Abstract This paper builds foundations for rigorous and intuitive understanding of ‘buffer stock’ savingmodels (close cousins of Bewley (1977) models), pairing each theoretical result with quantitativeillustrations. After describing conditions under which a consumption function exists, the paper showsthat a consumer subject to idiosyncratic shocks will engage in ‘target’ saving whenever anormalized ‘growth impatience’ condition is imposed. A related condition guarantees theexistence of an ‘expected balanced growth’ point. Together, the (provided) numerical toolsand (proven) analytical results constitute a comprehensive toolkit for understanding.

Keywords

Precautionary saving, buffer stock saving, marginal propensity

to consume, permanent income hypothesis, income fluctuation

problem

A dashboardallows users to see the consequences of alternative parametric choices in a live interactiveframework; a corresponding Jupyter Notebookuses the Econ-ARK/HARKtoolkit to produce all of the paper’sfigures (warning: the notebook may take several minutes to launch).

In the presence of empirically realistic transitory and permanent income shocks a laFriedman (1957),1

only one further ingredient is required to construct a microeconomically testable

model of optimal consumption: A description of preferences. Zeldes (1989) was

the first to construct a quantitatively realistic version of such a model, spawning a

subsequent literature showing that such models’ predictions can match evidence

from household data reasonably well, whether or not liquidity constraints are

imposed.2

A related theoretical literature has derived limiting properties of infinite-horizon

solutions of such models, but only in cases more complex than the case with just

shocks and preferences (Bewley (1977) and successors). The extra complexity has

been required, in part, because standard contraction mapping theorems (beginning

with Bellman (1957) and including those building on Stokey et. al. (1989))

cannot be applied when utility or marginal utility are unbounded. Many proof

methods also rule out permanent shocks a la Friedman (1957), Muth (1960), and

Zeldes (1989).3

This paper’s first technical contribution is to articulate conditions under which the simple

problem (without complications like a consumption floor or liquidity constraints) defines a

contraction mapping whose limiting value and consumption functions are nondegenerate as

the horizon approaches infinity. The key condition is a generalization of a condition in Ma,

Stachurski, and Toda (2020), which we call the‘Finite Value of Autarky Condition’ (the other

required condition, the ‘Weak Return Impatience Condition’ is unlikely to bind). Conveniently,

the resulting model has analytical properties, like continuous differentiability of the

consumption function, that make it easier to analyze than the standard (but more

complicated) models.

The paper’s other main theoretical contribution is to identify conditions under which

‘stable’ values of the wealth-to-permanent-income ratio exist, either for individual consumers

(an individual consumer’s wealth can be predicted to move toward a ‘target’ ratio) or for the

aggregate (the economy as a whole moves toward a ‘balanced growth’ equilibrium in which the

ratio of aggregate wealth to aggregate income is constant). The requirement for stability is

always that the model’s parameters must satisfy some version of a ‘Growth Impatience

Condition’ where the nature of the condition depends on the quantity whose stability is

required. A model that exhibits stability of this kind is what we will call a ‘buffer stock’

model.4

Even without a formal proof of its existence, target saving has been intuitively understood

to underlie central quantitative results from the heterogeneous agent macroeconomics

literature; for example, the logic of target saving is central to the recent claim by Krueger,

Mitman, and Perri (2016) in the Handbook of Macroeconomics that such models explain why,

during the Great Recession, middle-class consumers cut their consumption more than

the poor or the rich. The theory below provides the rigorous theoretical basis for

this claim: Learning that the future has become more uncertain does not change

the urgent imperatives of the poor (their high means they – optimally –

have little room to maneuver). And, increased labor income uncertainty does not

change the behavior of the rich because it poses little risk to their consumption. Only

people in the middle have both the motivation and the wiggle-room to reduce their

spending.

Analytical derivations required for the proofs provide foundations for many other results familiar from the

numerical literature.5

The paper proceeds in three parts.

The first part articulates sufficient conditions for the problem to define a useful

(nondegenerate) limiting consumption function, and explains how the model relates to those

previously considered in the literature, showing that the conditions required for convergence

are interestingly parallel to those required for the liquidity constrained perfect foresight

model; that parallel is explored and explained. Next, the paper derives limiting

properties of the consumption function as resources approach infinity, and as they

approach their lower bound; using these limits, the contraction mapping theorem is

then proven. Last comes a proof that a corresponding model with an ‘artificial’

liquidity constraint (that is, a model that exogenously prohibits consumers from

borrowing even if they could certainly repay) is a particular limiting case of the

model without constraints. The analytical convenience of the unconstrained model is

that it is both mathematically convenient (e.g., the consumption function is twice

continuously differentiable), and arbitraily close (cf. section 2.10) to less tractable

models that have heretofore been tackled with less convenient methods. For future

authors, the approach here models a strategy of proving interesting propositions in

this more congenial environment, and then appealing to a limiting argument to

establish the analogous proposition in an explicitly constrained but more unwieldy

environment.

In proving the remaining theorems, the next section examines key properties of the model.

First, as cash approaches infinity the expected growth rate of consumption and the

marginal propensity to consume (MPC) converge to their values in the perfect foresight

case. Second, as cash approaches zero the expected growth rate of consumption

approaches infinity, and the MPC approaches a simple analytical limit. Next, the central

theorems articulate conditions under which different measures of ‘growth impatience’

imply useful conclusions about points of stability (‘target’ or ‘balanced growth’

points).

The final section elaborates the conditions under which, even with a fixed aggregate interest

rate that differs from the time preference rate, a small open economy populated by

buffer stock consumers has a balanced growth equilibrium in which growth rates of

consumption, income, and wealth match the exogenous growth rate of permanent

income (equivalent, here, to productivity growth). In the terms of Schmitt-Grohé

and Uribe (2003), buffer stock saving is an appealing method of ‘closing’ a small

open economy model, because it requires no ad-hoc assumptions. Not even liquidity

constraints.

2 The Problem

2.1 Setup

The infinite horizon solution is the (limiting) first-period solution to a sequence of

finite-horizon problems as the horizon (the last period of life) becomes arbitrarily

distant.

That is, for the value function, fixing a terminal date , we are interested in the term

in the sequence of value functions . We will say that the problem

has a ‘nondegenerate’ infinite horizon solution if, corresponding to that value function, as

there is a limiting consumption function which is neither

everywhere (for all ) nor everywhere.

Concretely, a consumer born periods before date solves the problem

where the utility function

(1)

exhibits relative risk aversion .6

The consumer’s initial condition is defined by market resources and permanent

noncapital income , which both are positive,

(2)

and the consumer cannot die in debt,

(3)

In the usual treatment, a dynamic budget constraint (DBC) incorporates several elements

that jointly determine next period’s (given this period’s choices); for the detailed analysis

here, it will be useful to disarticulate the steps:

where indicates the consumer’s assets at the end of period , which grow

by a fixed interest factor between periods, so that is the

consumer’s financial (‘bank’) balances before next period’s consumption

choice;7 (‘market resources’) is the sum of financial wealth and noncapital income

(permanent noncapital income multiplied by a mean-one iid transitory

income shock factor ; transitory shocks are assumed to satisfy ).

Permanent noncapital income in is equal to its previous value, multiplied by a growth

factor , modified by a mean-one iid shock , satisfying

for (and is the degenerate case with no

permanent shocks).

Following Zeldes (1989), in future periods there is a small probability

that income will be zero (a ‘zero-income event’),

(4)

where is an iid mean-one random variable () whose distribution satisfies where

.8

Call the cumulative distribution functions and (where is derived trivially from

(4) and ). For quick identification in tables and graphs, we will call this the

Friedman/Muth model because it is a specific implementation of the Friedman (1957) model

as interpreted by Muth (1960), needing only a calibration of the income process and a

specification of preferences (here, geometric discounting and CRRA utility) to be

solvable.

The model looks more special than it is. In particular, the assumption of a positive

probability of zero-income events may seem objectionable (though it has empirical

support).9

However, it is easy to show that a model with a nonzero minimum value of (motivated,

for example, by the existence of unemployment insurance) can be redefined by

capitalizing the present discounted value of minimum income into current market

assets,10

transforming that model back into this one. And no key results would change

if the transitory shocks were persistent but mean-reverting, instead of IID.

Also, the assumption of a positive point mass for the worst realization of the

transitory shock is inessential, but simplifies the proofs and is a powerful aid to

intuition.11

This model differs from Bewley’s (1977) classic formulation in several ways. The Constant

Relative Risk Aversion (CRRA) utility function does not satisfy Bewley’s assumption that

is well defined, or that is well defined and finite; indeed, neither the value

function nor the marginal value function will be bounded. It differs from Schectman and

Escudero (1977) in that they impose liquidity constraints and positive minimum income. It

differs from both of these in that it permits permanent growth in income, and also permanent

shocks to income, which a large empirical literature finds are of dominant importance in micro

data12

(permanent shocks are far more consequential for household welfare than

are transitory fluctuations). It differs from Deaton (1991) because liquidity

constraints are absent; there are separate transitory and permanent shocks (a laMuth (1960)); and the transitory shocks here can occasionally cause income to reach

zero.13

It differs from models found in Stokey et. al. (1989) because neither

liquidity constraints nor bounds on utility or marginal utility are

imposed.1415Li and Stachurski (2014) show how to allow unbounded returns by using policy function

iteration, but also impose constraints.

The paper with perhaps the most in common with this one is Ma, Stachurski, and Toda (2020),

henceforth MST, who establish the existence and uniqueness of a solution to a general income

fluctuation problem in a Markovian setting. The most important differences are that MST

impose liquidity constraints, assume that , and that expected marginal utility of

income is finite (. These assumptions are not consistent with the combination

of CRRA utility and income dynamics used here, whose combined properties are key to the

results.16

2.2 The Problem Can Be Normalized By Permanent Income

We establish a bit more notation by reviewing the familiar result that in such problems

(CRRA utility, permanent shocks) the number of states can be reduced from two ( and

) to one . Value in the last period of life is ; using (in the last line in

(5) below) the fact that for our CRRA utility function, , and generically

defining nonbold variables as the boldface counterpart normalized by (as with

), consider the problem in the second-to-last period,

Now, in a one-time deviation from the notational convention established in the last

sentence, define nonbold ‘normalized value’ not as but as , because this

allows us to exploit features of the related problem,

where is a ‘growth-normalized’ return factor, and the new problem’s first order

condition is17

This logic induces to earlier periods; if we solve the normalized one-state-variable problem

(5), we will have solutions to the original problem for any from:

2.3 Definition of a Nondegenerate Solution

The problem has a nondegenerate solution if as the horizon gets arbitrarily large

the solution in the first period of life gets arbitrarily close to a limiting

:

(6)

that satisfies

(7)

for every

2.4 Perfect Foresight Benchmarks

The familiar analytical solution to the perfect foresight model, obtained by setting

and , allows us to define some remaining notation and

terminology.

2.4.1 Human Wealth

The dynamic budget constraint, strictly positive marginal utility, and the can’t-die-in-debt

condition (3) imply an exactly-holding intertemporal budget constraint (IBC):

(8)

where is nonhuman wealth, and with a constant ‘human wealth’

is

In order for to be finite, we must impose the Finite Human Wealth

Condition (‘FHWC’):

(9)

Intuitively, for human wealth to be finite, the growth rate of (noncapital) income must be

smaller than the interest rate at which that income is being discounted.

2.4.2 When Does the Perfect Foresight Unconstrained Solution Exist?

Without constraints, the consumption Euler equation always holds; with ,

(10)

where the archaic letter ‘thorn’ represents what we will call the ‘Absolute Patience Factor,’ or

APF:

(11)

The sense in which captures patience is that if the ‘absolute impatience condition’ (AIC)

holds,18

(12)

the consumer will choose to spend an amount too large to sustain indefinitely. We call such a

consumer ‘absolutely impatient.’

We next define a ‘Return Patience Factor’ (RPF) that relates absolute patience to the

return factor:

(13)

and since consumption is growing by but discounted by :

which defines a normalized finite-horizon perfect foresight consumption function

(16)

where is the marginal propensity to consume (MPC) – it answers the question ‘if

the consumer had an extra unit of resources, how much more would be spent.’

(’s overbar signfies that will be an upper bound as we modify the problem to

incorporate constraints and uncertainty; analogously, is a lower bound for the

MPC).

Equation (15) makes plain that for the limiting MPC to be strictly positive

as goes to infinity we must impose the Return Impatience Condition

(RIC):

(17)

so that

(18)

The RIC thus imposes a second kind of ‘impatience:’ The consumer cannot be so

pathologically patient as to wish, in the limit as the horizon approaches infinity, to

spend nothing today out of an increase in current wealth (the RIC rules out the

degenerate limiting solution ). A consumer who satisfies the RIC is ‘return

impatient.’

Given that the RIC holds, and (as before) defining limiting objects by the absence of a time

subscript, the limiting upper bound consumption function will be

(19)

and so in order to rule out the degenerate limiting solution we need to be

finite; that is, we must impose the Finite Human Wealth Condition (9).

Because we can write a useful analytical expression for the value the

consumer would achieve by spending permanent income in every period:

which (for ) asymptotes to a finite number as approaches if any of

these equivalent conditions holds:

where we call 19

the ‘Perfect Foresight Value Of Autarky Factor’ (PF-VAF), and the variants of (20) constitute

alternative versions of the Perfect Foresight Finite Value of Autarky Condition, PF-FVAC;

they guarantee that a consumer who always spends all permanent income ‘has finite autarky

value.’20

If the FHWC is satisfied, the PF-FVAC implies that the RIC is satisfied: Divide both sides

of the second inequality in (20) by :

(20)

and FHWC the RHS is because (and the RHS is raised to a positive

power (because )).

Likewise, if the FHWC and the GIC are both satisfied, PF-FVAC follows:

where the last line holds because FHWC and .

The first panel of Table 4 summarizes: The PF-Unconstrained model has a nondegenerate

limiting solution if we impose the RIC and FHWC (these conditions are necessary as well as

sufficient). Imposing the PF-FVAC and the FHWC implies the RIC, so PF-FVAC and FHWC

are jointly sufficient. If we impose the GIC and the FHWC, both the PF-FVAC and the RIC

follow, so GIC+FHWC are also sufficient. But there are circumstances under which the RIC

and FHWC can hold while the PF-FVAC fails (which we write ). For example, if

, the problem is a standard ‘cake-eating’ problem with a nondegenerate solution under

the RIC.

Perhaps more useful than this prose or the table, the relations of the conditions for the

unconstrained perfect foresight case are presented diagrammatically in Figure 1. Each node

represents a quantity considered in the foregoing analysis. The arrow associated with each

inequality reflects the imposition of that condition. For example, one way we wrote the

PF-FVAC in equation (20) is , so imposition of the PF-FVAC is captured

by the diagonal arrow connecting and . Traversing the boundary

of the diagram clockwise starting at involves imposing first the GIC then the

FHWC, and the consequent arrival at the bottom right node tells us that these two

conditions jointly imply that the PF-FVAC holds. Reversal of a condition will reverse

the arrow’s direction; so, for example, the bottommost arrow going from to

imposes ; but we can cancel the cancellation and reverse the

arrow. This would allow us to traverse the diagram in a clockwise direction from

to , revealing that imposition of GIC and FHWC (and, redundantly, FHWC

again) let us conclude that the RIC holds because the starting point is and the

endpoint is . (Consult Appendix K for a detailed exposition of diagrams of this

type).

Figure 1:Relation of GIC, FHWC, RIC, and PF-FVAC

An arrowhead points to the larger of the two quantities being compared. For example, the diagonal arrowindicates that, which is one way of writing thePF-FVAC, equation(20)

2.4.3 PF Constrained Solution Exists Under RIC or Under {,GIC}

We next examine the perfect foresight constrained solution because it is a useful

benchmark (and limit) for the unconstrained problem with uncertainty (examined

next).

If a liquidity constraint requiring is ever to be relevant, it must be relevant at the

lowest possible level of market resources, , defined by the lower bound for entering the

period, . The constraint is ‘relevant’ if it prevents the choice that would otherwise be

optimal; at the constraint is relevant if the marginal utility from spending all of

today’s resources , exceeds the marginal utility from doing the same thing

next period, ; that is, if such choices would violate the Euler equation

(5):

(21)

By analogy to the RPF, we therefore define a ‘growth patience factor’ (GPF)

as

(22)

and define a ‘growth impatience condition’ (GIC)

(23)

which is equivalent to (21) (exponentiate both sides by ).

We now examine implications of possible configurations of the conditions.

andRIC. If the GIC fails but the RIC (17) holds, appendix A shows that, for some

, an unconstrained consumer behaving according to (19) would choose for all

. In this case the solution to the constrained consumer’s problem is simple: For any

the constraint does not bind (and will never bind in the future); for such the

constrained consumption function is identical to the unconstrained one. If the consumer were

somehow21

to arrive at an the constraint would bind and the consumer would

consume . Using the accent to designate the version of a function in the

presence of constraints (and recalling that is the unconstrained perfect foresight

solution):

(24)

GICandRIC. More useful is the case where the return impatience and GIC conditions both

hold. In this case appendix A shows that the limiting constrained consumption function is

piecewise linear, with up to a first ‘kink point’ at , and with discrete

declines in the MPC at a set of kink points . As the constrained

consumption function becomes arbitrarily close to the unconstrained , and the

marginal propensity to consume function limits to . Similarly, the value

function is nondegenerate and limits into the value function of the unconstrained

consumer.

This logic holds even when the finite human wealth condition fails (), because the

constraint prevents the consumer from borrowing against infinite human wealth to finance

infinite current consumption. Under these circumstances, the consumer who starts with any

amount of resources will, over time, run those resources down so that by some finite

number of periods in the future the consumer will reach , and thereafter

will set for eternity (which the PF-FVAC says yields finite value). Using

the same steps as for equation (20), value of the interim program is also finite:

So, if , value for any finite will be the sum of two finite numbers: The

component due to the unconstrained consumption choice made over the finite horizon leading

up to , and the finite component due to the value of consuming all

thereafter.

GICand. The most peculiar possibility occurs when the RIC fails. Under these

circumstances the FHWC must also fail (Appendix A), and the constrained consumption

function is nondegenerate. (See appendix Figure 8 for a numerical example). While it is true

that , nevertheless the limiting constrained consumption function is

strictly positive and strictly increasing in . This result interestingly reconciles the

conflicting intuitions from the unconstrained case, where would suggest a

degenerate limit of while would suggest a degenerate limit of

.

We now examine the case with uncertainty but without constraints, which will turn out to

be a close parallel to the model with constraints but without uncertainty.

2.5 Uncertainty-Modified Conditions

2.5.1 Impatience

When uncertainty is introduced, the expectation of beginning-of-period bank balances

can be rewritten as:

(25)

where Jensen’s inequality guarantees that the expectation of the inverse of the permanent

shock is strictly greater than one. It will be convenient to define

(26)

which satisfies (thanks to Mr. Jensen), so we can define

(27)

which is useful because it allows us to write uncertainty-adjusted versions of equations and

conditions in a manner exactly parallel to those for the perfect foresight case; for example, we

define a normalized Growth Patience Pactor (GPF-Nrm):

(28)

and a normalized version of the Growth Impatience Condition, GIC-Nrm:

(29)

which is stronger than the perfect foresight version (23) because (cf (27)).

2.5.2 Autarky Value

Analogously to (20), value for a consumer who spent exactly their permanent income every

period would reflect the product of the expectation of the (independent) future shocks to

permanent income:

which invites the definition of a utility-compensated equivalent of the permanent

shock,

(30)

which will satisfy for and nondegenerate . Defining

(31)

we can see that will be finite as approaches if

which we call the ‘finite value of autarky condition’ (FVAC) because it

guarantees that value is finite for a consumer who always consumes their (now

stochastic) permanent income (and we will call the ‘Value of Autarky Factor,’

VAF).22

For nondegenerate , this condition is stronger (harder to satisfy in the

sense of requiring lower ) than the perfect foresight version (20) because

.23

2.6 The Baseline Numerical Solution

Figure 2, familiar from the literature, depicts the successive consumption rules that apply in

the last period of life , the second-to-last period, and earlier periods under baseline

parameter values listed in Table 2. (The 45 degree line is because in the last

period of life it is optimal to spend all remaining resources.)

Table 1:Microeconomic Model Calibration

Table 2:Model Characteristics Calculated from Parameters

Figure 2:Convergence of the Consumption Rules

In the figure, the consumption rules appear to converge to a nondegenerate . Our next

purpose is to show that this appearance is not deceptive.

2.7 Concave Consumption Function Characteristics

A precondition for the main proof is that the maximization problem (5)

defines a sequence of continuously differentiable strictly increasing strictly

concave24

functions . The straightforward but tedious proof is relegated to appendix B.

For present purposes, the most important point is that the income process induces what

Aiyagari (1994) dubbed a ‘natural borrowing constraint’: for all periods

because a consumer who spent all available resources would arrive in period with

balances of zero, and then might earn zero income over the remaining horizon, requiring

the consumer to spend zero, incurring negative infinite utility. To avoid this disaster, the

consumer never spends everything. Zeldes (1989) seems to have been the first to argue, based

on his numerical results, that the natural borrowing constraint was a quantitatively

plausible alternative to ‘artificial’ or ‘ad hoc’ borrowing constraints in a life cycle

model.25

Strict concavity and continuous differentiability of the consumption function are key

elements in many of the arguments below, but are not characteristics of models with

‘artificial’ borrowing constraints. As the arguments below will illustrate, the analytical

convenience of these features is considerable – a point that may appeal to theorists when

they realize (cf. section H below) that the solution to this congenial problem is

arbitraily close to the solutin to the constrained but less wieldy problem with explicit

constraints.

2.8 Bounds for the Consumption Functions

The consumption functions depicted in Figure 2 appear to have limiting

slopes as and as . This section confirms that impression

and derives those slopes, which will be needed in the contraction mapping

proof.26

Assume that a continuously differentiable concave consumption function exists in period

, with an origin at , a minimal MPC , and maximal MPC

. (If these will be ; for earlier periods they will exist by

recursion from the following arguments.)

The MPC bound as wealth approaches infinity is easy to understand: In this case, under our

imposed assumption that human wealth is finite, the proportion of consumption

that will be financed out of human wealth approaches zero. In consequence, the

proportional difference between the solution to the model with uncertainty and the perfect

foresight model shrinks to zero. In the course of proving this, appendix G provides

a useful recursive expression (used below) for the (inverse of the) limiting MPC:

(32)

2.8.1 Weak RIC Conditions

Appendix equation (72) presents a parallel expression for the limiting maximal MPC as

:

(33)

where is a decreasing convergent sequence if the ‘weak return patience factor’

satisfies:

(34)

a condition we dub the ‘Weak Return Impatience Condition’ (WRIC) because with it

will hold more easily (for a larger set of parameter values) than the RIC ().

The essence of the argument is that as wealth approaches zero, the overriding

consideration that limits consumption is the (recursive) fear of the zero-income

events. (That is why the probability of the zero income event appears in the

expression.)

We are now in position to observe that the optimal consumption function must

satisfy

(35)

because consumption starts at zero and is continuously differentiable (as argued above), is strictly

concave,27

and always exhibits a slope between and (the formal proof is in appendix

D).

2.9 Conditions Under Which the Problem Defines a Contraction Mapping

As mentioned above, standard theorems in the contraction mapping literature following

Stokey et. al. (1989) require utility or marginal utility to be bounded over the space of

possible values of , which does not hold here because the possibility (however unlikely) of

an unbroken string of zero-income events through the end of the horizon means

that utility (and marginal utility) are unbounded as . Although a recent

literature examines the existence and uniqueness of solutions to Bellman equations

in the presence of ‘unbounded returns’ (see, e.g., Matkowski and Nowak (2011)),

the techniques in that literature cannot be used to solve the problem here because

the required conditions are violated by a problem that incorporates permanent

shocks.28

Fortunately, Boyd (1990) provided a weighted contraction mapping theorem that Alvarez

and Stokey (1998) showed could be used to address the homogeneous case (of which CRRA is

an example) in a deterministic framework; later, Durán (2003) showed how to extend the

Boyd (1990) approach to the stochastic case.

Definition 1.Consider any functionwhereis the space of continuousfunctions fromto. Supposewithand. Thenis-bounded if the-norm of,

(36)

is finite.

For defined as the set of functions in that are -bounded; ,

, , and as examples of -bounded functions; and using to

indicate the function that returns zero for any argument, Boyd (1990) proves the

following.

We can show that our operator satisfies the conditions that Boyd requires of his

operator , if we impose two restrictions on parameter values. The first is the

WRIC necessary for convergence of the maximal MPC, equation (34) above. More serious is

the Finite Value of Autarky condition, equation (32). (We discuss the interpretation of these

restrictions in detail in section 2.11 below.) Imposing these restrictions, we are now in position

to state the central theorem of the paper.

Theorem 1.is a contraction mapping if the restrictions on parameter values (34)

and (32) are true (that is, if the weak return impatience condition and the finite valueof autarky condition hold).

Intuitively, Boyd’s theorem shows that if you can find a that is everywhere finite but

goes to infinity ‘as fast or faster’ than the function you are normalizing with , the

normalized problem defines a contraction mapping. The intuition for the FVAC condition is

just that, with an infinite horizon, with any initial amount of bank balances , in the

limit your value can always be made greater than you would get by consuming

exactly the sustainable amount (say, by consuming for some small

).

The details of the proof are cumbersome, and are therefore relegated to appendix D. Given

that the value function converges, appendix E.2 shows that the consumption functions

converge.32

2.10 The Liquidity Constrained Solution as a Limit

This section explains why a related problem commonly considered in the literature (e.g., by

Deaton (1991)), with a liquidity constraint and a positive minimum value of income, is the

limit of the problem considered here as the probability of the zero-income event

approaches zero.

The ‘related’ problem makes two changes to the problem defined above:

An ‘artificial’ liquidity constraint is imposed:

The probability of zero-income events is zero:

The essence of the argument is simple. Imposing the artificial constraint without changing

would not change behavior at all: The possibility of earning zero income over the

remaining horizon already prevents the consumer from ending the period with zero assets. So,

for precautionary reasons, the consumer will save something.

But the extent to which the consumer feels the need to make this precautionary provision

depends on the probability that it will turn out to matter. As , that probability becomes

arbitrarily small, so the amount of precautionary saving induced by the zero-income events

approaches zero as . But “zero” is the amount of precautionary saving that

would be induced by a zero-probability event for the impatient liquidity constrained

consumer.

Another way to understand this is just to think of the liquidity constraint reflecting a

component of the utility function that is zero whenever the consumer ends the period with

(strictly) positive assets, but negative infinity if the consumer ends the period with (weakly)

negative assets.

See appendix H for the formal proof justifying the foregoing intuitive

discussion.33

The conditions required for convergence and nondegeneracy are thus strikingly similar

between the liquidity constrained perfect foresight model and the model with uncertainty but

no explicit constraints: The liquidity constrained perfect foresight model is just the limiting

case of the model with uncertainty as the degree of all three kinds of uncertainty

(zero-income events, other transitory shocks, and permanent shocks) approaches

zero.

2.11 Discussion of Parametric Restrictions

The full relationship among all the conditions is represented in Figure 3. Though the diagram

looks complex, it is merely a modified version of the earlier diagram with further

(mostly intermediate) inequalities inserted. (Arrows with a “because” are a new

element to label relations that always hold under the model’s assumptions.) Again

readers unfamiliar with such diagrams should see Appendix K) for a more detailed

explanation.

Figure 3:Relation of All Inequality Conditions

See Table 2 for Numerical Values of Nodes Under Baseline Parameters

2.11.1 The WRIC

The ‘weakness’ of the additional condition sufficient for contraction beyond the FVAC, the

WRIC, can be seen by asking ‘under what circumstances would the FVAC hold but the

WRIC fail?’ Algebraically, the requirement is

(38)

If we require , the WRIC is redundant because now , so that (with

and ) the RIC (and WRIC) must hold. But neither theory nor evidence

demands that we assume . We can therefore approach the question of the WRIC’s

relevance by asking just how low must be for the condition to be relevant. Suppose for

illustration that , , and . In that case (38)

reduces to

but since by assumption, the binding requirement is that

so that for example if we would need (that is, a perpetual

riskfree rate of return of worse than -90 percent a year) in order for the WRIC to

bind.

Perhaps the best way of thinking about this is to note that the space of parameter

values for which the WRIC is relevant shrinks out of existence as , which

section 2.10 showed was the precise limiting condition under which behavior becomes

arbitrarily close to the liquidity constrained solution (in the absence of other risks). On

the other hand, when , the consumer has no noncapital income (so that

the FHWC holds) and with the WRIC is identical to the RIC; but the

RIC is the only condition required for a solution to exist for a perfect foresight

consumer with no noncapital income. Thus the WRIC forms a sort of ‘bridge’ between

the liquidity constrained and the unconstrained problems as moves from 0 to

1.

2.11.2 When the RIC Fails

In the perfect foresight problem (section 2.4.2), the RIC was necessary for existence of a

nondegenerate solution. It is surprising, therefore, that in the presence of uncertainty,

the much weaker WRIC is sufficient for nondegeneracy (assuming that the FVAC

holds).

We can directly derive the features the problem must exhibit (given the FVAC) under

(that is, :

but since (cf. the argument below (30)), this requires ; so, given the FVAC,

the RIC can fail only if human wealth is unbounded. As an illustration of the usefulness of

our diagrams, note that this algebraically complicated conclusion could be easily reached

diagrammatically in figure 3 by starting at the node and imposing (reversing the

RIC arrow) and then traversing the diagram along any clockwise path to the PF-VAF node at

which point we realize that we cannot impose the FHWC because that would let us conclude

.

As in the perfect foresight constrained problem, unbounded limiting human wealth

() here does not lead to a degenerate limiting consumption function (finite human

wealth is not a condition required for the convergence theorem). But, from equation (32) and

the discussion surrounding it, an implication of is that . Thus,

interestingly, in the special case (unavailable in the perfect foresight

model) the presence of uncertainty both permits unlimited human wealth and at the

same time prevents unlimited human wealth from resulting in infinite consumption

at any finite . Intutively, in the presence of uncertainty, pathological patience

(which in the perfect foresight model results in a limiting consumption function of

for finite ) plus unbounded human wealth (which the perfect foresight

model prohibits (by assumption FHWC) because it leads to a limiting consumption

function for any finite ) combine to yield a unique finite level of

consumption and the MPC for any finite value of . Note the close parallel to the

conclusion in the perfect foresight liquidity constrained model in the {GIC,} case.

There, too, the tension between infinite human wealth and pathological patience

was resolved with a nondegenerate consumption function whose limiting MPC was

zero.34

2.11.3 When the RIC Holds

FHWC. If the RIC and FHWC both hold, a perfect foresight solution exists (see 2.4.2

above). As the limiting consumption function and value function become

arbitrarily close to those in the perfect foresight model, because human wealth pays for a

vanishingly small portion of spending. This will be the main case analyzed in detail

below.

. The more exotic case is where FHWC does not hold; in the perfect foresight model,

{RIC,} is the degenerate case with limiting . Here, since the FVAC

implies that the PF-FVAC holds (traverse Figure 3 clockwise from by imposing FVAC

and continue to the PF-VAF node), reversing the arrow connecting the and PF-VAF nodes

implies that under :

where the transition from the first to the second lines is justified because

So, {RIC, } implies the GIC holds. However, we are not

entitled to conclude that the GIC-Nrm holds: does not imply where .

See further discussion of this illuminating case in section ??.

We have now established the principal points of comparison between the perfect foresight

solutions and the solutions under uncertainty; these are codified in the remaining parts of

Tables 3 and 4.

Table 3:Definitions and Comparisons of Conditions

Table 4:Sufficient Conditions for Nondegenerate Solution

For feasiblesatisfying, a nondegenerate limiting consumption function defines aunique optimal value ofsatisfying; a nondegenerate limiting value function defines acorresponding unique value of.RIC,FHWC are necessary as well as sufficient forthe perfect foresight case.That is, the first kink point iniss.t. forthe constraintwill bind now, while forthe constraint will bind one period in the future. The second kinkpoint corresponds to thewhere the constraint will bind two periods in the future, etc.In theFriedman/Muth model, theRIC+FHWCare sufficient, but not necessary for nondegeneracy

3 Analysis of the Converged Consumption Function

Figures 4 and 5a,b capture the main properties of the converged consumption rule when the RIC, GIC-Nrm,

and FHWC all hold.35

Figure 4 shows the expected growth factors for the levels of consumption and market

resources, and , for a consumer behaving according to the

converged consumption rule, while Figures 5 and 6 illustrate theoretical bounds for the

consumption function and the marginal propensity to consume.

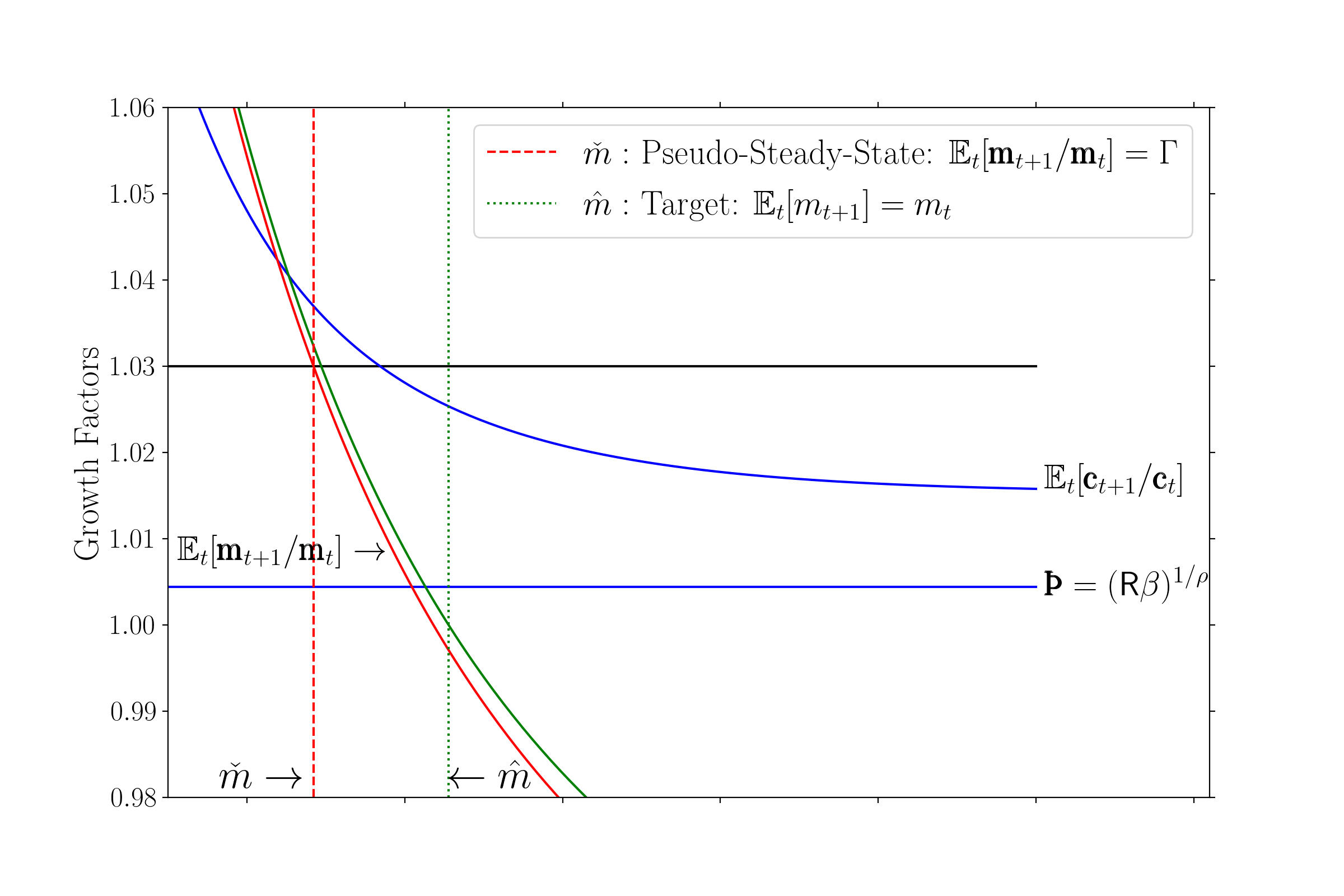

Three features of behavior are captured, or suggested, by the figures. First, as

the expected consumption growth factor goes to , indicated by the lower bound

in Figure 4, and the marginal propensity to consume approaches

(Figure 5), the same as the perfect foresight MPC. Second, as the consumption

growth factor approaches (Figure 4) and the MPC approaches

(Figure 5). Third, there is a value at which the expected growth rate of

matches the expected growth rate of permanent income , and a different

(lower) value where the expected growth rate of consumption at is lower

than . Thus, at the individual level, this model does not have a ‘balanced

growth’ equilibrium in which all model variables are expected to grow at the same

rate.36

Figure 4:‘Stable’ Values and Expected Growth Rates

3.1 Limits as approaches Infinity

Define

which is the solution to an infinite-horizon problem with no noncapital income

(); clearly , since allowing the possibility of future noncapital

income cannot reduce current consumption. Our imposition of the RIC guarantees that

, so this solution satisfies our definition of nondegeneracy, and because this solution

is always available it defines a lower bound on both the consumption and value

functions.

Assuming the FHWC holds, the infinite horizon perfect foresight solution (19) constitutes

an upper bound on consumption in the presence of uncertainty, since the introduction

of uncertainty strictly decreases the level of consumption at any (Carroll and

Kimball (1996)). Thus, we can write

But

so as , and the continuous differentiability and strict concavity of

therefore implies

because any other fixed limit would eventually lead to a level of consumption either exceeding

or lower than .

Figure 5 confirms these limits visually. The top plot shows the converged consumption

function along with its upper and lower bounds, while the lower plot shows the marginal

propensity to consume.

Figure 5:Limiting MPC’s

Figure 6:Upper and Lower Bounds on The Consumption Function

Next we establish the limit of the expected consumption growth factor as :

But

and

while (for convenience defining ),

because 37

and which goes to zero as goes to infinity.

Hence we have

so as cash goes to infinity, consumption growth approaches its value in the perfect

foresight model.

Now using the continuous differentiability of the consumption function along with

L’Hôpital’s rule, we have

Figure 5 confirms that the numerical solution obtains this limit for the MPC as

approaches zero.

For consumption growth, as we have

where the second-to-last line follows because is

positive, and the last line follows because the minimum possible realization of

is so the minimum possible value of expected next-period consumption is

positive.38

3.3 Unique ‘Stable’ Points

Two theorems, whose proofs are sketched here and detailed in an appendix, articulate

alternative (but closely related) stability criteria for the model.

3.3.1 ‘Individual Target Wealth’

One definition of a ‘stable’ point is an such that if , then .

Existence of such a target turns out to require the GIC-Nrm condition.

Theorem 2.For the nondegenerate solution to the problem defined in section2.1whenFVAC,WRIC, andGIC-Nrmall hold, there exists a unique cash-on-hand-to-permanent-income ratiosuch that

(39)

Moreover,is a point of ‘wealth stablity’ in the sense that

Since , the implicit equation for is

(40)

3.3.2 Collective Stability and the Expected-Balanced-Growth State

A traditional question in macroeconomic models is whether there is a ‘balanced growth’

equilibrium in which aggregate variables (income, consumption, market resources) all grow

forever at the same rate. For the model here, we have already seen in Figure 4 that there is no

single for which for an individual consumer.

Nevertheless, analysis below will show that economies populated by collections of such

consumers can exhibit balanced growth in the aggregate.

As an input to that analysis, we show here that if the GIC holds, the problem will have a

point of what we call ‘collective stability,’ by which we mean that there is some such that,

for all , , and conversely for . (‘Collective’ is

meant to capture the fact that calculating the expectation of the levels of future

and before dividing by is akin to examining aggregate values in a

population).

The critical will be the value at which growth matches :

The only difference between (41) and (40) is the substitution of for .

We will refer to as the problem’s Expected-Balanced-Growth State, a term

motivated by the fact that an economy composed of consumers all of whom had

, would exhibit balanced growth if all consumers happened to continually

draw permanent and transitory shocks equal to their expected values of 1.0

forever.39

Theorem 5 formally states the relevant proposition.

Theorem 3.For the nondegenerate solution to the problem defined in section2.1whenFVAC,WRIC, andGICall hold, there exists a unique pseudo-steady-statecash-on-hand-to-income ratiosuch that

(41)

Moreover,is a point of stability in the sense that

The proofs of the two theorems are almost completely parallel; to save space, they are

relegated to Appendix M. In sum, they involve three steps:

Existence and continuity of or

This follows from existence and continuity of the constitutents

Existence of the equilibrium point

This follows from the upper and lower bound limiting MPC’s, existence and

continuity, and the Intermediate Value Theorem

Monotonicity of or

This follows from concavity of the consumption function

3.3.3 Example Where There Is An Expected-Balanced-Growth State But No

Target

Because the equations defining target and pseudo-steady-state , (40) and (41), differ

only by substitution of for , if there are no permanent shocks

(), the conditions are identical. For many parameterizations (e.g., under the

baseline parameter values used for constructing figure 4), and will not differ

much.

An illuminating exception is exhibited in figure 7, which modifies the baseline parameter

values by quadrupling the variance of the permanent shocks, enough to cause failure of the

GIC-Nrm; now there is no target wealth level (consumption remains everywhere below the

level that would keep expected constant).

Figure 7:{FVAC,GIC,}: No Exists But Does

The pseudo-steady-state still exists because it turns off realizations of the permanent shock.

But an aggregate balanced growth equilibrim can exist even when realizations of the

permanent shock are implemented exactly as specified in the model. The key insight can be

understood by considering the evolution of an economy that starts, at date , with the entire

population at , but then evolves according to the model’s correct assumed dynamics

between and . Equation (41) will still hold for this economy, so for this first period,

at least, the economy will exhibit balanced growth: the growth factor for aggregate will

match the growth factor for permanent income . It is true that there will be

people for whom is boosted by a small draw of . But

their contribution to the aggregate variable is given by , so their

reweighted by an amount that exactly undoes the boosting caused by earlier

normalization.

The surprising consequence is that, if the GICholds but the GIC-Nrm fails, it is possible to

construct an aggregate economy composed of consumers all of whom have target wealth of

, but in which the aggregate economy still exhibits balanced growth with a finite ratio

of aggregate wealth to income. (For an example, see the software archive for the

paper).

This is a good introduction to a more explicit discssion of aggregation.

4 The Aggregate and Idiosyncratic Relationship Between Consumption Growth and

Income Growth

A large (infinite) collection of small (infinitesimal) buffer-stock consumers with identical

parameter values can be thought of as a subset of the population within a single

country (say, members of a given education or occupation group), or as the

whole population in a small open economy with an exogenous (constant) interest

rate.40

Until now for convenience we have assumed infinite horizons, with the implicit

understanding that Poisson mortality could be handled by adjusting the effective discount

factor for mortality. On that basis, section 4.1 continues to omit mortality. But a

reason for explicitly introducing mortality will appear at the end of section 4.2, so

implications of alternative assumptions about mortality are briefly examined in

Section 4.3.

Formally, we assume a continuum of ex ante identical households on the unit interval, with

constant total mass normalized to one and indexed by , all behaving according

to the model specified above. Szeidl (2013) proves that whenever the GIC holds

such a population will be characterized by invariant distributions of , , and

;41

designate these , , and .

4.1 Consumption and Income Growth at the Household Level

The operator yields the mean of its argument in the population, as distinct from

the expectations operator used above, which represents beliefs about the

future.

An economist with a microeconomic dataset could calculate the average growth rate of

idiosyncratic consumption in a cross section of an economy that had converged at date , and

would find

where and the last equality follows because the invariance of

(Szeidl (2013)) means that . Thus, the same GIC that

guaranteed the existence of an ‘individual pseudo-steady-state’ value of at the

microeconomic level guarantees both that there will be an invariant distribution of the

population across values of the model variables and that in that invariant distribution the

mean growth rates of all idiosyncratic variables are the same (see Szeidl (2013) for

details).

4.2 Balanced Growth of Aggregate Income, Consumption, and Wealth

Using boldface capital letters for aggregates, the growth factor for aggregate income

is:

because of the independence assumptions we have made about and .

From the perspective of period ,

Unfortunately, the covariance term in the numerator, while generally small, will not in

general be zero. This is because the realization of the permanent shock has a nonlinear

effect on .

Matters are simpler if there are no permanent shocks; see Appendix F for a proof that in that

case the growth rate of assets (and other variables) does eventually converge to the growth

rate of aggregate permanent income.

One way of thinking about the problem here is that it may reflect the fact that,

under our assumptions, permanent income does not have an ergodic distribution;

its distribution of becomes forever wider over time, because our consumers never

die and each immortal person is perpetually subject to symmetric shocks to their

.

This is why we need to introduce mortality.

4.3 Mortality and Redistribution

Most heterogeneous agent models incorporate a constant positive probability of death,

following Blanchard (1985). In a model that mostly follows Blanchard (1985), for

probabilities of death that exceed a threshold that depends on the size of the permanent

shocks, Carroll, Slacalek, Tokuoka, and White (2017) show that the limiting distribution of

permanent income has a finite variance, which is a useful step in the direction of taming the

problems caused by an unbounded distribution of . Numerical results in that paper confirm

the intuition that, under appropriate impatience conditions, balanced growth arises (though a

formal proof remains elusive).

Even with those (numerical) results in hand, the centrality of mortality assumptions

to the existence and nature of steady states requires them to be discussed briefly

here.

4.3.1 Blanchard Lives

Blanchard (1985)’s model assumes the existence of an annuitization scheme in which estates

of dying consumers are redistributed to survivors in proportion to survivors’ wealth, giving the

recipients a higher effective rate of return. This treatment has several analytical advantages,

most notably that the effect of mortality on the time preference factor is the exact inverse of

its effect on the (effective) interest factor: If the probability of remaining alive is , then

assuming that no utility accrues after death makes the effective discount factor

, while the enhancement to the rate of return from the annuity scheme

yields an effective interest rate of (recall that because of Poisson mortality, the

average wealth of the two groups is identical). Combining these, the effective patience

factor in the new economy is unchanged from its value in the infinite horizon

model:

(42)

The only adjustments this requires to the analysis from prior parts of this paper are

therefore to the few elements that involve a role for distinct from its contribution to

(principally, the RIC).

The numerical finding that the covariance term above is approximately zero allows us to

conclude again that the key requirement for aggregate balanced growth is presumably the

GIC.

4.3.2 Modigliani Lives

Blanchard (1985)’s innovation was useful not only for the insight it provided but also because

the principal alternative, the Life Cycle model of Modigliani (1966), was computationally

challenging given the then-available technologies. Aside from its (considerable) conceptual

value, there is no need for Blanchard’s analytical solution today, when serious modeling

incorporates uncertainty, constraints, and other features that rule out analytical solutions

anyway.

The simplest alternative to Blanchard’s mortality is to follow Modigliani in assuming that

any wealth remaining at death occurs accidentally (not implausible, given the robust finding

that for the great majority of households, bequests amount to less than 2 percent of lifetime

earnings, Hendricks (2001, 2016)).

Even if bequests are accidental, a macroeconomic model must make some assumption

about how they are disposed of: As windfalls to heirs, estate tax proceeds, etc. We

again consider the simplest choice, because it again represents something of a polar

alternative to Blanchard: Without a bequest motive, there are no behavioral effects of a

100 percent estate tax; we assume such a tax is imposed and that the revenues are

effectively thrown in the ocean; the estate-related wealth effectively vanishes from the

economy.

The chief appeal of this approach is the simplicity of the change it makes in the condition

required for the economy to exhibit a balanced growth equilibrium. If is the probability of

remaining alive, the condition changes from the plain GIC to a looser mortality-adjusted GIC:

(43)

With no income growth, the condition required to prohibit unbounded growth in aggregate

wealth would be the condition that prevents the per-capita wealth to income ratio of surviving

consumers from growing faster than the rate at which mortality diminishes their collective

population. With income growth, the aggregate wealth-to-income ratio will head to

infinity only if a cohort of consumers is patient enough to make the desired rate of

growth of wealth fast enough to counteract combined erosive forces of mortality and

productivity.

5 Conclusions

Numerical solutions to optimal consumption problems, in both life cycle and infinite horizon

contexts, have become standard tools since the first reasonably realistic models were

constructed in the late 1980s. One contribution of this paper is to show that finite horizon

(‘life cycle’) versions of the simplest such models, with assumptions about income shocks

(transitory and permanent) dating back to Friedman (1957) and standard specifications of

preferences – and without (plausible, but inconvenient) complications like liquidity

constraints – have attractive analytical properties (like continuous differentiability of

the consumption function, and analytical limiting MPC’s as resources approach

their minimum and maximum possible values), and that (more widely used) models

with liquidity constraints can be viewed as a particular limiting case of this simpler

model.

The main focus of the paper, though, is on the limiting solution of the finite horizon model

as the horizon extends to infinity. The paper shows that the simple model has additional

attractive properties: A ‘Finite Value of Autarky’ condition guarantees convergence of the

consumption function, under the mild additional requirement of a ‘Weak Return Impatience

Condition’ that will never bind for plausible parameterizations, but provides intuition for the

bridge between this model and models with explicit liquidity constraints. The paper also

provides a roadmap for the model’s relationships to the perfect foresight model without and

with constraints. The constrained perfect foresight model provides an upper bound to the

consumption function (and value function) for the model with uncertainty, which explains

why the conditions for the model to have a nondegenerate solution closely parallel

those required for the perfect foresight constrained model to have a nondegenerate

solution.

The main use of infinite horizon versions of such models is in heterogeneous agent

macroeconomics. The paper articulates intuitive ‘Growth Impatience Conditions’ under which

populations of such agents, with Blancharidan (tighter) or Modiglianian (looser) mortality will

exhibit balanced growth. Finally, the paper provides the analytical basis for a number of

results about buffer-stock saving models that are so well understood that even without

analytical foundations researchers uncontroversially use them as explanations of real-world

phenomena like the cross-sectional pattern of consumption dynamics in the Great

Recession.

The paper’s results are all easily reproducible interactively on the web or on any standard

computer system. Such reproducibility reflects the paper’s use of the open-source Econ-ARK

toolkit, which is used to generate all of the quantitative results of the paper, and which

integrally incorporates all of the analytical insights of the paper.

Appendices

A Perfect Foresight Liquidity Constrained Solution

Under perfect foresight in the presence of a liquidity constraint requiring , this

appendix taxonomizes the varieties of the limiting consumption function that arise

under various parametric conditions. Results are summarized in table 5.

Table 5:Taxonomy of Perfect Foresight Liquidity Constrained Model Outcomes

Conditions are applied from left to right; for example, the second row indicates conclusions in the case whereandRIC both hold, while the third row indicates that when theGIC and theRIC both fail, theconsumption function is degenerate; the next row indicates that whenever theGICholds, the constraint willbind in finite time.

A.1 If GIC Fails

A consumer is ‘growth patient’ if the perfect foresight growth impatience condition

fails (, ). Under the constraint does not bind at the

lowest feasible value of because implies that spending

everything today (setting ) produces lower marginal utility than is

obtainable by reallocating a marginal unit of resources to the next period at return

:42

Similar logic shows that under these circumstances the constraint will never bind at

for a constrained consumer with a finite horizon of periods, so for such a

consumer’s consumption function will be the same as for the unconstrained case examined in

the main text.

RICfails,FHWCholds. If the RIC fails () while the finite human wealth condition

holds, the limiting value of this consumption function as is the degenerate

function

(44)

(that is, consumption is zero for any level of human or nonhuman wealth).

RIC fails,FHWC fails. implies that human wealth limits to so the

consumption function limits to either or depending on the

relative speeds with which the MPC approaches zero and human wealth approaches

.43

Thus, the requirement that the consumption function be nondegenerate implies that for a

consumer satisfying we must impose the RIC (and the FHWC can be shown to be a

consequence of and RIC). In this case, the consumer’s optimal behavior is easy to

describe. We can calculate the point at which the unconstrained consumer would choose

from equation (19):

(45)

which (under these assumptions) satisfies

.44

For the unconstrained consumer would choose to consume more

than ; for such , the constrained consumer is obliged to choose

.45

For any the constraint will never bind and the consumer will choose to spend the

same amount as the unconstrained consumer, .

(Stachurski and Toda (2019) obtain a similar lower bound on consumption and use it to

study the tail behavior of the wealth distribution.)

A.2 If GIC Holds

Imposition of the GIC reverses the inequality in (44), and thus reverses the conclusion: A

consumer who starts with will desire to consume more than 1. Such a consumer will

be constrained, not only in period , but perpetually thereafter.

Now define as the such that an unconstrained consumer holding would

behave so as to arrive in period with (with trivially equal to 0); for

example, a consumer with was on the ‘cusp’ of being constrained in period :

Had been infinitesimally smaller, the constraint would have been binding

(because the consumer would have desired, but been unable, to enter period with

negative, not zero, ). Given the GIC, the constraint certainly binds in period (and

thereafter) with resources of : The consumer cannot spend more

(because constrained), and will not choose to spend less (because impatient), than

.

We can construct the entire ‘prehistory’ of this consumer leading up to as follows.

Maintaining the assumption that the constraint has never bound in the past, must have

been growing according to , so consumption periods in the past must have

been

(46)

The PDV of consumption from until can thus be computed as

and note that the consumer’s human wealth between and (the relevant time

horizon, because from onward the consumer will be constrained and unable to access

post- income) is

(47)

while the intertemporal budget constraint says

from which we can solve for the such that the consumer with would

unconstrainedly plan (in period ) to arrive in period with :

(48)

Defining , consider the function defined by linearly connecting the

points for integer values of (and setting for ). This

function will return, for any value of , the optimal value of for a liquidity constrained

consumer with an infinite horizon. The function is piecewise linear with ‘kink points’ where

the slope discretely changes; for infinitesimal the MPC of a consumer with assets

is discretely higher than for a consumer with assets because the

latter consumer will spread a marginal dollar over more periods before exhausting

it.

In order for a unique consumption function to be defined by this sequence (48) for the entire

domain of positive real values of , we need to become arbitrarily large with . That is,

we need

(49)

A.2.1 If FHWC Holds

The FHWC requires , in which case the second term in (48) limits to a constant as

, and (49) reduces to a requirement that

Given the GIC , this will hold iff the RIC holds, . But given that the

FHWC holds, the GICis stronger (harder to satisfy) than the RIC; thus,

the FHWC and the GIC together imply the RIC, and so a well-defined solution exists.

Furthermore, in the limit as approaches infinity, the difference between the limiting

constrained consumption function and the unconstrained consumption function becomes

vanishingly small, because the date at which the constraint binds becomes arbitrarily

distant, so the effect of that constraint on current behavior shrinks to nothing. That

is,

(50)

A.2.2 If FHWC Fails

If the FHWC fails, matters are a bit more complex.

IfRIC Holds. When the RIC holds, rearranging (51) gives

and for this to be true we need

which is merely the RIC again. So the problem has a solution if the RIC holds. Indeed, we

can even calculate the limiting MPC from

(51)

which with a bit of algebra46

can be shown to asymptote to the MPC in the perfect foresight

model:47

(53)

IfRIC Fails. Consider now the case, . We can rearrange (51)as

which makes clear that with and the numerators and

denominators of both terms multiplying can be seen transparently to be positive. So,

the terms multiplying in (51) will be positive if

which is merely the GIC which we are maintaining. So the first term’s limit is . The

combined limit will be if the term involving goes to faster than the term

involving goes to ; that is, if

which merely confirms the starting assumption that the RIC fails.

What is happening here is that the term is increasing backward in time at rate

dominated in the limit by while the term is increasing at a rate dominated by

term and

because

Consequently, while , the limit of the ratio in (51) is zero. Thus,

surprisingly, the problem has a well defined solution with infinite human wealth if the

RIC fails. It remains true that implies a limiting MPC of zero,

(56)

but that limit is approached gradually, starting from a positive value, and consequently the

consumption function is not the degenerate . (Figure 8 presents an example for

, , , ; note that the horizontal axis is bank balances

; the part of the consumption function below the depicted points is uninteresting –

– so not worth plotting).

Figure 8:Nondegenerate Consumption Function with and

We can summarize as follows. Given that the GIC holds, the interesting question is

whether the FHWC holds. If so, the RIC automatically holds, and the solution

limits into the solution to the unconstrained problem as . But even if the

FHWC fails, the problem has a well-defined and nondegenerate solution, whether or not the

RIC holds.

Although these results were derived for the perfect foresight case, we know from work

elsewhere in this paper and in other places that the perfect foresight case is an upper bound

for the case with uncertainty. If the upper bound of the MPC in the perfect foresight case is

zero, it is not possible for the upper bound in the model with uncertainty to be

greater than zero, because for any the level of consumption in the model with

uncertainty would eventually exceed the level of consumption in the absence of

uncertainty.

Ma and Toda (2020) characterize the limits of the MPC in a more general framework

that allows for capital and labor income risks in a Markovian setting with liquidity

constraints, and find that in that much more general framework the limiting MPC is also

zero.

B Existence of a Concave Consumption Function

To show that (5) defines a sequence of continuously differentiable strictly increasing concave

functions , we start with a definition. We will say that a function is

‘nice’ if it satisfies

is well-defined iff

is strictly increasing

is strictly concave

is

.

(Notice that an implication of niceness is that )

Assume that some is nice. Our objective is to show that this implies is also nice;

this is sufficient to establish that is nice by induction for all because

and is nice by inspection.

Now define an end-of-period value function as

(57)

Since there is a positive probability that will attain its minimum of zero and since

, it is clear that and . So is

well-defined iff ; it is similarly straightforward to show the other properties required for

to be nice. (See Hiraguchi (2003).)

Next define as

(58)

which is since and are both and note that our problem’s value function

defined in (5) can be written as

(59)

is well-defined if and only if . Furthermore, ,

, , and . It follows that the

defined by

(60)

exists and is unique, and (5) has an internal solution that satisfies

(61)

Since both and are strictly concave, both and are

strictly increasing. Since both and are three times continuously differentiable, using

(61) we can conclude that is continuously differentiable and

(62)

Similarly we can easily show that is twice continuously differentiable (as is )

(See Appendix C.) This implies that is nice, since .

C is Twice Continuously Differentiable

First we show that is Define as . Since

and

Since and are continuous and increasing, and

are satisfied. Then for

sufficiently small . Hence we obtain a well-defined equation:

This implies that the right-derivative, is well-defined and

Similarly we can show that , which means exists. Since is ,

exists and is continuous. is differentiable because is , is

and . is given by

(63)

Since is continuous, is also continuous.

D Proof that Is a Contraction Mapping

We must show that our operator satisfies all of Boyd’s conditions.

Boyd’s operator maps from to A preliminary requirement is

therefore that be continuous for any bounded , . This is not

difficult to show; see Hiraguchi (2003).

the solution to which is patently . Thus, condition (2) will hold if is

-bounded. We use the bounding function

(64)

for some real scalar whose value will be determined in the course of the proof. Under

this definition of , is clearly -bounded.

Finally, we turn to condition (3), The

proof will be more compact if we define and as the consumption and assets

functions49

associated with and and as the functions associated with ; using this

notation, condition (3) can be rewritten

Now note that if we force the consumer to consume the amount that is optimal for the

consumer, value for the consumer must decline (at least weakly). That

is,

Thus, condition (3) will certainly hold under the stronger condition

where the last line follows because by

assumption.50

Using and defining , this condition is

which by imposing PF-FVAC (equation (20), which says ) can be rewritten

as:

(65)

But since is an arbitrary constant that we can pick, the proof thus reduces to showing

that the numerator of (65) is bounded from above:

We can thus conclude that equation (65) will certainly hold for any:

(66)

which is a positive finite number under our assumptions.

The proof that defines a contraction mapping under the conditions (34) and (32) is now

complete.

D.1 and

In defining our operator we made the restriction . However, in

the discussion of the consumption function bounds, we showed only (in (35)) that

. (The difference is in the presence or absence of time subscripts on the

MPC’s.) We have therefore not proven (yet) that the sequence of value functions (5) defines a

contraction mapping.

Fortunately, the proof of that proposition is identical to the proof above, except that we

must replace with and the WRIC must be replaced by a slightly stronger (but still

quite weak) condition. The place where these conditions have force is in the step at (66).

Consideration of the prior two equations reveals that a sufficient stronger condition

is

where we have used (33) for (and in the second step the reversal of the inequality

occurs because we have assumed so that we are exponentiating both sides by the

negative number ). To see that this is a weak condition, note that for small values of

this expression can be further simplified using so that it

becomes

Calling the weak return patience factor and recalling that the WRIC was

, the expression on the LHS above is times the WRPF. Since we usually

assume not far below 1 and parameter values such that , this condition is clearly

not very different from the WRIC.

The upshot is that under these slightly stronger conditions the value functions for the original

problem define a contraction mapping with a unique . But since and

, it must be the case that the toward which these ’s are

converging is the same that was the endpoint of the contraction defined by our

operator . Thus, under our slightly stronger (but still quite weak) conditions, not only do

the value functions defined by (5) converge, they converge to the same unique defined by

.51

E Convergence in Euclidian Space

E.1 Convergence of

Boyd’s theorem shows that defines a contraction mapping in a -bounded space. We now

show that also defines a contraction mapping in Euclidian space.

Calling the unique fixed point of the operator , since ,

(67)

On the other hand, and because and are

in . It follows that

(68)

Then we obtain

(69)

Since , . On the other hand,

means , in other words, . Inductively one gets

. This means that is a decreasing sequence,

bounded below by .

E.2 Convergence of

Given the proof that the value functions converge, we now show the pointwise convergence of

consumption functions .

Consider any convergent subsequence of converging to

. By the definition of , we have

(70)

for any . Now letting go to infinity, it follows that the left hand

side converges to , and the right hand side converges to

. So the limit of the preceding inequality as approaches

infinity implies

(71)

Hence, . By the uniqueness of ,

.

F Equality of Aggregate Consumption Growth and Income Growth with Transitory

Shocks

Section 4.2 asserted that in the absence of permanent shocks it is possible to prove that the

growth factor for aggregate consumption approaches that for aggregate permanent income.

This section establishes that result.

First define as the function that yields optimal end-of-period assets as a function of

.

Suppose the population starts in period with an arbitrary value for .

Then if is the invariant mean level of we can define a ‘mean MPS away from ’

function :

where the combination of the bar and the are meant to signify that this is the average value