©April 15, 2008, Christopher Carroll RamseyCassKoopmans

This handout presents the Ramsey (1928)/Cass (1965)-Koopmans (1965) (RCK) model in continuous time for an economy with exogenous labor-augmenting technological progress.

The economy has a perfectly competitive production sector that uses a Cobb-Douglas aggregate production function

Thus, technological progress allows each worker to produce more and more as time goes by with the same amount of physical capital (this is the definition of labor-augmenting technical progress). The quantity ZL is known as the number of ‘efficiency units’ of labor in the economy.

Suppose that there is a social planner whose goal is to maximize the discounted sum of CRRA utility from per-capita consumption:

| (4) |

subject to

Now define lower case variables as the upper case version divided by efficiency units, i.e.

Note that

This definition also means that C∕L = Z(C∕ZL) = Zc. Recalling now that for a variable growing at rate g

Thus, defining ν = ϑ - (1 - ρ)g and normalizing the initial level of productivity to Z0 = 1, the complete optimization problem can be formulated as

| (21) |

subject to

| (22) |

which has a discounted Hamiltonian representation

| (23) |

The first discounted Hamiltonian optimization condition requires

∂ ∕∂c = 0:

∕∂c = 0:

The second discounted Hamiltonian optimization condition requires:

This is called the “modified golden rule” (or sometimes the “Keynes-Ramsey rule” because it was originally derived by Ramsey with an explanation attributed to Keynes). (The unmodified “golden rule” optimality condition amounts to this equation with the time preference rate set to ϑ = 0, and was proposed by Phelps (1961), an article well worth reading; this is one of the chief contributions for which Phelps won the Nobel prize.)

Thus, we end up with an Euler equation for consumption growth that is just like the Euler equation in the perfect foresight partial equilibrium consumption model, except that now the relevant interest rate can vary over time as f′(k) varies.

Substituting in the modified time preference rate gives

and finally note that defining per capita consumption χ = C∕L so that c = χZ-1, and since (33) can be written

The assumption of labor augmenting technological progress was made because it implies that in steady-state per-capita consumption, income, and capital all grow at rate g.

ċ∕c = 0 implies that at the steady-state value of

Thus, the steady-state k will be higher if capital is more productive (α is higher), and will be lower if consumers are more impatient, population growth is faster, depreciation is greater, or technological progress occurs more rapidly.

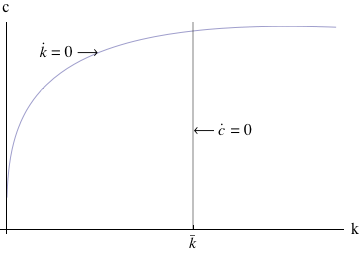

While the RCK model has an analytical solution for its steady-state, it does not have an analytical solution for the transition to the steady-state. The usual method for analyzing models of this kind is a phase diagram in c and k.

The first step in constructing the phase diagram is to take the

differential equations that describe the system and find the points

where they are zero. Thus, from (15) we have that  = 0 implies

= 0 implies

that characterizes

the ċ∕c = 0 locus. These can be combined to generate the borders

between the phases in the phase diagram, as illustrated in figure 1.

that characterizes

the ċ∕c = 0 locus. These can be combined to generate the borders

between the phases in the phase diagram, as illustrated in figure 1.

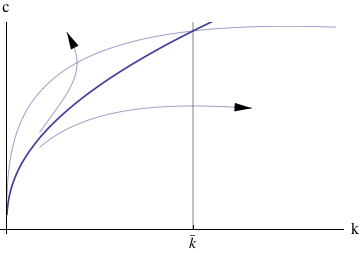

Actually, as stated so far, the solution to the problem is very simple: The consumer should spend an infinite amount in every period. This solution is not ruled out by anything we have yet assumed (except possibly the fact that once k becomes negative the production function is undefined).

Obviously, this is not the solution we are looking for. The problem is that we have not imposed anything corresponding to the intertemporal budget constraint. In this context, the IBC takes the form of a “transversality condition,”

The intuitive purpose of this unintuitive equation is basically to prevent the capital stock from becoming negative or infinity as time goes by. Obviously a capital stock that was negative for the entire future could not satisfy the equation. And a capital stock that is too large will have an arbitrarily small interest rate, which will result in the LHS of the TVC being a positive number, again failing to satisfy the TVC.

Figure 2 shows three paths for c and k that satisfy (33) and (15). The topmost path, however, is clearly on a trajectory toward zero then negative k, while the bottommost path is heading toward an infinite k. Only the middle path, labelled the “saddle path,” satisfies both (33) and (15) as well as the TVC (43).

Cass, David (1965): “Optimum growth in an aggregative model of capital accumulation,” Review of Economic Studies, 32, 233–240.

Koopmans, Tjalling C. (1965): “On the concept of optimal economic growth,” in (Study Week on the) Econometric Approach to Development Planning, chap. 4, pp. 225–87. North-Holland Publishing Co., Amsterdam.

Phelps, Edmund S. (1961): “The Golden Rule of Accumulation,” American Economic Review, pp. 638–642.

Ramsey, Frank (1928): “A Mathematical Theory of Saving,” Economic Journal, 38(152), 543–559.

The RCK model does not have an analytical solution, which means that numerical methods must be used to find out the model’s quantitative implications for transition paths.

The method of solution of these kinds of models is not important for the purposes of first year graduate macroeconomics; this appendix has been written as a reference for more advanced students who might be beginning their research on growth models.

The most effective method of numerical solution is called the ‘time elimination’ method. It starts from the fact that

Note from (33) that we can write

so we can obtain

There is one problem, however, which is that at the steady-state

values of c and k both numerator and denominator of this equation

are zero. We could use L’Hopital’s rule to derive an expression in

this neighborhood, but that gets very messy. The alternative is to

solve the differential equation twice: Once for a domain extending

from k = 0 to  - ε, yielding c-(k), and once for a domain from

- ε, yielding c-(k), and once for a domain from

+ ε to some large value of k, yielding c+(k). The true consumption

policy function can then be approximated by interpolating

between the upper endpoint of c-(k) and the lower endpoint of

c+(k).

+ ε to some large value of k, yielding c+(k). The true consumption

policy function can then be approximated by interpolating

between the upper endpoint of c-(k) and the lower endpoint of

c+(k).

|

|

= 0 Loci

= 0 Loci