September 13, 2023, Christopher D. Carroll 2PeriodLCModel

September 13, 2023, Christopher D. Carroll 2PeriodLCModel

September 13, 2023, Christopher D. Carroll 2PeriodLCModel

Irving Fisher (1930) first analyzed the optimization problem of a consumer who faces no uncertainty and lives for two periods.

In its most general form, the household’s lifetime value function can be written

where the first argument reflects consumption in ‘youth’ while the second argument represents consumption in ‘old age’ and we assume that the derivatives with respect to the first and second arguments are positive,

| (1) |

while the second derivatives are negative,

| (2) |

The consumer begins the first period with resources of  (think

‘bank balances’) and income of

(think

‘bank balances’) and income of  . Total resources are divided between

consumption and end-of-period assets

. Total resources are divided between

consumption and end-of-period assets  (‘assets after all actions’ in period

(‘assets after all actions’ in period

):

):

| (3) |

Balances at the beginning of period 2 are equal to end-of-first-period

accumulated assets  , rewarded by a gross interest factor

, rewarded by a gross interest factor  :

:

| (4) |

This is the dynamic budget constraint or DBC for this problem. A DBC links two adjacent periods of time. A more comprehensive kind of constraint is the intertemporal budget constraint (IBC):

| (5) |

which must be satisfied over an extended (multiperiod) span of time like a lifetime.

For various purposes, it is useful to keep track of human wealth  , defined

as the present discounted value of future labor income (the operator

, defined

as the present discounted value of future labor income (the operator

denotes the present discounted value of the variable

denotes the present discounted value of the variable  from

the perspective of the beginning of period

from

the perspective of the beginning of period  through the end of the

horizon),

through the end of the

horizon),

| (6) |

Because we have assumed (in (1)) that an additional unit of consumption always yields extra utility, we can reach our first conclusion (as opposed to assumption) in the model: Once the consumer has reached the last period of life, he will consume all available resources:

| (7) |

This means that the IBC will hold with equality (if it did not, utility could be increased by consuming more in one or both periods). Thus, the IBC can be rewritten as

| (8) |

The general form that the IBC will take is that the present discounted value of lifetime spending must equal the present discounted value of lifetime resources:

| (9) |

Substituting in the definition of  means that our problem can now be

stated as:

means that our problem can now be

stated as:

|

Now we can write the problem as a Lagrange multilier problem, where the maximand is:

| (10) |

The first order conditions are:

| (11) |

and substituting the second of these into the first we get

| (12) |

This is the same condition you get when deciding between two commodities at

a point in time, where we can now think of  as the intertemporal price: How

much of good 2 (consumption in period 2) do I get in exchange for giving up a

unit of good 1 (consumption in period 1).

as the intertemporal price: How

much of good 2 (consumption in period 2) do I get in exchange for giving up a

unit of good 1 (consumption in period 1).

Now suppose that the consumer’s utility is time-separable, and the felicity function (felicity is the utility obtained in a single period of a multi-period problem) is the same in both periods of life, so that

| (13) |

where  is a time preference factor that specifies how the

consumer trades off utility in period 1 against utility in period

2.1

is a time preference factor that specifies how the

consumer trades off utility in period 1 against utility in period

2.1

From our assumptions (1) and (2) we know that the felicity function must satisfy

| (14) |

and since the felicity functions are the same in both periods we have that

| (15) |

Substituting these equations into (12) yields the Euler equation for consumption:

| (16) |

The Euler equation is a central result in intertemporal optimization theory, and will be used again and again as the course progresses. It is therefore worth studying carefully to be sure you understand it thoroughly.

To help obtain the intuition for why the Euler equation is necessary for

optimality, consider the following thought experiment. Designate  and

and  as

the optimal levels of consumption in this problem, the levels that solve the

maximization problem under some set of circumstances. Thus, the highest

attainable utility is

as

the optimal levels of consumption in this problem, the levels that solve the

maximization problem under some set of circumstances. Thus, the highest

attainable utility is

| (17) |

Now consider reducing consumption by some small amount  in period 1,

investing that

in period 1,

investing that  so that it grows to

so that it grows to  in period 2, and then consuming it in

period 2. What happens to utility?

in period 2, and then consuming it in

period 2. What happens to utility?

Taking first-order Taylor expansions, the levels of first-period and second-period utility are now

| (18) |

Now the difference between the maximum possible utility and the new situation is given by

![u(c ∗)+ βu (c∗)− [u (c∗) − u ′(c ∗)𝜖 + β (u (c∗) + u ′(c ∗)R 𝜖)] = u′(c∗)𝜖− βu ′(c ∗)R𝜖.

1 2 1 1 2 2 1 2](2PeriodLCModel39x.svg) | (19) |

But it must be the case that (19) is approximately equal to zero. To see why,

suppose it were a negative number. That would mean that moving from the

original situation with  to the new situation with

to the new situation with

resulted in an increase in utility. But we assumed

that

resulted in an increase in utility. But we assumed

that  were already the utility-maximizing choices, which clearly could not

be true if adjusting

were already the utility-maximizing choices, which clearly could not

be true if adjusting  downward by

downward by  and

and  upward by

upward by  increased

utility. Similarly, if the expression were positive, then utility could be increased

by doing the opposite (i.e. increasing consumption in period 1 by

increased

utility. Similarly, if the expression were positive, then utility could be increased

by doing the opposite (i.e. increasing consumption in period 1 by  and

reducing it in period 2 by

and

reducing it in period 2 by  ). Thus, in either case if the expression is not zero,

we have a contradiction to the assumption that

). Thus, in either case if the expression is not zero,

we have a contradiction to the assumption that  and

and  are the

utility-maximizing choices.

are the

utility-maximizing choices.

To make further progress, it is necessary to make more specific assumptions about the structure of the utility function. The most common assumption is that utility takes the Constant Relative Risk Aversion form,

| (20) |

with marginal utility

| (21) |

Consider equation (16) with CRRA utility,

| (22) |

Now note that this equation allows us to calculate the intertemporal elasticity

of substitution as the change in the ratio of the log of  to the log change in

the intertemporal price

to the log change in

the intertemporal price  :

:

| (23) |

Next note that from (22) we can calculate the PDV of lifetime consumption from the perspective of the first period of life as

| (24) |

Now we can use the intertemporal budget constraint:

| (25) |

Thus, we have solved the two-period life cycle saving problem for the

consumption function  relating the level of consumption to all of the

parameters of the problem.

relating the level of consumption to all of the

parameters of the problem.

One of the surprising features of the solution goes by the name of “Fisherian

Separation”: Notice that the profile of consumption growth over the lifetime is

given by (22) regardless of the shape of the income profile. For two consumers

with the same total amount of lifetime wealth (combined  and

and  , the level

and growth rates of consumption over the lifetime will be identical whether the

consumer’s lifetime wealth is entirely concentrated in the first period (that

is,

, the level

and growth rates of consumption over the lifetime will be identical whether the

consumer’s lifetime wealth is entirely concentrated in the first period (that

is,  ), entirely concentrated in the last period (

), entirely concentrated in the last period ( ), split

half-and-half, or organized any other way. Fisherian Separation is a pervasive

feature of models that combine perfect foresight and a lack of liquidity

constraints.

), split

half-and-half, or organized any other way. Fisherian Separation is a pervasive

feature of models that combine perfect foresight and a lack of liquidity

constraints.

A common assumption (for simplicity, not realism) is that

, which is equivalent to assuming that the utility function is

logarithmic:2

, which is equivalent to assuming that the utility function is

logarithmic:2

| (26) |

In this case it turns out that we can simply substitute  into the solution

for consumption, obtaining

into the solution

for consumption, obtaining

| (27) |

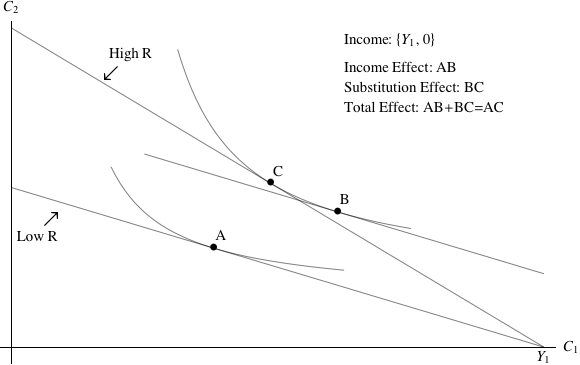

The classic graphical analysis of this problem is shown in figure 1.

The top figure depicts a situation in which all of the consumer’s lifetime

income is earned in the first period of life. The budget constraint in the initial

situation, associated with a “Low  ”, yields an optimal consumption choice

labeled as point

”, yields an optimal consumption choice

labeled as point  where the budget constraint is tangent to the indifference

curve. When the interest factor is increased to the “High

where the budget constraint is tangent to the indifference

curve. When the interest factor is increased to the “High  ” situation, the

optimal consumption choice moves to point

” situation, the

optimal consumption choice moves to point  .

.

Note first that if all income is earned in the first period of life, an increase in the interest factor is unambiguously good for the consumer - the set of consumption possibilities is strictly larger.

Second, the movement from point  to point

to point  can be decomposed into

two parts: an income effect

can be decomposed into

two parts: an income effect  and a substitution effect

and a substitution effect  .

.

Call the low and the high interest factors respectively  and

and  .

.

The income effect is the answer to the question “Suppose we wanted to change

lifetime value by the same amount as it is changed by going from  to

to  , but

we wanted to achieve this change in value at the initial interest factor

, but

we wanted to achieve this change in value at the initial interest factor

. Supposing we gave the consumer enough extra initial resources to

achieve the change in value, how would their consumption allocation

change?”

. Supposing we gave the consumer enough extra initial resources to

achieve the change in value, how would their consumption allocation

change?”

In order to relate this back to the algebraic analysis above, it will be useful

to rewrite lifetime value as a function simply of initial resources and

the interest factor (taking  and other parts of the problem as

given):

and other parts of the problem as

given):

| (28) |

Using this function, the income effect is obtained as the value of  in the

equation

in the

equation  .

.

The substitution effect is the answer to the question, “Staying on the new

indifference curve, how much does the allocation of consumption change as a

consequence of the difference in interest factors between  and

and  ?” This is

captured in the movement from

?” This is

captured in the movement from  to

to  .

.

Note that the income and the substitution effects on  are opposite in sign.

A higher interest factor gives consumers the incentive to substitute future for

current consumption (

are opposite in sign.

A higher interest factor gives consumers the incentive to substitute future for

current consumption ( is lower at point

is lower at point  than at

than at  ). But a higher

interest factor also gives consumers the ability to consume more in both periods.

Whether

). But a higher

interest factor also gives consumers the ability to consume more in both periods.

Whether  rises or falls in response to the increase in interest factors

will depend on the relative magnitudes of the income and substitution

effects.

rises or falls in response to the increase in interest factors

will depend on the relative magnitudes of the income and substitution

effects.

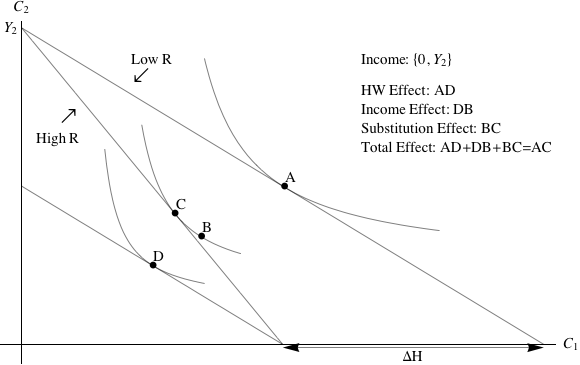

The lower figure shows a similar experiment, with the sole difference that the consumer’s lifetime resources are exclusively concentrated in period 2.

In this case, the period 1 consumer must borrow against future income in order to consume anything. An increase in interest factors is therefore unambiguously bad (the available set of consumption choices is strictly smaller).

The optimal choice again moves from point  to point

to point  . However, we now

decompose the movement into three parts. The first part is called the human

wealth effect. It captures the fact that the present discounted value of lifetime

resources

. However, we now

decompose the movement into three parts. The first part is called the human

wealth effect. It captures the fact that the present discounted value of lifetime

resources  is smaller when interest rates are higher; the magnitude of the

change in human wealth is depicted on the horizontal axis of the figure. The

human wealth effect is the consequence that an equivalent change in lifetime

resources would have in the absence of any change in interest factors. So

the human wealth effect takes the consumer from point

is smaller when interest rates are higher; the magnitude of the

change in human wealth is depicted on the horizontal axis of the figure. The

human wealth effect is the consequence that an equivalent change in lifetime

resources would have in the absence of any change in interest factors. So

the human wealth effect takes the consumer from point  to point

to point

.

.

Notice that once we have computed the human wealth effect, if we treat point

as the starting point of our analysis, the remaining analysis is identical to

that for the upper figure: We can increase the interest factor from

as the starting point of our analysis, the remaining analysis is identical to

that for the upper figure: We can increase the interest factor from  to

to  ,

which causes the equilibrium point to change from point

,

which causes the equilibrium point to change from point  to point

to point  , a

movement that can be decomposed into an income effect

, a

movement that can be decomposed into an income effect  (analogous to the

income effect

(analogous to the

income effect  in the original analysis) and a substitution effect

in the original analysis) and a substitution effect

.

.

The terminology here is a modification (refinement) of the terminology often employed in micro textbooks, where the “income effect” is defined in a way that would incorporate both what I am calling the income effect and what I am calling the human wealth effect.

The reason to make this distinction is that it is important to distinguish between effects on behavior caused by the fact that the discounted value of future income is changed, and effects caused by the fact that the income that will be earned on savings is different. Summers (1981) vigorously made the point that in standard life cycle models, the quantitative magnitude of the human wealth effect dwarfs the size of either the income or the substitution effects, because for most people most of their lifetime income is in the future.

Fisher, Irving (1930): The Theory of Interest. MacMillan, New York.

Frederick, Shane, George Loewenstein, and Ted O’Donogue (2002): “Time Discounting and Time Preference: A Critical Review,” Journal of Economic Literature, XL(2), 351–401.

Samuelson, Paul A (1937): “A note on measurement of utility,” The Review of Economic Studies, 4(2), 155–161.

Samuelson, Paul A. (1958): “An Exact Consumption-Loan Model of Interest with or without the Social Contrivance of Money,” Journal of Political Economy, 66(6), 467–482.

Summers, Lawrence H. (1981): “Capital Taxation and Accumulation in a Life Cycle Growth Model,” American Economic Review, 71(4), 533–544, http://www.jstor.org/stable/1806179.