The Distribution of Wealth and the MPC:

Implications of New European Data

February 11, 2014

The Distribution of Wealth and the MPC:

Implications of New European Data

February 11, 2014

_____________________________________________________________________________________

Abstract

Using new micro data on household wealth from fifteen European countries

(the Household Finance and Consumption Survey), we first document

substantial cross-country variation in how various measures of wealth are

distributed across individual households. Through the lens of a standard,

realistically calibrated model of buffer-stock saving with transitory and

permanent income shocks we then study how cross-country differences in the

wealth distribution and household income dynamics affect the marginal

propensity to consume out of transitory shocks (MPC). We find that the

aggregate consumption response ranges between 0.1 and 0.4 and is stronger (i) in

economies with large wealth inequality, where a larger proportion of households

has little wealth, (ii) under larger transitory income shocks and (iii) when we

consider households only using liquid assets (rather than net wealth) to smooth

consumption.

Marginal Propensity to Consume, Wealth Distribution, Liquid Assets, Cross-Country Comparisons, Household Finance and Consumption Survey

D12, D31, D91, E21

| PDF: | http://www.econ2.jhu.edu/people/ccarroll/papers/cstMPCxc.pdf |

| Slides: | http://www.econ2.jhu.edu/people/ccarroll/papers/cstMPCxc-Slides.pdf |

| Web: | http://www.econ2.jhu.edu/people/ccarroll/papers/cstMPCxc/ |

| Archive: | http://www.econ2.jhu.edu/people/ccarroll/papers/cstMPCxc.zip |

1Carroll: Department of Economics, Johns Hopkins University, Baltimore, MD, http://www.econ2.jhu.edu/people/ccarroll/, ccarroll@jhu.edu 2Slacalek: European Central Bank, Frankfurt am Main, Germany, http://www.slacalek.com/, jiri.slacalek@ecb.europa.eu 3Tokuoka: Ministry of Finance, Tokyo, Japan, kiichi.tokuoka@mof.go.jp

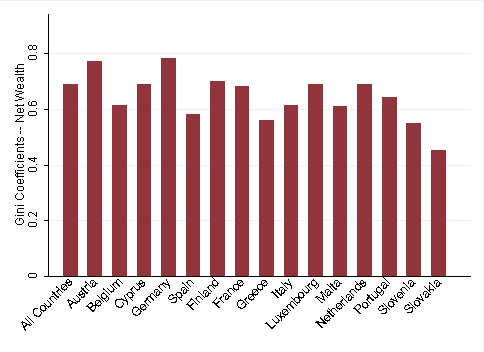

Source: The Eurosystem Household Finance and Consumption Survey.

Notes: The figure shows the Gini coefficient for net wealth, defined as the sum of real assets (including housing) and financial

assets, net of total liabilities. The data cover the following countries: Austria, Belgium, Cyprus, Germany, Spain, Finland, France,

Greece, Italy, Luxembourg, Malta, the Netherlands, Portugal, Slovenia and Slovakia. Reference year: mostly 2010; see Eurosystem

Household Finance and Consumption Network (2013b), Table 9.1. The Gini coefficient for ‘All Countries’ was calculated by

aggregating household-level data country by country using estimation weights (which give the number of households in the

population each observation represents).

Considerable evidence has recently confirmed the plausible implication of economic theory that low-wealth households should consume more out of a transitory shock to income than high-wealth households (that is, the Marginal Propensity to Consume is declining in wealth).2 Recent work by Carroll, Slacalek, and Tokuoka (2013b) (henceforth, CST) argues that when a standard buffer-stock model of consumption is calibrated to match the US wealth distribution, it yields MPCs that are consistent with the extensive empirical evidence that the MPC out of transitory shocks is very far from zero. (The model’s implied aggregate MPCs range from 0.2 to as high as 0.6, depending on which measure of wealth is matched).

This paper shows how the CST model can be adapted to the

various wealth distributions that have recently been measured for a

set of European countries in the newly released Household Finance

and Consumption Survey (HFCS). The HFCS indicates that wealth

inequality varies considerably across the fifteen European countries it

covers. (Figure 1 shows that the Gini coefficient ranges roughly between

0.45 and 0.8; the latter value broadly comparable with the data for the

US.3  4 )

4 )

Depending on the measure of wealth that is matched (total net worth or liquid assets), the interaction between the model’s concave consumption function and the distribution of wealth implies aggregate MPCs ranging from 0.1 to 0.4 in the European countries. The model’s prediction for MPCs in these European countries are somewhat lower than the version calibrated for the US because European households tend to hold more wealth than Americans and because wealth is more equally distributed in Europe than in the US.

We explore two aspects of heterogeneity: in the wealth distribution and income uncertainty. The wealth distribution affects the MPC through level and through inequality, as captured in the Gini coefficient. Countries in which households tend to hold less wealth respond more strongly to transitory income shocks. Similarly, countries with more pronounced wealth inequality have a higher aggregate MPC and also a larger dispersion of MPCs across households.

Household-level income dynamics affect the aggregate MPC mainly through the size of transitory shocks, against which households can better insure themselves than against permanent shocks. An increase in the variance of transitory shocks implies a more concave consumption function with a steeper slope close to the origin, and thus a higher value of the aggregate MPC.

Our research builds on the work from a number of streams: (i) measurement of the wealth distribution across countries,5 (ii) estimation of income dynamics at personal/household level,6 (iii) empirical work on estimating the MPC7 and (iv) calibration and solving models with heterogeneity.8

The paper proceeds as follows. Section 2 lays out the theoretical model. Section 3 presents key stylized facts on the wealth distribution in the new data from fifteen European countries. Section 4 presents the distribution of the MPCs across countries and households, implied by the model, and summarizes the relationships between the wealth distribution, income dynamics and the MPC. Section 5 concludes.

The model follows closely Carroll, Slacalek, and Tokuoka (2013b) and consists of the following components:

(‘Friedman/Buffer Stock’ income process,

FBS) with a permanent (

(‘Friedman/Buffer Stock’ income process,

FBS) with a permanent ( ) and a transitory (

) and a transitory ( ) idiosyncratic shock:

where

) idiosyncratic shock:

where  denotes the aggregate wage rate. The transitory component is:

where

denotes the aggregate wage rate. The transitory component is:

where  is the unemployment insurance payment when unemployed,

is the unemployment insurance payment when unemployed,

is the rate of tax collected to pay unemployment benefits,

is the rate of tax collected to pay unemployment benefits,  is time

worked per employee and

is time

worked per employee and  is white noise.

is white noise.

The motivation for this income process goes back to Friedman (1957). Vast empirical literature (see footnote 6) has since then investigated statistical properties of various measures of income in numerous datasets and concluded that the process (1)–(2) closely resembles the data and that both the transitory and the permanent (or highly persistent) component are important to capture actual income dynamics.

and are replaced with newborns earning permanent income equal

to the population mean. When the probability of dying is large

enough, it outweighs the effect of permanent shocks and ensures

that the ergodic distribution of income exists (and has a finite

variance).9

and are replaced with newborns earning permanent income equal

to the population mean. When the probability of dying is large

enough, it outweighs the effect of permanent shocks and ensures

that the ergodic distribution of income exists (and has a finite

variance).9

-Dist’ model of Carroll,

Slacalek, and Tokuoka (2013b), we assume that households in the

economy differ in time preference factors

-Dist’ model of Carroll,

Slacalek, and Tokuoka (2013b), we assume that households in the

economy differ in time preference factors  , which are distributed

uniformly between

, which are distributed

uniformly between  and

and  . We estimate

. We estimate  and

and  by

fitting the wealth Lorenz curve implied by the model to that in the

data:

by

fitting the wealth Lorenz curve implied by the model to that in the

data:

| (3) |

subject to the constraint that the aggregate wealth-to-output ratio in the

model matches the aggregate capital-to-output ratio from the perfect foresight

model.10

In the above we denote  and

and  the proportion of total wealth held by

the top

the proportion of total wealth held by

the top  percent of households in the model and in the data,

respectively.

percent of households in the model and in the data,

respectively.

Each household maximizes its lifetime expected discounted CRRA utility:

satisfy:

satisfy: . The three steps (5)–(7) in

the evolution of household’s market resources account for the probability of

dying

. The three steps (5)–(7) in

the evolution of household’s market resources account for the probability of

dying  , the depreciation factor for capital

, the depreciation factor for capital  and the interest rate

and the interest rate

, so that the effective interest rate is

, so that the effective interest rate is  . The production function is

Cobb–Douglas,

. The production function is

Cobb–Douglas,  , where

, where  is aggregate productivity,

is aggregate productivity,  is

capital,

is

capital,  is time worked per employee and

is time worked per employee and  is employment. The wage rate

and the interest rate are equal to the marginal product of labor and capital,

respectively.

is employment. The wage rate

and the interest rate are equal to the marginal product of labor and capital,

respectively.

A target wealth-to-permanent-income ratio exists if households are impatient enough in the sense that ‘the Death-Modified Growth Impatience Condition’ of Carroll, Slacalek, and Tokuoka (2013a) holds.11

The model is calibrated at the quarterly frequency following Carroll, Slacalek, and Tokuoka (2013b), Table 3 and the Journal of Economic Dynamics and Control (2010) volume on comparing solution methods for the Krusell and Smith (1998) model.12

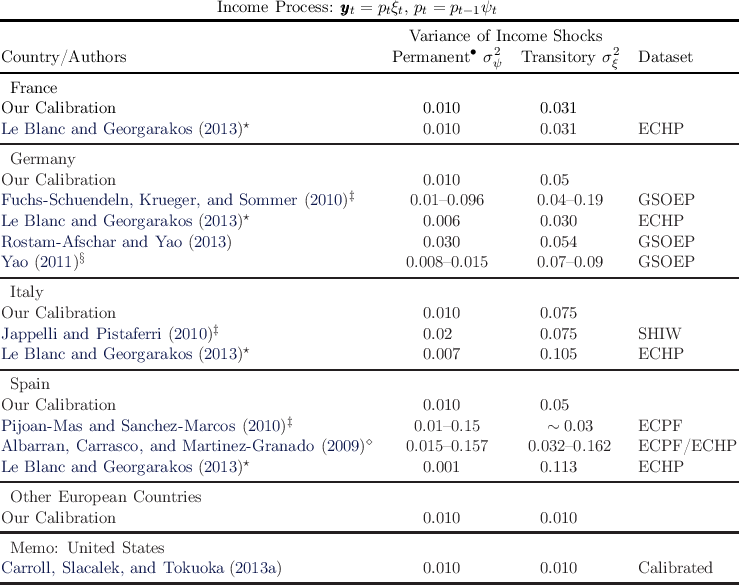

Notes: ECHP: European Community Household Panel, GSOEP: German Socio–Economic Panel, SHIW: Survey of

Household Income and Wealth, ECPF: Encuesta Continua de Presupuestos Familiares;  : For this calibration of other

parameters variance of permanent shocks cannot be increased much above 0.01 for the ‘Death-Modified Growth

Impatience Condition’ described in footnote 11 to be satisfied. (Results of section 4.3 below suggest the MPCs implied

by the model are quite robust to alternative calibrations of variance of income shocks.)

: For this calibration of other

parameters variance of permanent shocks cannot be increased much above 0.01 for the ‘Death-Modified Growth

Impatience Condition’ described in footnote 11 to be satisfied. (Results of section 4.3 below suggest the MPCs implied

by the model are quite robust to alternative calibrations of variance of income shocks.)  : See Table 5 in Le

Blanc and Georgarakos (2013),

: See Table 5 in Le

Blanc and Georgarakos (2013),  : See Table 7A–C in Review of Economic Dynamics (2010), pages 11–13,

: See Table 7A–C in Review of Economic Dynamics (2010), pages 11–13,  :

See Figures 3 and 4 in Albarran, Carrasco, and Martinez-Granado (2009), page 509.

:

See Figures 3 and 4 in Albarran, Carrasco, and Martinez-Granado (2009), page 509.  : Implied by Table 1 in

Yao (2011).

: Implied by Table 1 in

Yao (2011).

The calibration and estimation of the model here differs from that in Carroll, Slacalek, and Tokuoka (2013b) in two ways: The distribution of wealth (see section 3 below) and the parametrization of the income process. The estimates of the FBS income process for European countries, summarized in Table 1, are much scarcer than for the US; the key contributions are in the Review of Economic Dynamics (2010) volume on ‘Cross-Sectional Facts for Macroeconomists’ (which reports the evidence from Germany, Italy and Spain). The rows ‘Our Calibration’ display the values we use.13

We measure the wealth distribution using data from the Household Finance and Consumption Survey, a new cross-country comparable household-level dataset produced by euro area central banks.14 The recently released survey provides detailed information on balance sheets of more than 62,000 households from fifteen euro area countries and is thus an ideal source for cross-country comparisons of how various measures and components of wealth are distributed across households.

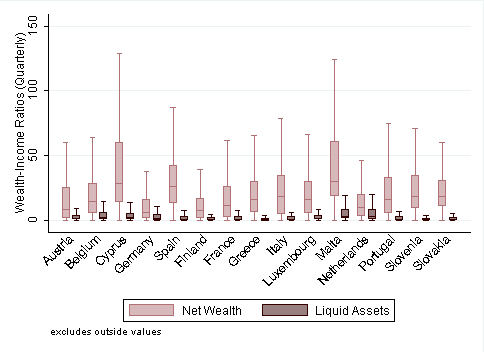

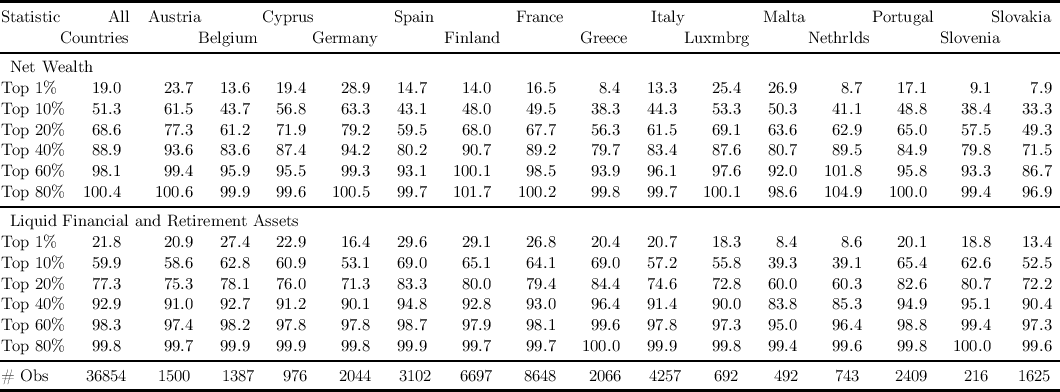

Figure 2 displays the distribution of wealth-to-permanent income ratios (see also Table 6 in the Appendix). Net wealth is defined as the sum of value of real and financial assets, net of total liabilities. Liquid financial and retirement assets are defined as the sum of value of deposits, mutual funds, non-self-employment business wealth, shares, managed accounts and voluntary private pensions/whole life insurance. We approximate permanent income by restricting the sample to households which in the survey respond that their current income equals roughly to their ‘normal’ income.

Several facts are relevant for our results below. First, substantial heterogeneity in ratios both across and within countries—up to the multiple of 100 or so of quarterly income—suggests that the MPCs will vary across individual households (because of concavity of the consumption function) and they will imply different reactions of aggregate consumption across countries.

Source: The Eurosystem Household Finance and Consumption Survey.

Notes: The figure shows a box plot with the lower adjacent value, the 25th percentile, the median, the 75th percentile

and the upper adjacent value. The adjacent values are the 25th percentile interquartile range and the

75th percentile

interquartile range and the

75th percentile interquartile range. The figure shows only the results for households which state that their

current income equals roughly to their ‘normal’ income (variable HG0700 in the survey). The sample is restricted

to households with non-negative holdings of net wealth/liquid assets and with the reference person aged 25–60

years.

interquartile range. The figure shows only the results for households which state that their

current income equals roughly to their ‘normal’ income (variable HG0700 in the survey). The sample is restricted

to households with non-negative holdings of net wealth/liquid assets and with the reference person aged 25–60

years.

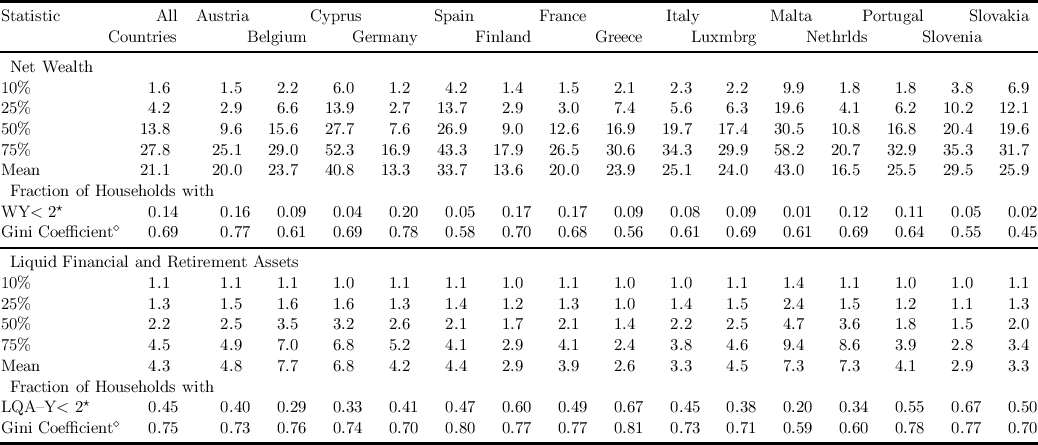

Source: The Eurosystem Household Finance and Consumption Survey.

Notes: Ratios to quarterly household income. The table displays only the statistics for households which state that their current

income equals roughly to their ‘normal’ income (variable HG0700 in the survey). The sample is restricted to households with

non-negative holdings of net wealth/liquid assets and with the reference person aged 25–60 years.  : Fraction of households with

wealth–quarterly income ratio below 2.

: Fraction of households with

wealth–quarterly income ratio below 2.  : Calculated for level of net wealth/liquid assets (not wealth–income

ratio).

: Calculated for level of net wealth/liquid assets (not wealth–income

ratio).

Second, across all countries, the distribution of liquid assets lies substantially closer to zero than the distribution of net wealth, which points toward the hypothesis that a model calibrated to the distribution of liquid assets will imply higher MPCs than a model calibrated to the distribution of net wealth.

Third, the dispersion of the distribution of liquid assets, as reflected, e.g., in the rectangles in Figure 2 showing the interquartile range, is considerably more compressed.

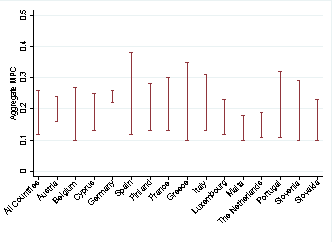

We will now use our model economies to back out quantitatively how the distribution of wealth affects the distribution of the MPC and the reaction of aggregate spending to shocks, such as a ‘fiscal stimulus.’

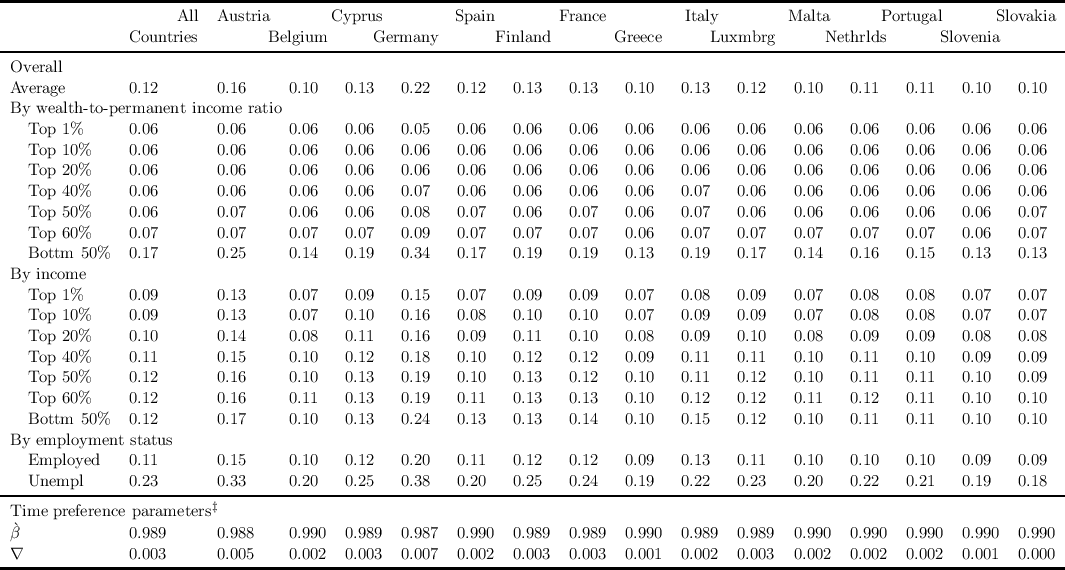

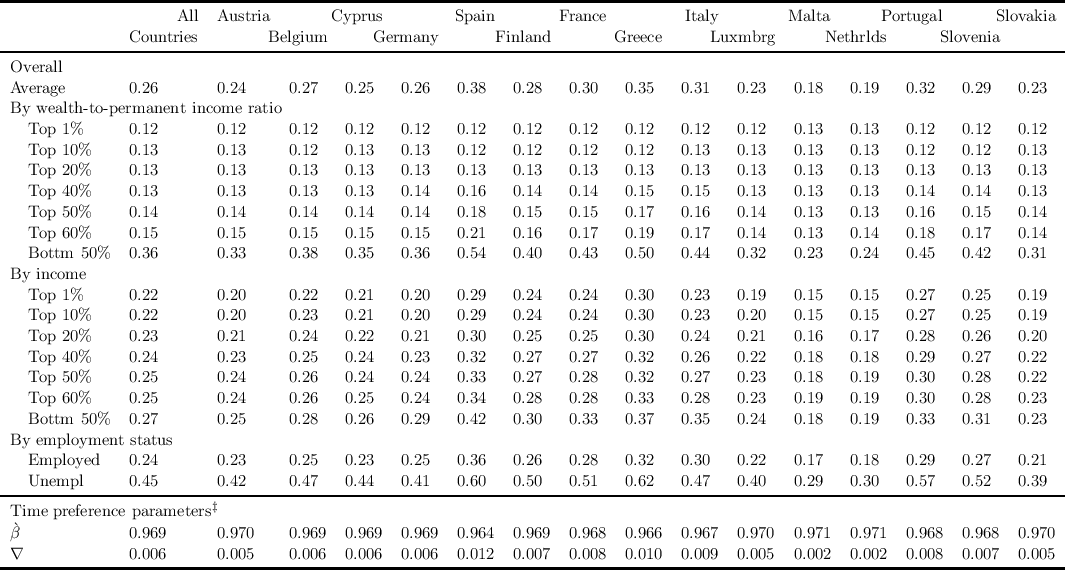

To apply the model of section 2, we alternatively target two wealth variables: net wealth, and liquid financial and retirement assets. These two wealth targets illustrate a range of resources that households can use to smooth adverse shocks.

As argued by Otsuka (2003), Kaplan and Violante (2011) and others, a key factor determining the response of consumer spending is liquidity of assets held by households, i.e., the cost households have to incur if they use their assets to smooth consumption. The model estimated for the distribution of net wealth implicitly assumes that all assets (including housing) are completely liquid, while the model estimated for liquid assets assumes that housing assets are completely illiquid and are not used to smooth consumption. A realistic case in which different assets can be rebalanced at different costs (also depending on, e.g., availability and cost of mortgage equity withdrawal across countries) thus likely lies between these two polar cases reported in Tables 3 and 4.

Notes: The figure shows the range of aggregate MPCs spanned by the estimates based on the distribution of net wealth (lower

bound, Table 3) and of liquid assets (upper bound, Table 4).

Notes: Average (aggregate) propensities in annual terms. Annual MPC is calculated by  quarterly MPC

quarterly MPC .

.  : Discount

factors are uniformly distributed over the interval

: Discount

factors are uniformly distributed over the interval ![[β`- ∇,β`+∇ ]](cstMPCxc54x.png) .

.

Notes: Average (aggregate) propensities in annual terms. Annual MPC is calculated by  quarterly MPC

quarterly MPC .

.  : Discount

factors are uniformly distributed over the interval

: Discount

factors are uniformly distributed over the interval ![[β`- ∇,β`+∇ ]](cstMPCxc59x.png) .

.

To summarize the tables, the model of section 2 implies the following facts:

These estimates are in the lower range of values from numerous empirical studies, which typically find an MPC between 0.2 and 0.6 (investigating mostly various fiscal stimulus episodes in the US).16 Our model thus implies sharply different conclusions than many other models (including Krusell and Smith (1998)) in which the economy behaves in a certainty-equivalent manner and has aggregate MPCs out of transitory income shocks of 0.02–0.05.

This finding is again broadly in line with a number of empirical studies, such as Blundell, Pistaferri, and Preston (2008), Broda and Parker (2012), Kreiner, Lassen, and Leth-Petersen (2012) and Jappelli and Pistaferri (2013).

lie around 0.99 for net

wealth and 0.97 for liquid assets. The extent of heterogeneity in

lie around 0.99 for net

wealth and 0.97 for liquid assets. The extent of heterogeneity in

is very modest:

is very modest:  and

and  for net wealth and

liquid assets, respectively. These values are roughly half the size of

those reported in Carroll, Slacalek, and Tokuoka (2013b) for the

US (

for net wealth and

liquid assets, respectively. These values are roughly half the size of

those reported in Carroll, Slacalek, and Tokuoka (2013b) for the

US ( –

– ), reflecting the lower wealth inequality in

European countries.

), reflecting the lower wealth inequality in

European countries.

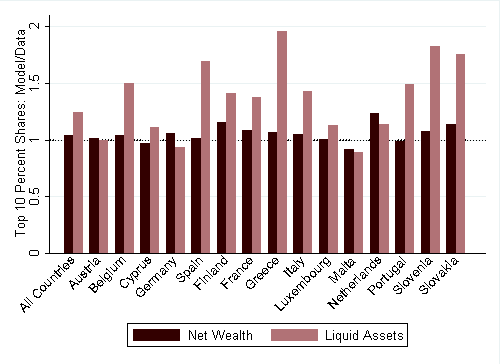

Source: The Eurosystem Household Finance and Consumption Survey and authors’ calculations.

Notes: The figure shows the ratio of the shares implied by the models to those in the data; the values close to one indicate

a good fit.

Source: The Eurosystem Household Finance and Consumption Survey and authors’ calculations.

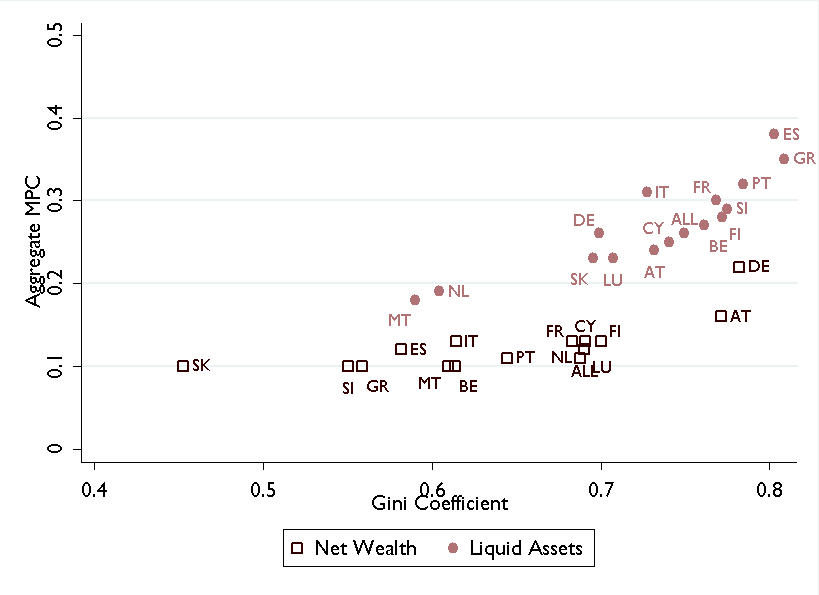

An important advantage of datasets with a large country dimension, such as the Household Finance and Consumption Survey, is that they make it possible to compare economic behavior of households across countries. This section investigates how differences in wealth distributions across countries affect the response of economies to shocks.19

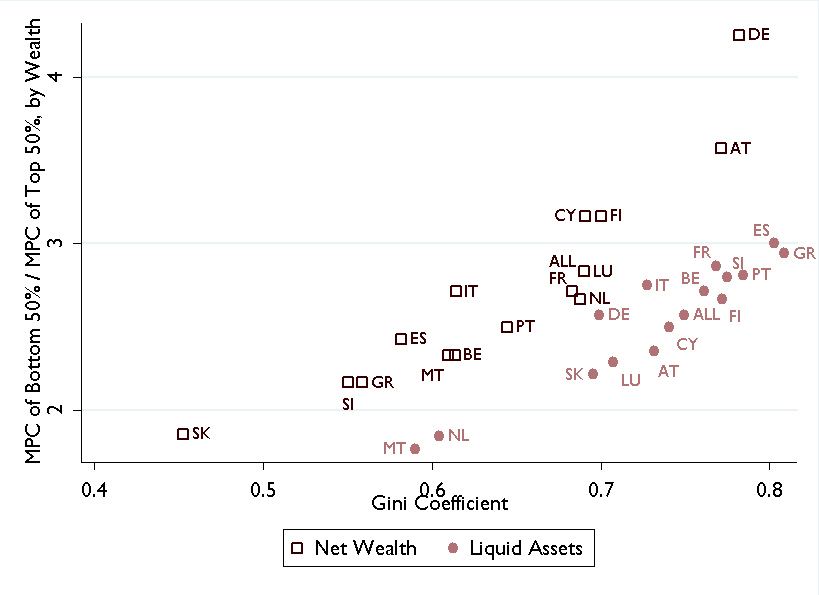

Figure 5 summarizes the relationship between wealth inequality (as measured with the Gini coefficient) and aggregate MPCs (reported in row 1 of Tables 3 and 4). For both measures of wealth, countries with more unequal wealth distributions tend to have a higher proportion of households with little wealth and tend to respond more strongly to shocks.20 The relationship is tighter for liquid assets as these holdings are lower than holdings of net wealth and the consumption function is more concave (and steeper) close to the origin.

Source: The Eurosystem Household Finance and Consumption Survey and authors’ calculations.

Notes: The figure shows the Gini coefficient for wealth against the ratio of the MPC for bottom and top 50 percent of households

by wealth-to-permanent income ratio.

Figure 6 displays the relationship between wealth inequality and heterogeneity across MPCs (as captured in the ratio of average MPCs of the top and bottom half of households by wealth). For both measures of wealth, the figure documents that wealth inequality affects not only the level of aggregate MPC but also the dispersion of MPCs across individual households in the economy. Given the shape of the consumption function, more pronounced wealth inequality increases the proportion of households with little wealth and the MPC among the lower half of the population, while it does not affect the MPC of the upper half, as the consumption function is essentially linear in that region. The relationship is again tighter for liquid assets.

Notes: Average (aggregate) propensities in annual terms. Annual MPC is calculated by  quarterly MPC

quarterly MPC .

.  : Discount

factors are uniformly distributed over the interval

: Discount

factors are uniformly distributed over the interval ![` `

[β - ∇,β +∇ ]](cstMPCxc72x.png) . The targeted wealth distribution is the distribution of net

wealth for the full sample covering all fifteen countries.

. The targeted wealth distribution is the distribution of net

wealth for the full sample covering all fifteen countries.

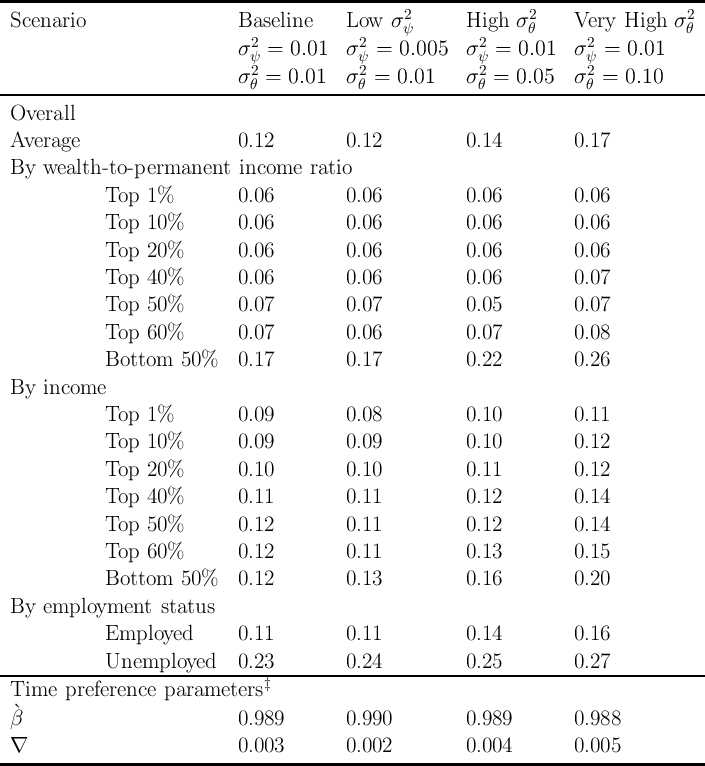

Table 1 above summarized empirical estimates of the FBS income process (1)–(2). Although in principle variance of income shocks should be related to institutional features at the country level, such as progressivity of the tax system and generosity of social benefits, empirical estimates do not seem to reflect this clearly enough.

For that reason, Table 5 presents a comparative statics exercise about the role of the size of income shocks, comparing the baseline calibration of Table 3 (for ‘all countries’) to three alternatives which differ in the variance of permanent and transitory shocks.21

While the size of permanent income shocks affects the shape of the

consumption function only negligibly, empirically plausible variation in the

variance of transitory shocks generates quite substantial changes in the MPC for

the whole economy and, in particular, for households with little wealth. Larger

transitory shocks make the consumption function steeper close to the origin.

Specifically, an increase in  from 0.01 to 0.1 raises the average MPC from

0.13 to 0.17 for the whole population and from 0.19 to 0.26 for the lower 50

percent of households by wealth.

from 0.01 to 0.1 raises the average MPC from

0.13 to 0.17 for the whole population and from 0.19 to 0.26 for the lower 50

percent of households by wealth.

Our results document the importance of matching stylized facts at the household level for thinking about the reaction of economies to shocks. The precautionary saving motive generates a concave consumption function, which means that the reaction of spending of individual households depends on the level of wealth they hold. Due to this substantial non-linearity, to draw correct quantitative conclusions about the aggregate behavior of the economy, it is important that the model fits the empirical wealth distribution. Using data from fifteen European countries, we find that wealth inequality and differences in the dynamics of household income affect the response of economies to a ‘fiscal stimulus’ in an economically relevant way.

ALBARRAN, PEDRO, RAQUEL CARRASCO, AND MAITE MARTINEZ-GRANADO (2009): “Inequality for Wage Earners and Self-Employed: Evidence from Panel Data,” Oxford Bulletin of Economics and Statistics, 71(4), 491–518.

BLANCHARD, OLIVIER J. (1985): “Debt, Deficits, and Finite Horizons,” Journal of Political Economy, 93(2), 223–247.

LE BLANC, JULIA, AND DIMITRIS GEORGARAKOS (2013): “How Risky Is Their Income? Labor Income Processes in Europe,” mimeo, Goethe University Frankfurt.

BLUNDELL, RICHARD, MICHAEL GRABER, AND MAGNE MOGSTAD (2013): “Labor Income Dynamics and the Insurance from Taxes, Transfers, and the Family,” mimeo, University College London.

BLUNDELL, RICHARD, LUIGI PISTAFERRI, AND IAN PRESTON (2008): “Consumption Inequality and Partial Insurance,” American Economic Review, 98(5), 1887–1921.

BRODA, CHRISTIAN, AND JONATHAN A. PARKER (2012): “The Economic Stimulus Payments of 2008 and the Aggregate Demand for Consumption,” mimeo, Northwestern University.

CARROLL, CHRISTOPHER D., JIRI SLACALEK, AND KIICHI TOKUOKA (2013a): “Buffer-Stock Saving in a Krusell–Smith World,” mimeo, Johns Hopkins University.

__________ (2013b): “The Distribution of Wealth and the Marginal Propensity to Consume,” mimeo, Johns Hopkins University, At http://www.econ2.jhu.edu/people/ccarroll/papers/cstMPC/.

CASTANEDA, ANA, JAVIER DIAZ-GIMENEZ, AND JOSE-VICTOR RIOS-RULL (2003): “Accounting for the U.S. Earnings and Wealth Inequality,” Journal of Political Economy, 111(4), 818–857.

CHIURI, MARIA CONCETTA, AND TULLIO JAPPELLI (2003): “Financial Market Imperfections and Home Ownership: A Comparative Study,” European Economic Review, 47(5), 857–875.

EUROSYSTEM HOUSEHOLD FINANCE AND CONSUMPTION NETWORK (2013a): “The Eurosystem Household Finance and Consumption Survey – First Results,” Statistics Paper Series 2, European Central Bank, http://www.ecb.europa.eu/pub/pdf/other/ecbsp2en.pdf.

__________ (2013b): “The Eurosystem Household Finance and Consumption Survey – Methodological Report,” Statistics Paper Series 1, European Central Bank, http://www.ecb.europa.eu/pub/pdf/other/ecbsp1en.pdf.

FRIEDMAN, MILTON A. (1957): A Theory of the Consumption Function. Princeton University Press.

FUCHS-SCHUENDELN, NICOLA, DIRK KRUEGER, AND MATHIAS SOMMER (2010): “Inequality Trends for Germany in the Last Two Decades: A Tale of Two Countries,” Review of Economic Dynamics, 13(1), 103–132.

JAPPELLI, TULLIO, AND LUIGI PISTAFERRI (2010): “Does Consumption Inequality Track Income Inequality in Italy?,” Review of Economic Dynamics, 13(1), 133–153.

__________ (2013): “Fiscal Policy and MPC Heterogeneity,” discussion paper 9333, CEPR.

JOHNSON, DAVID S., JONATHAN A. PARKER, AND NICHOLAS S. SOULELES (2009): “The Response of Consumer Spending to Rebates During an Expansion: Evidence from the 2003 Child Tax Credit,” working paper, The Wharton School.

JOURNAL OF ECONOMIC DYNAMICS AND CONTROL (2010): “Computational Suite of Models with Heterogeneous Agents: Incomplete Markets and Aggregate Uncertainty,” edited by Wouter J. Den Haan, Kenneth L. Judd, Michel Juillard, 34(1), 1–100.

KAPLAN, GREG, AND GIOVANNI L. VIOLANTE (2011): “A Model of the Consumption Response to Fiscal Stimulus Payments,” NBER Working Paper Number W17338.

KREINER, CLAUS THUSTRUP, DAVID DREYER LASSEN, AND SØREN LETH-PETERSEN (2012): “Heterogeneous Responses and Aggregate Impact of the 2001 Income Tax Rebates,” discussion paper 9161, CEPR.

KRUSELL, PER, AND ANTHONY A. SMITH (1998): “Income and Wealth Heterogeneity in the Macroeconomy,” Journal of Political Economy, 106(5), 867–896.

MEGHIR, COSTAS, AND LUIGI PISTAFERRI (2011): “Earnings, Consumption and Life Cycle Choices,” in Handbook of Labor Economics, ed. by O. Ashenfelter, and D. Card, vol. 4, chap. 9, pp. 773–854. Elsevier.

OTSUKA, MISUZU (2003): “Household Portfolio Choice with Illiquid Assets,” manuscript, Johns Hopkins University.

PIJOAN-MAS, JOSEP, AND VIRGINIA SANCHEZ-MARCOS (2010): “Spain Is Different: Falling Trends of Inequality,” Review of Economic Dynamics, 13(1), 154–178.

REVIEW OF ECONOMIC DYNAMICS (2010): “Special Issue: Cross-Sectional Facts for Macroeconomists,” 13(1), 1–264, edited by by Dirk Krueger, Fabrizio Perri, Luigi Pistaferri and Giovanni L. Violante.

ROSTAM-AFSCHAR, DAVUD, AND JIAXIONG YAO (2013): “Taxation and Precautionary Savings over the Life Cycle,” mimeo, Johns Hopkins University.

SHAPIRO, MATTHEW W., AND JOEL B. SLEMROD (2009): “Did the 2008 Tax Rebates Stimulate Spending?,” American Economic Review, 99(2), 374–379, http://www-personal.umich.edu/~shapiro/papers/Rebate2008-2008-12-27-assa-draft.pdf.

SOULELES, NICHOLAS S. (2002): “Consumer Response to the Reagan Tax Cuts,” Journal of Public Economics, 85, 99–120.

YAO, YAO (2011): “Labor Income Risks in Germany,” mimeo, University of Mannheim.

Table 6 displays statistics about the distribution of net wealth, and liquid financial and retirement assets across countries. The last row shows the number of observations in the sample (which is restricted to households with the reference person aged 25–60 years).

Source: The Eurosystem Household Finance and Consumption Survey.

Notes: The sample is restricted to households with the reference person aged 25–60 years.