September 26, 2022, Christopher D. Carroll OLGModel

September 26, 2022, Christopher D. Carroll OLGModel

September 26, 2022, Christopher D. Carroll OLGModel

This handout and the associated Jupyter notebook, DiamondOLG, present a canonical overlapping generations (OLG) model, like the one originally proposed by Diamond (1965), building on Samuelson (1958).1

The economy has the following features:

is given by

is given by  .

.

.

They earn no income in the second period of life (

.

They earn no income in the second period of life ( ).

).

are the source of the

capital used for aggregate production in period

are the source of the

capital used for aggregate production in period  ,

,  where

where  is the assets per young household after their consumption

in period 1. (For convenience, we assume that there is no depreciation).

is the assets per young household after their consumption

in period 1. (For convenience, we assume that there is no depreciation).

own the entire capital stock and (because they

have no bequest motive) will consume it all, so dissaving by the old

in period

own the entire capital stock and (because they

have no bequest motive) will consume it all, so dissaving by the old

in period  will be

will be  . (The old do receive interest on

their capital, so their consumption will be

. (The old do receive interest on

their capital, so their consumption will be  plus the interest income

plus the interest income

, but the

, but the  component does not affect saving because it is part

of both income and consumption).

component does not affect saving because it is part

of both income and consumption).

(recall that this implies

that

(recall that this implies

that  , which is “Euler’s Theorem”.

, which is “Euler’s Theorem”.

Let’s normalize everything by the period- young population

young population  , writing

normalized variables in lower case. Thus the per-young-capita aggregate

production function becomes

, writing

normalized variables in lower case. Thus the per-young-capita aggregate

production function becomes

| (1) |

The perfect competition assumption implies that wages and net interest rates are equal to the marginal products of labor and capital, respectively:

| (2) |

To make further progress, we need to make specific assumptions about the

utility function and the aggregate production function. Assume that utility is

CRRA,  and assume a Cobb-Douglas aggregate production

function

and assume a Cobb-Douglas aggregate production

function  .

.

In this case we can solve for wages and interest rates:

| (3) |

The individual’s maximization problem yields the Euler equation:

| (4) |

Now let’s assume that utility is logarithmic,  , which implies

that

, which implies

that

![=0

◜-◞◟ -◝

W1,t-+--W2,t+1-∕Rt+1---

c1,t = 1 + β

W1,t---

c1,t = 1 + β

a1,t = W1,t − c1,t

= W1,t (1 − 1∕ (1 + β ))

= W1,t (β ∕(1(+ β )) )

β

= (1 − 𝜀)k 𝜀t -------

1 + β

=a1,t∕Ξ [ ]

◜◞ ◟◝ (1 − 𝜀)β

kt+1 = k 𝜀t -----------

Ξ (1 + β)

[ ]

dkt+1--= k 𝜀− 1 𝜀-(1-−-𝜀-)β .

dkt t Ξ (1 + β )](OLGModel26x.svg) | (5) |

The steady-state will be the point where  . For convenience, define a

constant

. For convenience, define a

constant

𝒬 =  , ,

|

allowing us to rewrite (5) as

| (6) |

Then the steady-state will be the point where

| (7) |

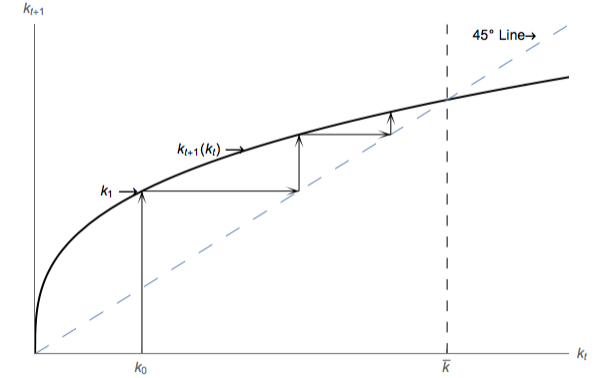

Dynamics of the model can be analyzed using a simple figure relating the

capital stock per capita in period  to that in period

to that in period  . The solid locus is a

graph of equation (5). We depict the 45 degree line because it indicates the set of

‘steady-state’ points where

. The solid locus is a

graph of equation (5). We depict the 45 degree line because it indicates the set of

‘steady-state’ points where  and thus any intersection of the 45

degree line with the

and thus any intersection of the 45

degree line with the  function indicates a steady-state of the

model.

function indicates a steady-state of the

model.

The experiment traced out in the figure is as follows. We start the economy in

period  with capital per capita of

with capital per capita of  , which, from (5), implies a certain

value

, which, from (5), implies a certain

value  for capital in period

for capital in period  . Now think about period

. Now think about period  becoming

becoming  and period

and period  becoming

becoming  . To find the correct level of

capital implied by the model in period

. To find the correct level of

capital implied by the model in period  we need to find the point on

the 45 degree line that corresponds to

we need to find the point on

the 45 degree line that corresponds to  , then go vertically up from

there to find

, then go vertically up from

there to find  . When the same set of gyrations is repeated

the result is that the level of capital converges to the steady-state level

. When the same set of gyrations is repeated

the result is that the level of capital converges to the steady-state level

.

.

We have determined the outcome that will arise in a perfectly competitive economy in which households optimally choose their behavior given market prices with no government intervention.

Often in macroeconomic analysis this constellation of assumptions yields a conclusion that the steady state is optimal (and dynamics are also optimal) according to some plausible criteria. We now examine the optimality properties of the OLG model outcome.

As a preliminary, let’s define the lifetime utility experienced by the young

generation at time  as

as

| (8) |

Suppose our definition of optimality reflects the choices that would be made by a benevolent social planner who maximizes a social welfare function of the form2

| (9) |

subject to the economy’s aggregate resource constraint

| (10) |

where the Hebrew letter  reflects the social planner’s discount factor and the

planner must allocate the society’s resources (“Sources”) between consumption of

the two generations alive at time

reflects the social planner’s discount factor and the

planner must allocate the society’s resources (“Sources”) between consumption of

the two generations alive at time  and the capital stock in period

and the capital stock in period  (“Uses”).

(“Uses”).

The idea is that the social planner cares about every generation’s lifetime happiness, but discounts the happiness of future generations. (We will discuss why discounting is necessary later in the class).

It is possible to show (using methods not described in this handout; see Blanchard and Fischer (1989) for details) that the socially optimal steady state is characterized by the equation

| (11) |

In the case of our Cobb-Douglas production function, this becomes

| (12) |

Comparing this to the outcome that will actually arise,

| (13) |

our point is that there is no particular relationship between the socially optimal outcome and the actual equilibrium outcome that will arise if the social planner is not involved. The actual outcome could have too little capital or too much, and there is no reason to expect it to be the “right” amount.

You might respond by saying that our definition of optimality here is too strong; we might hope that the economy would at least be able to avoid a Pareto inefficient outcome, even if we can’t expect perfect optimality according to the preferences of some mythical Godlike “social planner.”

It turns out, however, that even Pareto efficiency is not guaranteed. (In this context, Pareto efficiency must be defined across generations: The economy is Pareto efficient if there is no way to make one generation better off without making another generation worse off).

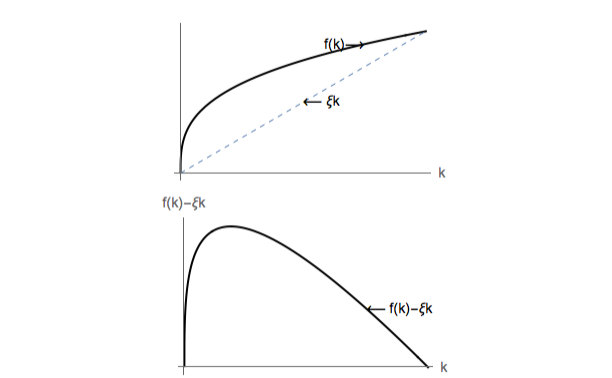

To examine Pareto efficiency, start by rewriting the aggregate DBC by dividing

by the size of the labor force at time  :

:

| (14) |

Define an index of aggregate per capita consumption as

| (15) |

In steady state,  , so if

, so if  is the steady-state level of

is the steady-state level of  then

the accumulation equation implies

then

the accumulation equation implies

| (16) |

Now consider the effects of a change in  on

on  :

:

| (17) |

There exists a  which maximizes per-capita steady-state consumption:

which maximizes per-capita steady-state consumption:

| (18) |

whose solution is obtained from the FOC

| (19) |

and note that this means that for  an extra bit of capital actually

requires a decline in steady-state consumption. An economy in this circumstance

of excessive saving is called ‘dynamically inefficient.’

an extra bit of capital actually

requires a decline in steady-state consumption. An economy in this circumstance

of excessive saving is called ‘dynamically inefficient.’

Note further that there is actually a  so large that consumption would have

to be zero:

so large that consumption would have

to be zero:

| (20) |

These points are illustrated graphically in the remaining figure.

Blanchard, Olivier, and Stanley Fischer (1989): Lectures on Macroeconomics. MIT Press.

Diamond, Peter A. (1965): “National Debt in a Neoclassical Growth Model,” American Economic Review, 55, 1126–1150, http://www.jstor.org/stable/1809231.

Jefferson, Thomas (1789): “‘The Earth Belongs to the Living’: A Letter to James Madison,” http://infomotions.com/etexts/literature/american/1700-1799/jefferson-letters-256.htm.

Samuelson, Paul A. (1958): “An exact consumption loan model of interest with or without the social contrivance of money,” Journal of Political Economy, 66, 467–482.

Weil, Philippe (2008): “Overlapping Generations: The First Jubilee,” Journal of Economic Perspectives, 22(4), 115–34.