −ρ ]}

ρ cet+1- cut+1

= ÞÞÞΦΦΦ ce 1 + ℧ ce − 1

( ) { t [( ) ]t}+1

cet+1 ρ ρ cet+1- ρ

ce = ÞÞÞΦΦΦ 1 + ℧ cu − 1

( t ) { [( t+1 ) ]}

cet+1 cet+1- ρ 1∕ρ

ce = ÞÞÞΦΦΦ 1 + ℧ cu − 1 .

t t+1](TractableBufferStock65x.svg) | (14) |

beginCDC An interesting thought: Imagine the creation of an insurance system in which the

consumer pledges their next period  to the insurance company in exchange for receiving

a lognormally distributed

to the insurance company in exchange for receiving

a lognormally distributed  with an amount of variation that is (according to some

metric that deserves further thought) equivalent,

with an amount of variation that is (according to some

metric that deserves further thought) equivalent, ![e e 2 2

logˆct+1 ∼ 𝒩 (𝔼t[ct+1] − σˆct+1∕2,σ ˆct+1∕2)](TractableBufferStock68x.svg) .

In that case we would be able to compute analytically the value of

.

In that case we would be able to compute analytically the value of ![𝔼t[(cet+1)−ρ]](TractableBufferStock69x.svg) in (12) and

might be able to proceed with solving a version of the model with transitory as well as

permanent shocks.

in (12) and

might be able to proceed with solving a version of the model with transitory as well as

permanent shocks.

Second thoughts on this: This approach misses the concavity of the consumption function,

which may or may not matter much depending on the magnitude of the shocks. If it does

matter, it should be possible for the insurance company to provide a contract in which the

amount of consumption provided in the contract is, say, ∙](TractableBufferStock70x.svg) where

where  is lognormal

and

is lognormal

and  gives the best approximation to the slope of the consumption function around

gives the best approximation to the slope of the consumption function around

![e

𝔼t[ct+1]](TractableBufferStock73x.svg) . How many people would buy the contract would depend on the profit

margin required by the insurance company, as well as consumption concavity. endCDC

. How many people would buy the contract would depend on the profit

margin required by the insurance company, as well as consumption concavity. endCDC

(This is where the perfect foresight assumption is important; without it (14) would be

![[ ( e ) −ρ { [ ( u )− ρ ] } ]

1 = ÞÞÞ ρ 𝔼 ct+1 1 + ℧ ct+1- − 1

ΦΦΦ t cet cet+1](TractableBufferStock74x.svg) | (15) |

and we would be unable to proceed.)

Now define  (which is the proportion by which consumption would be

greater next period for an employed than for an unemployed person), and define an ‘excess

prudence’ factor

(which is the proportion by which consumption would be

greater next period for an employed than for an unemployed person), and define an ‘excess

prudence’ factor

| (16) |

Appendix A shows that, with some approximations, we can rewrite (11) as

| (17) |

which can be simplified in the logarithmic utility case (where  ) to

) to

| (18) |

Now since consumption if employed  is surely greater than consumption if unemployed

is surely greater than consumption if unemployed

,

,  is certainly a positive number. But since

is certainly a positive number. But since  is the value that

is the value that  would

exhibit in a perfect foresight model, this equation tells us that uncertainty boosts consumption

growth10 –

in the logarithmic case, consumption growth is augmented by an amount proportional to the

probability of becoming unemployed

would

exhibit in a perfect foresight model, this equation tells us that uncertainty boosts consumption

growth10 –

in the logarithmic case, consumption growth is augmented by an amount proportional to the

probability of becoming unemployed  multiplied by the size of the ‘consumption risk’ (the

amount by which consumption would fall if unemployment occurs).

multiplied by the size of the ‘consumption risk’ (the

amount by which consumption would fall if unemployment occurs).

We noted above that for any given  , an increase in uncertainty constitutes

a mean-preserving spread in human wealth; thus the ‘human wealth effect’ of an

increase in

, an increase in uncertainty constitutes

a mean-preserving spread in human wealth; thus the ‘human wealth effect’ of an

increase in  would be zero for a consumer without a precautionary motive. In this

small-open-economy model a change in

would be zero for a consumer without a precautionary motive. In this

small-open-economy model a change in  also has no effect on the interest rate

also has no effect on the interest rate  , and so

none of the conventional determinants of consumption in the perfect foresight model

(the income, substitution, and human wealth effects) is affected by a change in

uncertainty. The increase in consumption growth from an increase in

, and so

none of the conventional determinants of consumption in the perfect foresight model

(the income, substitution, and human wealth effects) is affected by a change in

uncertainty. The increase in consumption growth from an increase in  in (17) or (18)

therefore must be entirely the result of the precautionary motive. Furthermore, because

a profile with faster consumption growth can only exhibit the same PDV if that

faster growth starts from a lower initial consumption level, we know that for any

given initial value of

in (17) or (18)

therefore must be entirely the result of the precautionary motive. Furthermore, because

a profile with faster consumption growth can only exhibit the same PDV if that

faster growth starts from a lower initial consumption level, we know that for any

given initial value of  , the introduction of a risk of becoming unemployed

, the introduction of a risk of becoming unemployed  induces a (precautionary) decline in consumption (and corresponding increase in

saving).

induces a (precautionary) decline in consumption (and corresponding increase in

saving).

Furthermore, under the (compelling) assumption that  , (17) implies that a consumer

with a higher degree of prudence (larger

, (17) implies that a consumer

with a higher degree of prudence (larger  and therefore larger

and therefore larger  ) will anticipate a greater

increment to consumption growth as a consequence of the introduction of uncertainty.

This reflects the greater precautionary saving motive induced by a higher degree of

prudence.

) will anticipate a greater

increment to consumption growth as a consequence of the introduction of uncertainty.

This reflects the greater precautionary saving motive induced by a higher degree of

prudence.

The target level of  (if one exists) will be the point of intersection between the

(if one exists) will be the point of intersection between the  and

and  loci.

loci.

The  locus can be characterized by substituting

locus can be characterized by substituting  :

:

![{ [( cet+1 )ρ ]} ρ

1 = 1 + ℧ -u-- − 1 ÞÞÞ ΦΦΦ

ct+(1 )

−ρ -ce- ρ

ÞÞÞ ΦΦΦ = (1 − ℧) + ℧ cu

( ) ( ) t+1

ÞÞÞ −ΦΦΦρ − 1 + ℧ 1∕ρ ce

------------- = -u--

◟-------℧◝◜-------◞ ct+1

≡ Π

( ≡ϖ ) 1∕ρ ( )

◜-−1-◞◟−ρ----◝ ce

( ℧ (ÞÞÞΦΦΦ − 1)+1 ) = -u--

ct+1

◟---------◝◜----------◞

Π=(1+ϖ)1∕ρ](TractableBufferStock101x.svg) |

which boils down to

| (19) |

The importance of the linearity of the consumption function of the unemployed consumer

now becomes evident: It means that the RHS of (19) is linear in  :

:

| (20) |

beginCDC

| (21) |

and even if we had a solution for  , this equation defines the consumption function for the

employed consumer only implicitly; this explains why the linearity of the consumption

function for the unemployed consumer is essential for the tractability of the solution. endCDC

, this equation defines the consumption function for the

employed consumer only implicitly; this explains why the linearity of the consumption

function for the unemployed consumer is essential for the tractability of the solution. endCDC

We know that  because a consumer in these circumstances (facing possible

perpetual unemployment) will never borrow (see below for a full discussion of this point).

Since the RIC imposes

because a consumer in these circumstances (facing possible

perpetual unemployment) will never borrow (see below for a full discussion of this point).

Since the RIC imposes  , (20) tells us that steady-state consumption (if it

exists)11 is a positive finite

number so long as

, (20) tells us that steady-state consumption (if it

exists)11 is a positive finite

number so long as  .12

.12

, Given Other Parameters

, Given Other ParametersAs with the RIC, it may be useful to rewrite this as defining an upper bound to the permissible time preference rates:

| (23) |

In the limit as  approaches zero, (12) reduces to a requirement that the growth patience

factor is less than one,

approaches zero, (12) reduces to a requirement that the growth patience

factor is less than one,

| (24) |

which, as in PerfForesightCRRA, we call a ‘growth impatience condition’ (GIC) by analogy to

the ‘return impatience condition’ (4) imposed earlier. PerfForesightCRRA shows that the

limit of (12) as  ,

,  , ensures that a consumer facing no uncertainty is sufficiently

impatient that his wealth-to-permanent-income ratio will fall over time. We label the weaker

condition (12) the ‘GIC-TBS’ (the version of the GIC required for a solution to exist in the

Tractable Buffer Stock model). It will always hold if the plain-vanilla GIC

, ensures that a consumer facing no uncertainty is sufficiently

impatient that his wealth-to-permanent-income ratio will fall over time. We label the weaker

condition (12) the ‘GIC-TBS’ (the version of the GIC required for a solution to exist in the

Tractable Buffer Stock model). It will always hold if the plain-vanilla GIC holds because

holds because

. Thus, a consumer who, in the absence of uncertainty, would satisfy both the RIC and

the GIC

. Thus, a consumer who, in the absence of uncertainty, would satisfy both the RIC and

the GIC , will have a positive finite target level of wealth when uncertainty is

introduced.13

, will have a positive finite target level of wealth when uncertainty is

introduced.13

When it is useful to distinguish the version of the GIC that applies in the model with

income growth of  from the corresponding condition when growth is

from the corresponding condition when growth is  we will

label the two conditions GIC

we will

label the two conditions GIC and GIC

and GIC , and the corresponding bounds on

, and the corresponding bounds on  are

are

| (25) |

Using  , we similarly define the corresponding ‘growth impatience rate’:

, we similarly define the corresponding ‘growth impatience rate’:

| (26) |

so that the growth impatience condition (12) (the GIC-TBS) can also be written (approximately) as

| (27) |

or, since  ,

,

| (28) |

Equation (28) becomes easier to satisfy (in the sense of requiring a lower  ) as

) as  increases, since in both places where

increases, since in both places where  appears on the LHS it is with a negative

coefficient.

appears on the LHS it is with a negative

coefficient.

The reason the two appearances of  have not been combined in (28) is that the

separate terms reflect two logically distinct effects. The first appearance, where

have not been combined in (28) is that the

separate terms reflect two logically distinct effects. The first appearance, where

is premultiplied by

is premultiplied by  , can be interpreted as capturing the sense in

which an increase in

, can be interpreted as capturing the sense in

which an increase in  is like an increase in the discounting of the future (the

coefficient on

is like an increase in the discounting of the future (the

coefficient on  is the same as that on

is the same as that on  ). This downweighting of the future

occurs precisely because that future might not occur (if the consumer becomes

unemployed).14

The effect is much like the increase in discounting that occurs when a positive probability of

death is introduced in consumption problems, cf. Blanchard (1985).

). This downweighting of the future

occurs precisely because that future might not occur (if the consumer becomes

unemployed).14

The effect is much like the increase in discounting that occurs when a positive probability of

death is introduced in consumption problems, cf. Blanchard (1985).

The second, separate, reason  weakens growth impatience (that is, the GIC-TBS holds in

more circumstances than the GIC

weakens growth impatience (that is, the GIC-TBS holds in

more circumstances than the GIC ) is that we adjust labor productivity growth so

that

) is that we adjust labor productivity growth so

that  in order to maintain constant human wealth for different values

of

in order to maintain constant human wealth for different values

of  (eq. (9)). For higher

(eq. (9)). For higher  , permanent income growth is greater conditional

on remaining employed; the continuously-employed consumer is effectively more

‘impatient’ in the relevant sense of desiring consumption growth slower than income

growth.

, permanent income growth is greater conditional

on remaining employed; the continuously-employed consumer is effectively more

‘impatient’ in the relevant sense of desiring consumption growth slower than income

growth.

This is essentially a mechanical result, which reflects our model’s design for the purpose of examining thought experiments that manipulate the degree of uncertainty while leaving the perfect-foresight level of human wealth constant.

Note that although  is our measure of uncertainty, neither of these effects of

is our measure of uncertainty, neither of these effects of

is in any meaningful sense directly a ‘precautionary’ effect; instead, they both

reflect effects of

is in any meaningful sense directly a ‘precautionary’ effect; instead, they both

reflect effects of  on the relevant degree of growth impatience in the GIC-TBS

condition.

on the relevant degree of growth impatience in the GIC-TBS

condition.

Appendix B demonstrates that the RIC and the GIC-TBS are necessary conditions for the

existence of a target value of market resources  and that the GIC

and that the GIC is sufficient.

Appendix C solves for an explicit formula for that target.

is sufficient.

Appendix C solves for an explicit formula for that target.

Briefly, this is accomplished as follows. We can obtain the  locus by substituting

locus by substituting

into equation (20):

into equation (20):

| (29) |

Now we need to use a normalized version of the DBC (equation (8)),

| (30) |

to derive the  locus (also referred to as the

locus (also referred to as the  locus):

locus):

| (31) |

The steady-state levels of  and

and  are the values of these two variables at which both

(31) and (29) hold. This is just a set of two linear equations and two unknowns, and with a bit

of algebra can be solved explicitly.

are the values of these two variables at which both

(31) and (29) hold. This is just a set of two linear equations and two unknowns, and with a bit

of algebra can be solved explicitly.

In the special case of logarithmic utility ( ), the appendix shows that (under

some strong assumptions) an approximation to target market resources will be given

by

), the appendix shows that (under

some strong assumptions) an approximation to target market resources will be given

by

| (32) |

and that the GIC and the RIC guarantee that the denominator of the fraction is a positive number.

This expression encapsulates several of the key intuitions of the model. The ‘human

wealth effect’ of growth (cf. Summers (1981)) is captured by the first  term in the

denominator; clearly, for any calibration for which the denominator is a positive number,

increasing

term in the

denominator; clearly, for any calibration for which the denominator is a positive number,

increasing  will increase the size of the denominator and therefore reduce the

target level of wealth. The human wealth effect of interest rates is correspondingly

captured by the

will increase the size of the denominator and therefore reduce the

target level of wealth. The human wealth effect of interest rates is correspondingly

captured by the  term. An increase in the future discounting rate,

term. An increase in the future discounting rate,  , will also

increase the size of the denominator and therefore reduce target wealth. Finally, a

reduction in unemployment risk will boost

, will also

increase the size of the denominator and therefore reduce target wealth. Finally, a

reduction in unemployment risk will boost  and therefore reduce target

wealth.15

and therefore reduce target

wealth.15

The assumption of log utility is restrictive, and probably does not capture sufficient aversion

to consumption fluctuations. Fortunately, another special case helps to illuminate the effect of

higher levels of prudence. The appendix shows that, in the special case where  , the

target level of wealth will be approximable by

, the

target level of wealth will be approximable by

| (33) |

which is like (32) (with  ) but with the addition of the final term involving

) but with the addition of the final term involving  which

measures the amount by which prudence exceeds the logarithmic benchmark. An increase in

which

measures the amount by which prudence exceeds the logarithmic benchmark. An increase in

reduces the denominator of (33) and thereby boosts the target level of wealth:

Exactly what would be expected from an increase in the intensity of the precautionary

motive.

reduces the denominator of (33) and thereby boosts the target level of wealth:

Exactly what would be expected from an increase in the intensity of the precautionary

motive.

Note that the different effects interact with each other, in the sense that the strength of, say, the human wealth effect will vary depending on the values of the other parameters. The ways in which these interactions make intuitive sense will repay deep reflection. (Hint: How much I care about the future governs the power that future events have in determining my targets; use the formula to think about why).

Interestingly, the limit of the buffer stock model as  is not the perfect foresight solution

obtained when

is not the perfect foresight solution

obtained when  is exactly equal to zero.

is exactly equal to zero.

The handout PerfForesightCRRA shows that in the perfect foresight context, it is necessary to

impose the Finite Human Wealth Condition  (henceforth, FHWC

(henceforth, FHWC ) to obtain a sensible

solution.16

But if the FHWC

) to obtain a sensible

solution.16

But if the FHWC holds, the GIC

holds, the GIC is strictly stronger than the RIC, because the

combination

is strictly stronger than the RIC, because the

combination  and

and  obviously implies

obviously implies  . If we substitute

. If we substitute  for

for  ,

we can define the corresponding version of the condition in the case where growth is

,

we can define the corresponding version of the condition in the case where growth is  : the

FHWC

: the

FHWC .

.

It turns out that in the buffer stock model, we can relax the requirement that human wealth is finite.

We pointed out above that (12), which is necessary for the existence of a steady-state level

of consumption, implies that the GIC holds in the case being considered here, the limit as

holds in the case being considered here, the limit as

. The interesting question is therefore what happens when the FHWC

. The interesting question is therefore what happens when the FHWC does not hold

(that is

does not hold

(that is  ).

).

Given that the GIC holds, if the FHWC

holds, if the FHWC does not hold the RIC may or may not hold:

does not hold the RIC may or may not hold:

implies that

implies that  but

but  could be consistent with

could be consistent with  being

greater or less than one. But recall that our assumption is that the unemployed consumer is

assumed to behave according to the perfect foresight model with human wealth equal to zero.

We must therefore impose the RIC in order to obtain a nondegenerate solution. We therefore

impose the RIC.

being

greater or less than one. But recall that our assumption is that the unemployed consumer is

assumed to behave according to the perfect foresight model with human wealth equal to zero.

We must therefore impose the RIC in order to obtain a nondegenerate solution. We therefore

impose the RIC.

For any finite horizon, human wealth is finite, and there is a positive probability that income will be zero over the remainder of the horizon. This puts a strict bound on the extent to which consumers are willing to rely for current consumption upon future income that is unbounded in expectation (as the horizon extends) but potentially bounded in practice. In effect, the precautionary motive introduces a self-imposed borrowing constraint that prevents the (arbitrarily large) amount of future income from being something the consumer is willing to borrow against.

The consequence is that the limiting model (as  ) exhibits a solution with a unique

finite target

) exhibits a solution with a unique

finite target  so long as (12) holds, even if human wealth is infinite; in this case the

so long as (12) holds, even if human wealth is infinite; in this case the

locus is downward sloping (because

locus is downward sloping (because  ; see (31)) while the

; see (31)) while the

locus is upward sloping (as guaranteed by (12)). Thus, a target

locus is upward sloping (as guaranteed by (12)). Thus, a target  will

exist.

will

exist.

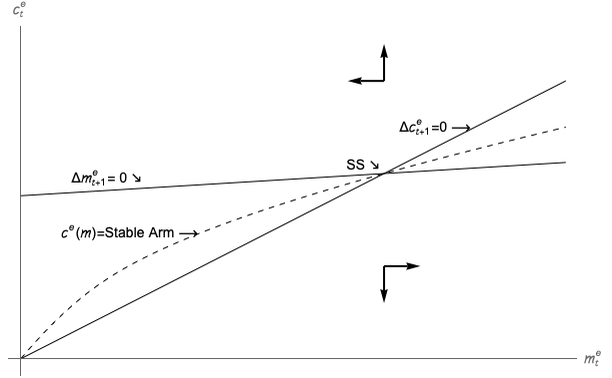

Figure 1 presents the phase diagram.

The  locus, given in (31), indicates, for a given level of

locus, given in (31), indicates, for a given level of  , how much

consumption

, how much

consumption  would be exactly the right amount to leave

would be exactly the right amount to leave  unchanged. Call

this the ‘permanently sustainable consumption locus,’ or for short ‘sustainable

consumption.’17

For any given

unchanged. Call

this the ‘permanently sustainable consumption locus,’ or for short ‘sustainable

consumption.’17

For any given  , consuming an amount less than the ‘sustainable’ level will cause wealth to

rise (and conversely for points above

, consuming an amount less than the ‘sustainable’ level will cause wealth to

rise (and conversely for points above  ). This provides the logic for the horizontal

arrows of motion in the diagram: Above the sustainable consumption locus they point left,

and below they point right.

). This provides the logic for the horizontal

arrows of motion in the diagram: Above the sustainable consumption locus they point left,

and below they point right.

The intuition for the  locus (which comes from (29)) is a bit subtler. Take a point

on the

locus (which comes from (29)) is a bit subtler. Take a point

on the  locus, and consider how things would change if

locus, and consider how things would change if  were a bit higher at the

same

were a bit higher at the

same  . Recall that the growth rate of consumption consistent with the Euler equation (11)

depends on the amount by which consumption will fall if the bad state is realized,

. Recall that the growth rate of consumption consistent with the Euler equation (11)

depends on the amount by which consumption will fall if the bad state is realized,

. But

. But  so at the same

so at the same  but a greater

but a greater  ,

,  will

be larger. If

will

be larger. If  were to remain unchanged, then with the larger

were to remain unchanged, then with the larger  the ratio

the ratio

would be smaller.

would be smaller.

The consequences of this are easiest to see in the logarithmic case whose consumption

growth equation is derived in (18), which tells us that  , which

directly implies that the lower

, which

directly implies that the lower  will yield a lower

will yield a lower  . That is, for any point to the

right of the

. That is, for any point to the

right of the  locus, the growth rate of consumption will be lower than at the

corresonding point on the locus. Since on the locus, growth was zero, this means that to the

right of the locus,

locus, the growth rate of consumption will be lower than at the

corresonding point on the locus. Since on the locus, growth was zero, this means that to the

right of the locus,  is declining (hence the down arrow in the phase diagram). Reciprocally,

for any point to the left of

is declining (hence the down arrow in the phase diagram). Reciprocally,

for any point to the left of  , the Euler equation implies that consumption will

rise.

, the Euler equation implies that consumption will

rise.

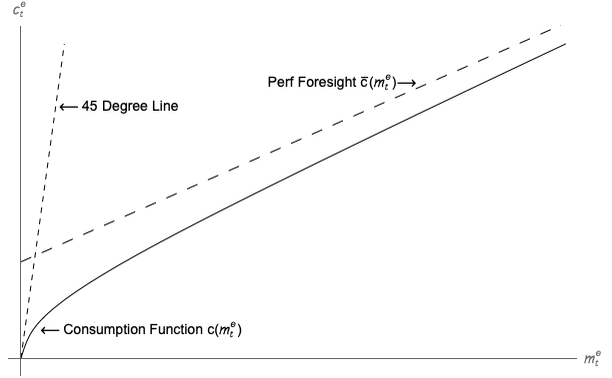

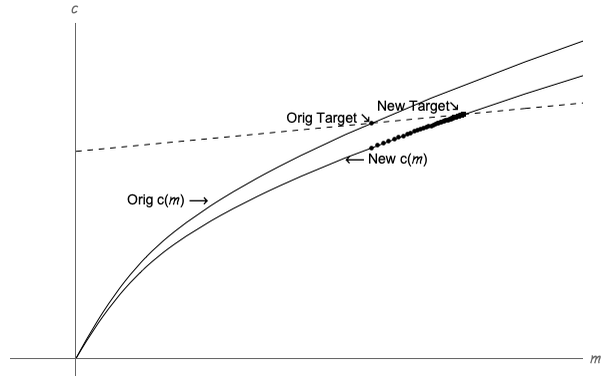

The next figure shows the optimal consumption function  for an employed consumer

(dropping the

for an employed consumer

(dropping the  superscript to reduce clutter). This is actually just the stable arm in the

phase diagram. (Think about why). Also plotted are the 45 degree line along which

superscript to reduce clutter). This is actually just the stable arm in the

phase diagram. (Think about why). Also plotted are the 45 degree line along which  as well as the function

as well as the function

| (34) |

where

| (35) |

is the level of (normalized) human wealth.  is the solution to a perfect foresight

problem in which income grows by the factor

is the solution to a perfect foresight

problem in which income grows by the factor  ; it is depicted in order to

introduce a final fact: As wealth approaches infinity, the solution to the problem

with uncertain labor income approaches arbitrarily close to the perfect foresight

solution.18

; it is depicted in order to

introduce a final fact: As wealth approaches infinity, the solution to the problem

with uncertain labor income approaches arbitrarily close to the perfect foresight

solution.18

Note that  is concave.19

That is, the marginal propensity to consume

is concave.19

That is, the marginal propensity to consume  is higher at low levels of

is higher at low levels of

. This is because of the increase in the intensity of the precautionary motive as resources

. This is because of the increase in the intensity of the precautionary motive as resources

decline; the consequences of becoming unemployed with little wealth are very painful. The

MPC is high at low levels of

decline; the consequences of becoming unemployed with little wealth are very painful. The

MPC is high at low levels of  because at low levels of

because at low levels of  the relaxation in the intensity of

the precautionary motive with each extra bit of

the relaxation in the intensity of

the precautionary motive with each extra bit of  is quite large (Kimball (1990)). This

diminution in the precautionary motive translates into an increase in consumption; for

is quite large (Kimball (1990)). This

diminution in the precautionary motive translates into an increase in consumption; for

-poor consumers even a modest increase in

-poor consumers even a modest increase in  can give a substantial boost to

can give a substantial boost to

.

.

This point is clearest as  approaches zero. Note that the consumption function always

remains below the 45 degree line. This is because if the consumer were to spend all his

resources in period

approaches zero. Note that the consumption function always

remains below the 45 degree line. This is because if the consumer were to spend all his

resources in period  ,

,  , then if he became unemployed next period he

would have

, then if he became unemployed next period he

would have  which would induce

which would induce  ,

yielding negative infinite utility. Thus the consumer will never spend all of his

resources - he will always leave at least a little bit for next period in case of disaster

(unemployment).20

,

yielding negative infinite utility. Thus the consumer will never spend all of his

resources - he will always leave at least a little bit for next period in case of disaster

(unemployment).20

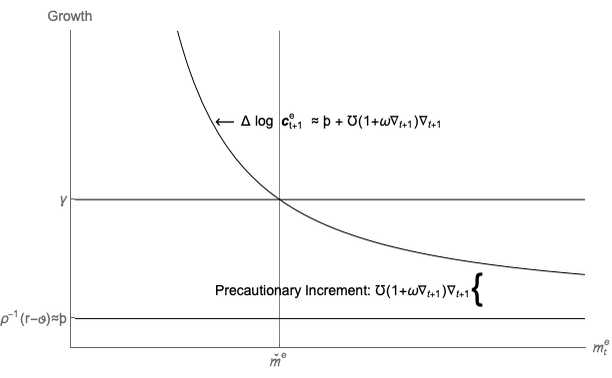

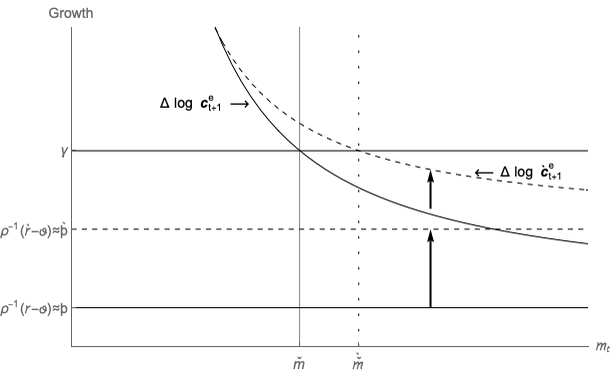

The next figure (‘the growth diagram’) illustrates some of the same points in a different way.

It depicts the growth rate of consumption as a function of  . Since

. Since  , the GIC

, the GIC for

this model implies:

for

this model implies:

| (36) |

a condition that can be visually verified for our benchmark calibration in figure 3. Now

multiply both sides of (11) by  , obtaining

, obtaining

![( e ) { [( e ) ρ ] }1∕ρ

ct+1 1∕ρ ct+1-

cet = (Rβ) 1 + ℧ cut+1 − 1

e −1

Δ log ct+1 ≈ ρ (r − τ ) + ℧ ∇t+1,](TractableBufferStock273x.svg) | (37) |

where the last line uses the same (dubious) approximations used to obtain (17).21

Thus consumption growth is equal to what it would be in the absence of uncertainty, plus a

precautionary term. Furthermore, the precautionary contribution will become arbitrarily large

as  because

because  approaches zero as

approaches zero as  . Sure

enough, figure 3 shows that as

. Sure

enough, figure 3 shows that as  gets low, expected consumption growth gets very

large.

gets low, expected consumption growth gets very

large.

Next, note that the point where the consumption growth locus meets the income growth

line is labelled  . This is because the place where consumption growth is equal to income

growth is at the target value of

. This is because the place where consumption growth is equal to income

growth is at the target value of  .

.

We are finally in position to get an intuitive understanding of how the model works, and why there is a target wealth ratio. On the one hand, consumers are growth-impatient. This prevents their wealth-to-income ratio from heading off to infinity. On the other hand, consumers have a precautionary motive that intensifies more and more as the level of wealth gets lower and lower. At some point the precautionary motive gets strong enough to counterbalance impatience. The point where impatience matches prudence defines the target wealth-to-income ratio.

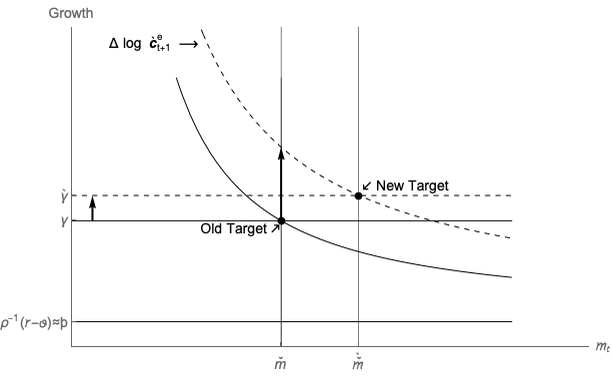

Now consider the results of increasing the interest rate to  , depicted in figure 4.

Obviously the perfect foresight consumption growth locus will shift up, to

, depicted in figure 4.

Obviously the perfect foresight consumption growth locus will shift up, to  ,

inducing a corresponding increase in the expected consumption growth locus. But we have not

changed the expected growth rate of income. It is clear from the figure, therefore, that the new

target level of cash-on-hand

,

inducing a corresponding increase in the expected consumption growth locus. But we have not

changed the expected growth rate of income. It is clear from the figure, therefore, that the new

target level of cash-on-hand  will be greater than the original target. That is, an increase

in the interest rate increases the target level of wealth, as would be expected on intuitive

grounds.

will be greater than the original target. That is, an increase

in the interest rate increases the target level of wealth, as would be expected on intuitive

grounds.

The next exercise is an increase in the risk of unemployment  The principal

effect we are interested in is the upward shift in the expected consumption growth

locus to

The principal

effect we are interested in is the upward shift in the expected consumption growth

locus to  . If the household starts at the original target level of resources

. If the household starts at the original target level of resources  ,

the size of the upward shift at that point is captured by the arrow orginating at

,

the size of the upward shift at that point is captured by the arrow orginating at

.

.

In the absence of other consequences of the rise in  , the effect on the target level

of

, the effect on the target level

of  would be unambiguously positive. However, recall our adjustment to the

growth rate conditional upon employment, (9); this induces the shift in the income

growth locus to

would be unambiguously positive. However, recall our adjustment to the

growth rate conditional upon employment, (9); this induces the shift in the income

growth locus to  which has an offsetting effect on the target

which has an offsetting effect on the target  ratio. Under

our benchmark parameter values, the target value of

ratio. Under

our benchmark parameter values, the target value of  is higher than before the

increase in risk even after accounting for the effect of higher

is higher than before the

increase in risk even after accounting for the effect of higher  , but in principle it is

possible for the

, but in principle it is

possible for the  effect to dominate the direct effect. Note, however, that even if the

target value of

effect to dominate the direct effect. Note, however, that even if the

target value of  is lower, it is possible that the saving rate will be higher; this is

possible because the faster rate of

is lower, it is possible that the saving rate will be higher; this is

possible because the faster rate of  makes a given saving rate translate into a lower

ratio of wealth to income. In any case, the most useful calibrations of the model are

those for which an increase in uncertainty results in either an increase in the saving

rate or an increase in the target ratio of resources to permanent income. This is

partly because our intent is to use the model to illustate the general features of

precautionary behavior, including the qualitative effects of an increase in the magnitude

of transitory shocks, which unambiguously increase both target

makes a given saving rate translate into a lower

ratio of wealth to income. In any case, the most useful calibrations of the model are

those for which an increase in uncertainty results in either an increase in the saving

rate or an increase in the target ratio of resources to permanent income. This is

partly because our intent is to use the model to illustate the general features of

precautionary behavior, including the qualitative effects of an increase in the magnitude

of transitory shocks, which unambiguously increase both target  and saving

rates.

and saving

rates.

Figures 3 and 4 show that, so long as consumers are impatient, the steady state growth rate of consumption will be equal to the steady-state growth rate of income,

| (38) |

Yet the approximate Euler equation for consumption growth, (37), does not contain any term explicitly involving income growth; in the logarithmic utility case, for example, the expression is

| (39) |

How can we reconcile these two expressions for consumption growth? Only by

realizing that the size of the precautionary term  is endogenous: It depends on

is endogenous: It depends on

. Indeed, we can solve (38) and (39) to determine that in steady-state we must

have

. Indeed, we can solve (38) and (39) to determine that in steady-state we must

have

| (40) |

We can use this equation to understand the relationship between parameters and

steady-state levels of wealth, by noting that  is a downward-sloping function of

is a downward-sloping function of  (see figure 3 again). This is because at low levels of current wealth, much of the spending of

employed consumers is financed by their current income. If they lose that income, they will

have no choice but to cut consumption drastically; this is reflected in a large value of

(see figure 3 again). This is because at low levels of current wealth, much of the spending of

employed consumers is financed by their current income. If they lose that income, they will

have no choice but to cut consumption drastically; this is reflected in a large value of

.

.

For example, an increase in the growth rate of income implies that the RHS of equation (40)

increases. The new target level of  must be lower, because lower wealth induces greater

consumption risk and a corresponding increase in the LHS of (40). This is how the human

wealth effect works in this framework: Consumers who anticipate faster income growth will

hold less market wealth.

must be lower, because lower wealth induces greater

consumption risk and a corresponding increase in the LHS of (40). This is how the human

wealth effect works in this framework: Consumers who anticipate faster income growth will

hold less market wealth.

The fact that consumption growth equals income growth in the steady-state poses major

problems for empirical attempts to estimate the Euler equation. To see why, suppose we had a

collection of countries indexed by  , identical in all respects except that they have different

interest rates

, identical in all respects except that they have different

interest rates  . Then in the spirit of Hall (1988), one might be tempted to estimate an

equation:

. Then in the spirit of Hall (1988), one might be tempted to estimate an

equation:

| (41) |

and to interpret the coefficient estimate on  as an indication of the value of

as an indication of the value of  .

.

But suppose that all of these countries contained impatient consumers and

were in their steady-states where  . Suppose further that all

countries had the same steady-state income growth rate and unemployment

rate.22

Then the regression equation would return the estimates

. Suppose further that all

countries had the same steady-state income growth rate and unemployment

rate.22

Then the regression equation would return the estimates

| (42) |

The econometric problem here is that there is an omitted variable from the regression

specification, the  term, which is (perfectly) correlated with the included variable

term, which is (perfectly) correlated with the included variable

. Thus, Euler equation estimation cannot be expected to return an unbiased

estimate of

. Thus, Euler equation estimation cannot be expected to return an unbiased

estimate of  . For much more on this problem, see Carroll (2001). For empirical

evidence that the problem is important in macroeconomic practice, see Parker and

Preston (2005).

. For much more on this problem, see Carroll (2001). For empirical

evidence that the problem is important in macroeconomic practice, see Parker and

Preston (2005).

We now consider a final experiment: A decrease in the time preference rate. To reduce

clutter, we drop the  locus from the phase diagram from Figure 1, and

everywhere drop

locus from the phase diagram from Figure 1, and

everywhere drop  the superscripts. (In exam questions, a figure like this might be

referred to as the ‘simplified consumption phase diagram’ or just ‘the consumption

diagram’).

the superscripts. (In exam questions, a figure like this might be

referred to as the ‘simplified consumption phase diagram’ or just ‘the consumption

diagram’).

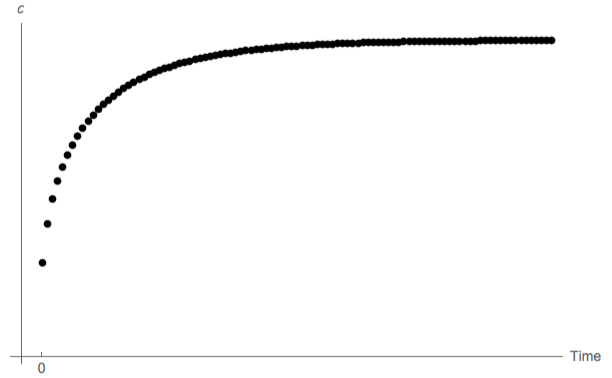

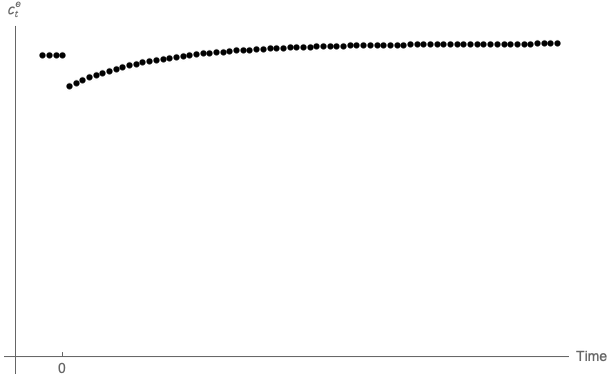

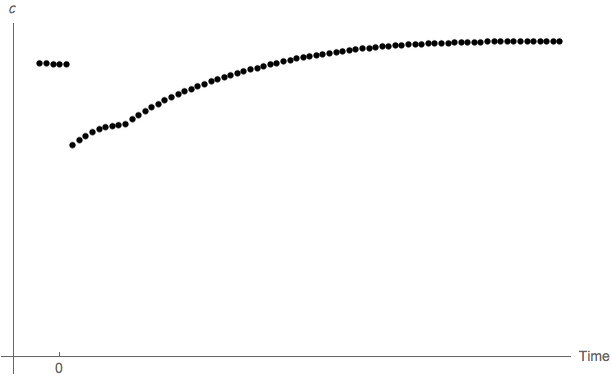

Figure 6 depicts the effect on the employed consumer’s spending by showing

each successive point in time as a dot. Starting at time 0 from the steady-state

level of consumption, the decrease in the future discounting rate (an increase in

patience) causes an instantaneous drop in the level of consumption. Starting from this

diminished base, consumption growth is subsequently faster than before the drop in

.23

.23

Eventually consumption approaches its new, higher equilibrium ratio to permanent

income at a new, higher level of equilibrium  . This higher level of consumption is

financed in the long run by the higher interest income earned on the higher level of

wealth.

. This higher level of consumption is

financed in the long run by the higher interest income earned on the higher level of

wealth.

Note again, however, that equilibrium steady-state consumption growth is still equal to the

growth rate of income (this follows from the fact that there is a steady-state level for the ratio

of consumption to income,  ). This means that the higher level of wealth in equilibrium

ends up being precisely enough to reduce the precautionary term by an amount

that exactly offsets the fact that the

). This means that the higher level of wealth in equilibrium

ends up being precisely enough to reduce the precautionary term by an amount

that exactly offsets the fact that the  term in the Euler equation is now

smaller.

term in the Euler equation is now

smaller.

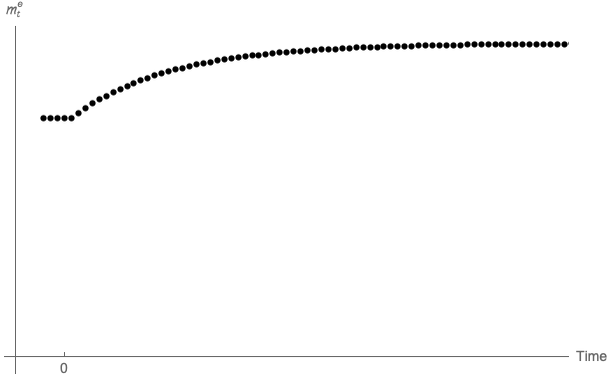

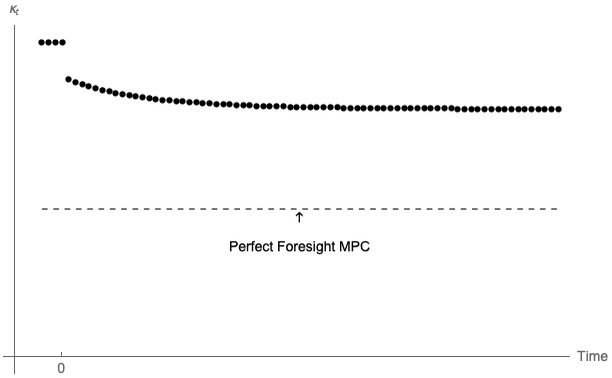

The final figures depict the time paths of consumption, market wealth, and the marginal

propensity to consume  following the decline in

following the decline in  . These are implicit in the phase

diagram analysis, but the dots in these two new diagrams are spread out evenly over time

to give a sense of the time scale over which the model adjusts toward the steady

state.

. These are implicit in the phase

diagram analysis, but the dots in these two new diagrams are spread out evenly over time

to give a sense of the time scale over which the model adjusts toward the steady

state.

Loosely following Carroll and Jeanne (2009) (with some simplifications), this section extends

the model to analyze macroeconomic dynamics in a small open economy with a large number

of individuals, where the population statistics reflect the fulfillment of individual consumers’

ex ante expectations; for example, exactly proportion  of households who are

employed in period

of households who are

employed in period  become ‘unemployed’ before

become ‘unemployed’ before  , so that the aggregate labor

supply of the ‘active’ (still employed) members of a generation evolves according

to

, so that the aggregate labor

supply of the ‘active’ (still employed) members of a generation evolves according

to

| (43) |

where the first subscript denotes the date being examined and the second denotes the period of birth of the generation being examined.

We make strong assumptions that permit straightforward aggregation. The first such assumption is that newly unemployed households immediately migrate out of the country (think of British retirees moving to southern Spain).24 This means that macroeconomic variables will reflect only the circumstances of employed consumers, rather than a blend of the employed and the unemployed.

Each person is part of a single ‘generation’ of households born at the same time, and every

new generation is larger by the factor  than the newborn generation in the previous

period:

than the newborn generation in the previous

period:

| (44) |

We assume that total production by the (surviving) members of a generation grows by the

factor  every period. If total production is to grow despite a shrinking number of surviving

members of the generation, production per active capita must grow by

every period. If total production is to grow despite a shrinking number of surviving

members of the generation, production per active capita must grow by  as per

(9).

as per

(9).

Consider the economy in some period 0 in which the size of the newborn population and the

wage rate have been normalized to  . If the economy has existed for

. If the economy has existed for  periods (where

periods (where  is a negative number, indicating that the economy was created

before period 0), the ratio of the total population to the population of newborns will

be

is a negative number, indicating that the economy was created

before period 0), the ratio of the total population to the population of newborns will

be

| (45) |

whose limit is a finite number so long as  , which we require.

, which we require.

Relative to the labor income of period 0’s newborn cohort ( ), the total labor

income in period 0 of the generation born in period

), the total labor

income in period 0 of the generation born in period  is

is  ; the sum of the incomes of

all of the two-period-old individuals is

; the sum of the incomes of

all of the two-period-old individuals is  , and so on; total labor income for all generations

in the economy in period 0 is

, and so on; total labor income for all generations

in the economy in period 0 is

| (46) |

which is finite so long as either population growth is positive  (which we will assume)

or the economy has existed for a finite period of time (

(which we will assume)

or the economy has existed for a finite period of time ( ). In either case, the

proportion of aggregate income accounted for by a generation born at any specific

moment declines toward zero as time passes (old generations never die, they just fade

away).

). In either case, the

proportion of aggregate income accounted for by a generation born at any specific

moment declines toward zero as time passes (old generations never die, they just fade

away).

In the balanced growth equilibrium, the growth factor for aggregate population will

therefore be  and output per capita will increase by

and output per capita will increase by  per period. Total labor income

therefore grows by

per period. Total labor income

therefore grows by

We now examine this model under two assumptions about the initial ‘stake’ of newborns in the economy. (We use ‘stake’ to designate a transfer received by newborns). This is explicitly not an inheritance, as we have assumed that individuals have no bequest motive and newborns are unrelated to anyone in the existing population. Our motivation is to make the model more tractable, rather than to represent an important feature of the real world; we later perform simulations designed to show that the characteristics of the model with no ‘stake’ are qualitatively and quantitatively similar to those of the more tractable model with the ‘stake’ that makes the model tractable.

We first consider a version of the model in which an exogenous redistribution program guarantees that the behavior of employed households can be understood by analyzing the actions of a “representative employed agent.”

If a benevolent source outside the economy were to provide every newborn with an initial

transfer upon birth of size  , then the newborn’s total monetary resources would

be

, then the newborn’s total monetary resources would

be

|

Thus, per-capita market resources for members of the newborn generation would be exactly equal to the target level of market resources for a person anticipating the future path of labor income that the members of the newborn generation actually anticipate (which is the same as the future path anticipated by all other generations as well).

If such a transfer policy had been in place forever, the economy at every point in time would

consist of employed households whose consumption had been equal to its steady-state value

for their whole lives. That is, every individual agent in this economy would be identical in

their ratio of consumption, market resources, etc. to permanent labor income. The behavior of

any individual would therefore be fully captured by the behavior of a representative employed

agent.25

for their whole lives. That is, every individual agent in this economy would be identical in

their ratio of consumption, market resources, etc. to permanent labor income. The behavior of

any individual would therefore be fully captured by the behavior of a representative employed

agent.25

The foregoing scenario assumed that the ‘stake’ is provided by a mysterious ‘benevolent source outside the economy.’ Fortunately, there is an easy way to eliminate this problematic assumption: Assume that the stakes are financed by a wage tax.

The size of the required tax rate is calculated as follows. The total size of the resources transferred to the newborn generation must be

| (47) |

where

| (48) |

is the after-tax wage rate for the economy as a whole (and  is the steady state target ratio

of bank balances to after-tax wages).

is the steady state target ratio

of bank balances to after-tax wages).

From (46), the ratio of total aggregate labor income to the labor income of the newborn generation is

| (49) |

so the aggregate wage tax rate required to finance a ‘stake’ of size  for newborns is given

by

for newborns is given

by

| (50) |

Note, however, that in an economy where this tax has existed forever, the consequence

of the tax is effectively just a permanent reduction in after-tax labor income by

proportion  , compared to its value in the absence of the tax. Given the homotheticity of

the model, a permanent rescaling by a constant factor leaves the scaled version of

the individual’s problem (and its solution) unchanged. Thus we can conclude not

only that a representative agent exists in this economy, but that the steady-state

characteristics of the representative agent’s problem are identical (in ratio form) to the

characteristics of the unrescaled individual’s problem; that is,

, compared to its value in the absence of the tax. Given the homotheticity of

the model, a permanent rescaling by a constant factor leaves the scaled version of

the individual’s problem (and its solution) unchanged. Thus we can conclude not

only that a representative agent exists in this economy, but that the steady-state

characteristics of the representative agent’s problem are identical (in ratio form) to the

characteristics of the unrescaled individual’s problem; that is,  ,

,  , and so

on.

, and so

on.

Matters are not much more complicated outside the balanced growth steady state, so long

as we assume that the government always transfers the amount  to newborn households,

financed by the tax

to newborn households,

financed by the tax  derived above. Consider, for example, an economy that was in

steady-state equilibrium leading up to period

derived above. Consider, for example, an economy that was in

steady-state equilibrium leading up to period  , and at the beginning of

, and at the beginning of  there is a sudden

realization that future growth rates will be higher than those anticipated and experienced in

the past:

there is a sudden

realization that future growth rates will be higher than those anticipated and experienced in

the past:  after

after  . Since expected growth rates affect

. Since expected growth rates affect  , the tax rate must be

immediately and permanently changed so that the generations born after

, the tax rate must be

immediately and permanently changed so that the generations born after  receive

a ‘stake’ of the proper new size. This change in

receive

a ‘stake’ of the proper new size. This change in  has two consequences for the

generations that survive from periods prior to

has two consequences for the

generations that survive from periods prior to  . Under the old tax rate, they would have

experienced

. Under the old tax rate, they would have

experienced  ; the change in expectations has no effect on

; the change in expectations has no effect on  or

or  but

changes the tax rate to

but

changes the tax rate to  . Thus these households will have an actual resource ratio

that differs from its new target value,

. Thus these households will have an actual resource ratio

that differs from its new target value,  , both because the after-tax income

scaling factor has changed and because the target ratio has changed from

, both because the after-tax income

scaling factor has changed and because the target ratio has changed from  to

to

.

.

However, if we started out in steady-state, the ratio problem of every member of the continuing-employed population is identical to that of every other such household (though, again, their masses differ depending on age, etc); as a result, the dynamics of the economy are fully captured by keeping track of the relative weights in the economy of the (gradually diminishing) ‘representative shocked agent’ and the (gradually increasing) ‘representative new agent’ whose behavior is locked at its steady-state value.26

Figure 10 illustrates the dynamics in this economy using an experiment identical to one

explored above for the individual’s problem: In period 0 there is a one-off decline in the future

discounting rate (assuming the economy was in steady state before period 0). In the

previous model, each individual consumer’s consumption function shifted down, and

consumption experienced a discrete jump downward, because the agent became more

impatient. Here, there is a modest further effect: With more-patient consumers,

the tax rate that the government sets to finance a transfer of  to the newborns

must be larger (so that the ratio of initial assets to after-tax income is smaller).

Qualitatively, the dynamics are indistinguishable from the individual consumer’s dynamics

obtainable without working through the extra complication involved in accounting for the

‘stakes.’

to the newborns

must be larger (so that the ratio of initial assets to after-tax income is smaller).

Qualitatively, the dynamics are indistinguishable from the individual consumer’s dynamics

obtainable without working through the extra complication involved in accounting for the

‘stakes.’

The polar alternative to assuming that newborns get a ‘stake’ is to assume that newborns enter the economy with zero assets. Analysis of this version of the model must be performed using simulation methods, because households of different ages will have different levels of assets. (With a concave and nonanalytical consumption function, analytical aggregation cannot be performed.)

Our simulation procedure assumes that at date 0 the economy has existed

forever (so that the age distribution of relative populations and productivities are

at their steady-state values), but saving has been impossible prior to period

0.27

With everyone’s  , the ratio of market resources to permanent labor income is the same

for all individuals:

, the ratio of market resources to permanent labor income is the same

for all individuals:

| (51) |

The consumption ratio in period 0 is therefore  for every household (regardless of age),

while the level of total labor income for a generation that is

for every household (regardless of age),

while the level of total labor income for a generation that is  periods old is

periods old is

.28

The population of such workers is

.28

The population of such workers is  , so aggregate consumption will be given by the

per-capita consumption ratio, multiplied by the per-capita level of permanent income,

multiplied by the population of workers still alive:

, so aggregate consumption will be given by the

per-capita consumption ratio, multiplied by the per-capita level of permanent income,

multiplied by the population of workers still alive:

| (52) |

The longer a generation lives, the more time it will have had to save toward its target level of wealth; but newborns always begin life with no assets. After period 0, therefore, age-heterogeneity in assets and consumption ratios creeps into the population.

The foregoing discussion contains (in some cases implicitly) all the assumptions necessary to

conduct a simulation of this economy. Figure 11 shows the path of the ratio  starting from period 0 for an economy under our benchmark parameterization that generated

our earlier figures. The only extra parameter required beyond those used before is

starting from period 0 for an economy under our benchmark parameterization that generated

our earlier figures. The only extra parameter required beyond those used before is  ; we

choose

; we

choose  corresponding roughly to the postwar population growth rate in the United

States.

corresponding roughly to the postwar population growth rate in the United

States.

beginCDC

We consider now the consequences if the government creates a balanced-budget partial ‘unemployment insurance’ system. This system operates by imposing a labor income tax on the employed in order to finance transfers to the unemployed.29

Our definition of partial insurance starts by assuming that the ‘true’ labor income process is

the one specified above, but the government interferes with this process by selecting a

constant proportion  of the newly unemployed in each period who will be guaranteed

a ‘wage-indexed unemployment benefit’ that yields the same income they would

have received if they had not become unemployed. The lucky recipients of these

payments, however, are subject to a risk of termination from the unemployment

insurance program that matches the risk of becoming unemployed for the still-employed

consumers.

of the newly unemployed in each period who will be guaranteed

a ‘wage-indexed unemployment benefit’ that yields the same income they would

have received if they had not become unemployed. The lucky recipients of these

payments, however, are subject to a risk of termination from the unemployment

insurance program that matches the risk of becoming unemployed for the still-employed

consumers.

Under these circumstances, the household does not care whether it remains employed, or becomes unemployed but is selected for the unemployment insurance program: The dynamics of idiosyncratic future income are identical in the two cases.

Each generation finances its own unemployment insurance (this assumption is made to keep

the model as transparent as possible; it would not change things much to have the UI system

financed by the general government, but this would require some extra notation and

derivations, and discussion of essentially inconsequential intergenerational aspects of

unemployment insurance). The government sets the overall uninsurance rate  (‘uninsurance’

rather than ‘insurance’ rate because

(‘uninsurance’

rather than ‘insurance’ rate because  will be ‘no uninsurance’ or perfect insurance,

while

will be ‘no uninsurance’ or perfect insurance,

while  will be no insurance) and enforces exogenous taxation among the ‘truly

employed’ in the generation in such a way as to yield a modified ‘post-tax-and-transfer’

growth profile consistent with substituting

will be no insurance) and enforces exogenous taxation among the ‘truly

employed’ in the generation in such a way as to yield a modified ‘post-tax-and-transfer’

growth profile consistent with substituting  for

for  in the derivations above,

where

in the derivations above,

where

| (53) |

and  guarantees that the insurance program results in a reduction of idiosyncratic

income risk.

guarantees that the insurance program results in a reduction of idiosyncratic

income risk.

Substituting  for

for  in the prior derivations, this scheme is consistent with the

generational budget constraint because, as noted above, the individual income growth process

was constructed so that the present discounted value of income remains invariant to the size of

in the prior derivations, this scheme is consistent with the

generational budget constraint because, as noted above, the individual income growth process

was constructed so that the present discounted value of income remains invariant to the size of

, and the aggregate income of a generation grows by

, and the aggregate income of a generation grows by  regardless of the underlying

idiosyncratic unemployment risk.

regardless of the underlying

idiosyncratic unemployment risk.

This scheme is attractive because in practice it simply requires solving the model specified

above for a different value of  . This will make solution and simulation of the model

particularly simple.

. This will make solution and simulation of the model

particularly simple.

In addition to the consumption function, the solution procedure

produces an estimate of the representative employed agent’s value

function.30

Value depends on current resources, but also (numerically) on all of the parameters in the

calibration of the model. We are particularly interested in how value relates to expected labor

productivity growth  , to the ‘true’ unemployment risk

, to the ‘true’ unemployment risk  , and to the generosity of the

unemployment insurance program

, and to the generosity of the

unemployment insurance program  . Writing

. Writing

| (54) |

(where we separate the state variable  from the parameters using a semicolon) we can

investigate a variety of interesting questions. Some examples:

from the parameters using a semicolon) we can

investigate a variety of interesting questions. Some examples:

such that

such that

| (55) |

. The cost is increased unemployment risk

. The cost is increased unemployment risk  . For a given generosity of

unemployment insurance, how much extra growth is necessary to offset the utility cost

of greater risk? That is, supposing the relationship between

. For a given generosity of

unemployment insurance, how much extra growth is necessary to offset the utility cost

of greater risk? That is, supposing the relationship between  and

and  is

indexed by a parameter

is

indexed by a parameter  , e.g.

, e.g.  , what is the

, what is the  for

which

for

which

| (56) |

?

?Many more such questions can be imagined. endCDC

Using from MathFacts the second-order and then the first-order Taylor approximations

![[TaylorTwo ]](TractableBufferStock431x.svg)

and then

and then ![[TaylorOne ]](TractableBufferStock433x.svg)

,

the expression in braces in (11) can be rewritten

,

the expression in braces in (11) can be rewritten

![{ [( ce )ρ ]}1 ∕ρ { [( cu + ce − cu ) ρ ]}1∕ρ

1 + ℧ -t+u1- − 1 = 1 + ℧ -t+1----t+u1----t+1 − 1

ct+1 ct+1

= {1 + ℧ [(1 + ∇ )ρ − 1]}1∕ρ

{ [ t+1 ]}

≈ 1 + ℧ 1 + ρ∇t+1 + ρ(∇t+1 )2ω − 1 1∕ρ

{ }1∕ρ

= 1 + ρ℧ (∇t+1 + (∇t+1)2ω )

≈ 1 + ℧ (1 + ∇ ω) ∇ ,

t+1 t+1](TractableBufferStock435x.svg) |

which leads directly to (17) in the main text.

At a steady-state value of  , both

, both  and

and  hold (equations (29) and (31));

for convenience defining

hold (equations (29) and (31));

for convenience defining  ,

,

| (57) |

But since  is a positive number, at

is a positive number, at  the

the  locus’s

value is

locus’s

value is  while the value of the

while the value of the  locus is zero, the two loci

can intersect for a positive

locus is zero, the two loci

can intersect for a positive  only if the slope of the

only if the slope of the  locus is

greater:31

locus is

greater:31

| (58) |

which is equivalent to

| (59) |

where the LHS is (proportional to) the slope of  and the RHS is (proportional to) the

slope of

and the RHS is (proportional to) the

slope of  . beginCDC

. beginCDC

It is not totally obvious why these are equivalent, so here’s the derivation.

| (60) |

endCDC

For any fixed  and

and  and

and  we can find some

we can find some  for which

for which  , and

using this

, and

using this  it turns out to be useful to rewrite

it turns out to be useful to rewrite

| (61) |

Note for future use that (61) implies that whenever  , the FHWC

, the FHWC fails (‘human

wealth is infinite’) because

fails (‘human

wealth is infinite’) because  .

.

Multiplying both sides of (59) by  then substituting the expression for

then substituting the expression for  from (61) gives

from (61) gives

| (62) |

Since  and

and  (as guaranteed by the RIC), (62) is satisfied whenever the

FHWC

(as guaranteed by the RIC), (62) is satisfied whenever the

FHWC fails (

fails ( ) and

) and  . We now show that under these conditions,

. We now show that under these conditions,

.

.

from (19) is:

from (19) is:

| (63) |

but note that

| (64) |

and in the case where  ,

,  must also be 1, implying that

must also be 1, implying that  (the

RIC) so that

(the

RIC) so that  and so

and so  and hence

and hence  . The other interesting case is

when

. The other interesting case is

when  so that

so that  and

and  . In this case

. In this case

and so

and so  and so

and so  is even more positive so that

is even more positive so that  is even more

strongly

is even more

strongly  . Similar logic holds for any

. Similar logic holds for any  .

.

Thus, we can conclude that, when human wealth is infinite (that is, if  ), a target

), a target

will exist.

will exist.

In the case where human wealth is finite ( ), we need the RHS of (62) not merely to be

positive, but to exceed a specific positive number,

), we need the RHS of (62) not merely to be

positive, but to exceed a specific positive number,  :

:

![1∕ρ

κ(1 + ϖ ) > ((α − 1 )℧ ∕(1) − ℧ )

1∕ρ (α − 1)℧

(1 + ϖ ) > ---------

( κ (1 − ℧ )) ρ

(α-−-1)℧-

(1 + ϖ) > κ (1 − ℧ )

( ) ρ

(ÞÞÞ −ρ− 1)℧−1 = ϖ > (α-−-1)℧- − 1

ΦΦΦ κ (1 − ℧ )

[ ((α − 1)℧) ρ ]

(ÞÞÞ−ΦΦΦ ρ− 1) > ℧ --------- − 1

κ(1 − ℧)

−ρ [( (α − 1 )℧ ) ρ ]

ÞÞÞΦΦΦ > 1 + ℧ --------- − 1

( κ (1 − ℧ ) )

| | −1∕ρ

||{ [( ) ρ ]||}

ÞÞÞ < 1 + ℧ (α-−-1-)℧- − 1

ΦΦΦ || κ (1 − ℧) ||

|( ◟--------◝◜--------◞|)

≡χ](TractableBufferStock495x.svg) | (65) |

and the boundary will be the point at which this expression holds with equality.